We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Interest on Flexible ISAs during the year?

Comments

-

Yes I think that's right. For "old" money, if you want to change providers, that has to be done by a transfer (even if it's a flexi). For "new" money (ie the current tax year), if the ISA where it is now is flexi, you can do it manually by withdrawing it and depositing it somewhere else and you've not lost any of your allowance (as long as you do it within the same tax year). For a non-flexi ISA, a transfer is still the only option (if you want to retain the money in an ISA), since withdrawing anything takes it out of the ISA umbrella.csw5780 said:

So is it only necessary to TRANSFER funds held in an ISA between tax years? As if they are flexible, moving funds between them in the current tax year merely adjusts the £20k? ie the allowance is not lost on withdrawals outside the ISA if deposited to any ISA in the current tax year.slinger2 said:

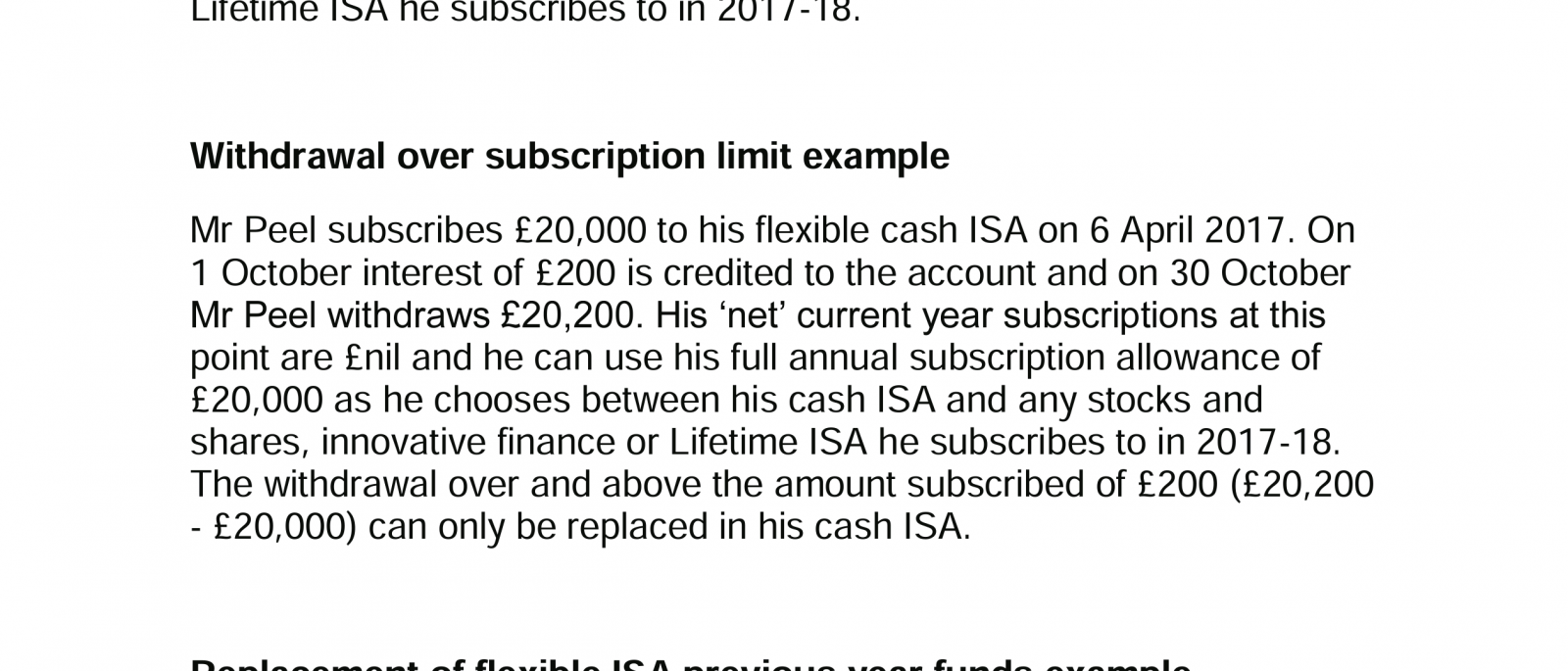

That's right. Your net subscriptions after the withdrawals are £nil, so you've got £20k left to use as you like. The £200 seems to be treated like "old" money and has to go back to where it came from.csw5780 said:

In the example quoted surely the £200 can be returned to the originating account ONLY. However the example implies that the remaining current year £20k allowance could be payed into any other ISA, cash or otherwise including the originating account.slinger2 said:

Seems my assumption was wrong. In any case you can't increase your allowance by withdrawing the interest, Your net subscriptions after the withdrawals are £nil, not -£200.surreysaver said:

It isn't so black and white. Interest earned in previous tax years is obviously previous years monies.Bjn201_2 said:Got it. I didn't realise it was so black and white. Absolutely not possible then.

Interest earned this year isn't part of this year's subscriptions. Nor is it part of last year's money.

Without looking, I suspect you'd be able to take the money out and pay it back in (as long as its the same account). Whether the organisation's systems would be confused by that or not I don't know

1 -

So MSE guide is out of date:slinger2 said:

Yes I think that's right. For "old" money, if you want to change providers, that has to be done by a transfer (even if it's a flexi). For "new" money (ie the current tax year), if the ISA where it is now is flexi, you can do it manually by withdrawing it and depositing it somewhere else and you've not lost any of your allowance (as long as you do it within the same tax year). For a non-flexi ISA, a transfer is still the only option (if you want to retain the money in an ISA), since withdrawing anything takes it out of the ISA umbrella.csw5780 said:

So is it only necessary to TRANSFER funds held in an ISA between tax years? As if they are flexible, moving funds between them in the current tax year merely adjusts the £20k? ie the allowance is not lost on withdrawals outside the ISA if deposited to any ISA in the current tax year.slinger2 said:

That's right. Your net subscriptions after the withdrawals are £nil, so you've got £20k left to use as you like. The £200 seems to be treated like "old" money and has to go back to where it came from.csw5780 said:

In the example quoted surely the £200 can be returned to the originating account ONLY. However the example implies that the remaining current year £20k allowance could be payed into any other ISA, cash or otherwise including the originating account.slinger2 said:

Seems my assumption was wrong. In any case you can't increase your allowance by withdrawing the interest, Your net subscriptions after the withdrawals are £nil, not -£200.surreysaver said:

It isn't so black and white. Interest earned in previous tax years is obviously previous years monies.Bjn201_2 said:Got it. I didn't realise it was so black and white. Absolutely not possible then.

Interest earned this year isn't part of this year's subscriptions. Nor is it part of last year's money.

Without looking, I suspect you'd be able to take the money out and pay it back in (as long as its the same account). Whether the organisation's systems would be confused by that or not I don't know

https://www.moneysavingexpert.com/savings/flexible-isas/ as last tax year you couldn’t pay new money into more than one cash ISA.0

as last tax year you couldn’t pay new money into more than one cash ISA.0 -

Yes. One of many many web sites that have out of date information. As you say, it wasn't possible before because you could only pay into one Cash ISA each tax year. All change.csw5780 said:

So MSE guide is out of date:slinger2 said:

Yes I think that's right. For "old" money, if you want to change providers, that has to be done by a transfer (even if it's a flexi). For "new" money (ie the current tax year), if the ISA where it is now is flexi, you can do it manually by withdrawing it and depositing it somewhere else and you've not lost any of your allowance (as long as you do it within the same tax year). For a non-flexi ISA, a transfer is still the only option (if you want to retain the money in an ISA), since withdrawing anything takes it out of the ISA umbrella.csw5780 said:

So is it only necessary to TRANSFER funds held in an ISA between tax years? As if they are flexible, moving funds between them in the current tax year merely adjusts the £20k? ie the allowance is not lost on withdrawals outside the ISA if deposited to any ISA in the current tax year.slinger2 said:

That's right. Your net subscriptions after the withdrawals are £nil, so you've got £20k left to use as you like. The £200 seems to be treated like "old" money and has to go back to where it came from.csw5780 said:

In the example quoted surely the £200 can be returned to the originating account ONLY. However the example implies that the remaining current year £20k allowance could be payed into any other ISA, cash or otherwise including the originating account.slinger2 said:

Seems my assumption was wrong. In any case you can't increase your allowance by withdrawing the interest, Your net subscriptions after the withdrawals are £nil, not -£200.surreysaver said:

It isn't so black and white. Interest earned in previous tax years is obviously previous years monies.Bjn201_2 said:Got it. I didn't realise it was so black and white. Absolutely not possible then.

Interest earned this year isn't part of this year's subscriptions. Nor is it part of last year's money.

Without looking, I suspect you'd be able to take the money out and pay it back in (as long as its the same account). Whether the organisation's systems would be confused by that or not I don't know

https://www.moneysavingexpert.com/savings/flexible-isas/as last tax year you couldn’t pay new money into more than one cash ISA.1 -

Strictly speaking, what they say there is factually accurate, but it omits the fact that you can now also pay into another cash ISA!csw5780 said:So MSE guide is out of date:

https://www.moneysavingexpert.com/savings/flexible-isas/as last tax year you couldn’t pay new money into more than one cash ISA.

As ever, it's better to rely on the official documentation, which has been updated:Withdrawals of current year subscriptions, can effectively be replaced in any current year ISA.https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas

instead of what it used to say:Withdrawals of current year subscriptions, can effectively be replaced in any current year ISA, but cannot breach the ‘one ISA of each type per tax year’ rule.1 -

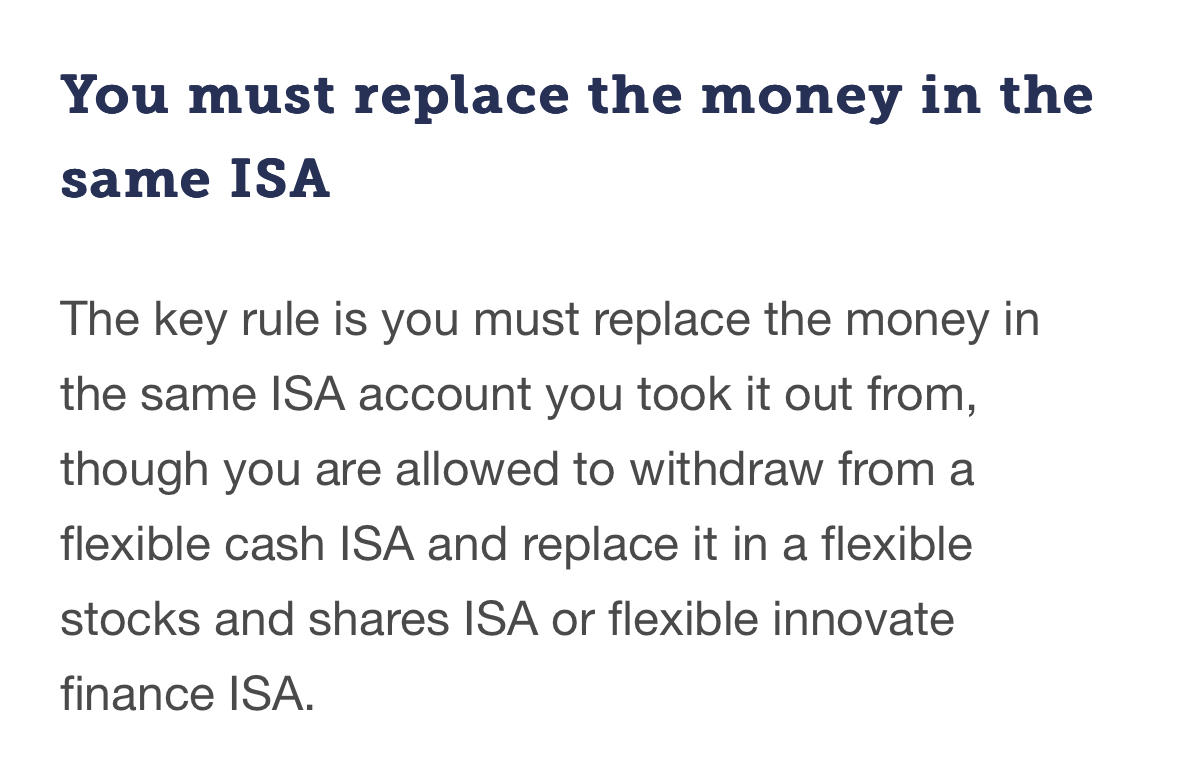

The MSE guide has been wrong on one point from the outset and probably always will be. When replacing flexibly withdrawn subscriptions from the current tax year, they've never needed to be replaced in a flexible ISA.

4 -

slinger2 said:

That's right. Your net subscriptions after the withdrawals are £nil, so you've got £20k left to use as you like. The £200 seems to be treated like "old" money and has to go back to where it came from.csw5780 said:

In the example quoted surely the £200 can be returned to the originating account ONLY. However the example implies that the remaining current year £20k allowance could be payed into any other ISA, cash or otherwise including the originating account.slinger2 said:

Seems my assumption was wrong. In any case you can't increase your allowance by withdrawing the interest, Your net subscriptions after the withdrawals are £nil, not -£200.surreysaver said:

It isn't so black and white. Interest earned in previous tax years is obviously previous years monies.Bjn201_2 said:Got it. I didn't realise it was so black and white. Absolutely not possible then.

Interest earned this year isn't part of this year's subscriptions. Nor is it part of last year's money.

Without looking, I suspect you'd be able to take the money out and pay it back in (as long as its the same account). Whether the organisation's systems would be confused by that or not I don't know@slinger2 this is no longer the case. HMRC has updated its guidance as of 30th April and no longer permits any flexibly withdrawn subscriptions to be replaced in a different ISA than the one it was taken from.See new text at https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas(so now the MSE guide is wrong in a different way") )

)

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards