We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Best option of keeping cash over of 85K getting best easy interest?

Comments

-

Do you need to keep it all as cash? If some is invested then less need to monitor rates and it can just be left to growRemember the saying: if it looks too good to be true it almost certainly is.1

-

Noted and Tks.jimjames said:Do you need to keep it all as cash? If some is invested then less need to monitor rates and it can just be left to grow

I'm aware that historically, plonk a big chunk in a GIA or similar and it always exceedes cash getting interest.

It's just possible that I may decide to use a large chunk of cash to possibly buy a property if it suited me.

If say I plonk 50% if cash in GIA and we are in a long dip, I'll be unlikely to cash it out.

Another dynamic is using many different institutions with different terms/maturity & and lock ins, plus interest paid yearly or maturity instead of monthly. Monthly looks best to mitigate 40% income tax, getting a few good % rate lock ins and they all say pay interest on block in 2025/26 won't allow me to use 20% income tax availability window 2024/25 and my DB pension will increase next April.

I think interest rates will move very slowly and not by big amounts, I'm guessing UK maybe 4.5/4.75% Xmas 2024 and maybe 4/4.25% Xmas 2025.

So currently feeling monthly interest and instant access mostly plus maybe a few lock ins no longer than a year.

Cheers Roger.

1 -

RogerPensionGuy said:

Two friends are using Insignis as an all in one savings place and their IFAs told them Insignis is better than all others in this field, I do wonder for who there are better, maybe I can find an all in one savings comparison site?

https://www.insigniscash.com/personal-savings/I don't have personal experience with Insignis and I'd never heard of them so did a quick browse and there are a few yellow flags on their website, so I'd be careful with them. There's a lot of jargon oriented towards financial advisors, they have a bit of a thing with calling their customers "clients", and notably, unlike Raisin or HL, they charge an (also notably, not publicly disclosed) management fee. It seems to become a direct client you have to fill out a contact us form, it seems really oriented to FAs to me. This page https://www.insigniscash.com/wealth-managers/ talk about FAs "becoming partners" and includes the very choice quote:Flexible feesYou can choose between earning a share of the ongoing management fee or passing a fee discount onto your clients – the choice is up to you.

So not making any accusations but it may well be your friends' IFAs think Insignis is better because (unlike Raisin or HL as far as I can tell) they can basically get a commission on it.

edit: Someone on trustpilot said the fee they were charged is 0.2% which is frankly ridiculous for a savings marketplace in my opinion, for context Vanguard charges 0.15% to manage an actual investment platform which is much more complicated. It sounds like the fee scales down with how much you put in but still I would avoid.

4 -

I too had never heard of Insignis so thought I'd take a look. Their minimum deposit of £100,000 would suggest they're aiming for those with more cash than most. They only list 'top payers' and while they do seem to be higher than HL they do charge a fee ( the amount is not disclosed) so one wonders just how competitive to the likes of HL or AJ Bell they are once this is taken into account.

1 -

I guess my perfect solution is like one of these institutions that allow simple tinkering and moving money between the various savings buckets to try maintaining the best overall interest, lock-ins and allowing me to keep some instant, medium or longer term buckets to have balance.

I would also every account pays monthly or the end of every financial year.

I would also like The One Main Account Instution to produce me a simple interest earned at the end of every year.

Plus obviously with all the above I would like to aheive the best overall net interest to me and then just pay income tax on that.

On a side note I saw HMRC were going to close the phone line help service for 6 months this year, then felt obliged to cancel that idea, but to me it looks like they don't have sufficient staff currently and with interest rates at current levels and CGT gone from 12.3K to 3K now in a 13 months period, lots of problems and hassle coming.

I wonder how many more nee people will be having to do self assement for tax 2023/24 and probably much more 2024/25 that have never done this before.

***

https://www.bbc.co.uk/news/business-68606722.amp

***

https://www.thisismoney.co.uk/money/smallbusiness/article-12919215/amp/Self-assessment-needs-file-tax-return-January-face-hefty-bill-selling-online.html

0 -

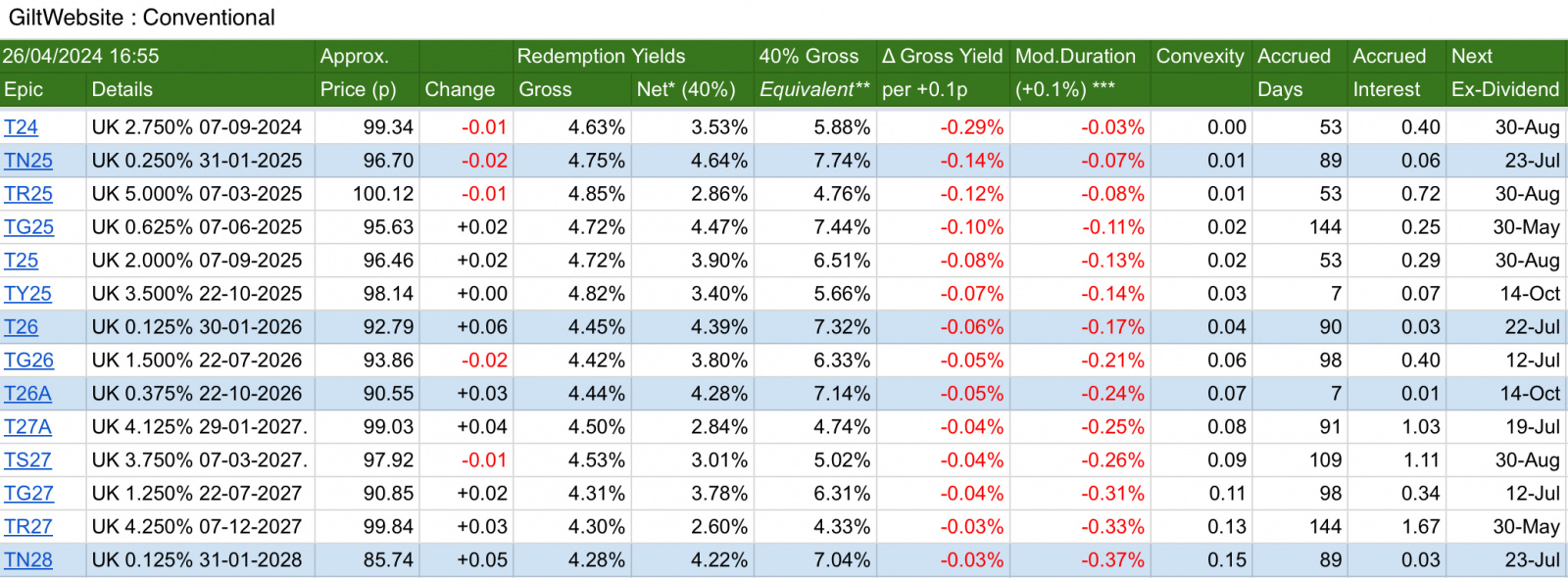

If you're willing to 'lock' some of the money up for a while then another option would be directly owning gilts, not a fund, and if you're worried about tax look to low coupon gilts as capital gains are tax free. Held to maturity the returns are certain but of course you could sell them when the market is open. You can buy these via HL.There's also one month UK Treasury bills offered via Freetrade. Your money's locked in for a month and Freetrade will automatically roll them until you tell it to stop. Given it's a relatively early stage company I'd be circumspect about having vast amounts of money with Freetrade, though. The current annualised yield is c.5.1%.

https://freetrade.io/treasury 2

2 -

I have been reading up on the HL Active Savings Account.

I must say it looks simple to open and operate, no direct charges, just get a lesser interest rate than going direct with the various institutions.

I also like the way HL will produce a single statement showing how much interest was received every year, this is much less hassle for tax reasons. Below is a quote from HL.

"As part of your April bi-annual statement, we will send you a consolidated tax schedule which summarises all the interest you have received in the previous tax year from the products held in your Active Savings Account along with all your other holdings within Hargreaves Lansdown accounts. You are responsible for submitting this to HMRC with your tax return"

Looks like I will open an account with HL and as the post above states, doing a mixture of gilts and cash savings look simple enough I hope.

0 -

RogerPensionGuy said:I must say it looks simple to open and operate, no direct charges, just get a lesser interest rate than going direct with the various institutions.In my experience they are frequently the same. The participating partners benefit from HL's scale and client baseThe top AS 1 year fix with Close Brothers is the same as direct, as is Zopa, Sainsbury's and Paragon. Aldermore with AS is 5.05% and 4.65% direct1

-

I opened up a HL and am happy and frustrated with their security varafication systems, rather they are secure and it feels secure to me.

So I'll probably buy gilts and use the Active Saver.

The Active Saver looks simple.

I'll have to investigate and understand how to buy gilts.

***

A quick question to anyone, if I put in X pounds in to a product in their Active Saver today, can I put in more X pounds in to that product tomorrow or next week?

***

My guess is if it's an instant access account product and it still shows availability, I can just put in more pounds whenever I like.

However, if product is a term product, lets say it says apply by 10MAY24, I can top up that account if it still shows availability when I look in a few days.

Or after opening a term product, do I have 7 or 14 days from opening to top up product.

I tried looking on HL site and was unable to see the exact mechanics of exactly how it works, I was going to plonk a token amount in the various products and then when I see the workings, top up the various products to the required levels I feel appropriate.

I was poking about for monthly interest and only noticed monthly interest available on instant products, I noticed most longer term accounts pay interest on maturity, so that's not purfect on managing interest payments every year, I did notice a 2 or 3 year term that paid interest annually, so that could be helpful for me.

Any information on my one *** question *** above would be most helpful and thanks in advance.

0 -

It depends on the productRogerPensionGuy said:A quick question to anyone, if I put in X pounds in to a product in their Active Saver today, can I put in more X pounds in to that product tomorrow or next week?My guess is if it's an instant access account product and it still shows availability, I can just put in more pounds whenever I like.Yes but it may not show availability to new applicants, it will be available to you howeverHowever, if product is a term product, lets say it says apply by 10MAY24, I can top up that account if it still shows availability when I look in a few days.You cannot 'top up' or add to your initial deposit. You have to cancel your initial deposit and then add it again if it's still availableOr after opening a term product, do I have 7 or 14 days from opening to top up product.Don't confuse 'opening' with adding your deposit to HL's queue (if you like). The account is only opened and earning interest from the Start Date, there is no funding window once opened or Started. Sometimes, though not very often, there is a cooling down period after the start date if you want to cancel. Read the T&CsI was poking about for monthly interest and only noticed monthly interest available on instant products, I noticed most longer term accounts pay interest on maturity, so that's not purfect on managing interest payments every year, I did notice a 2 or 3 year term that paid interest annually, so that could be helpful for me.I have never seen a fixed term account with monthly interest. If you open a 2+ year fix some of them pay annually, others on maturity

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards