We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

ISA Providers; Are most choosing to ignore the Chancellor's new ISA Reforms?

Comments

-

Jimjames,

Thanks. I was just waiting for that answer from Proplend as I queried exactly that this afternoon.

I wasn't sure and had wondered if maybe both ISAs had to be mutually linked (with no middle-man account).

I also have wrongly believed that any monies paid out my flexible ISA had to go back into that same ISA.

You are quite right - My Chip responder did answer the original query put to him.

Proplend staff however, had the benefit of my full scenario and exactly what my goal was. Hence, I thought that they would have thought beyond my query (as you did) and come up with your solution earlier.

So I now have a perfectly viable solution based on your knowledge of the rules. Cheers.

I'll be interested still to see if Proplend now reaches the same solution!!1 -

-

Glad it all has worked out for you and you now have a solution to achieve what you wantedVTechnician said:Remember the saying: if it looks too good to be true it almost certainly is.0 -

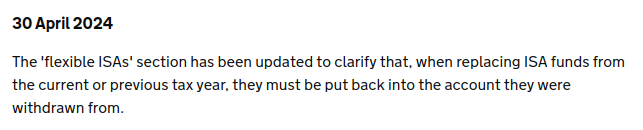

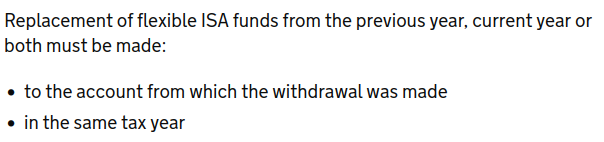

@VTechnician @jimjames unfortunately HMRC has updated its guidance as of 30th April and no longer permits any flexibly withdrawn subscriptions to be replaced in a different ISA than the one it was taken from. To do as you wish would now require a series of partial transfers (if this new interpretation is enforced).

https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas

https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas

4 -

Well @jimjames,masonic said:@VTechnician @jimjames unfortunately HMRC has updated its guidance as of 30th April and no longer permits any flexibly withdrawn subscriptions to be replaced in a different ISA than the one it was taken from. To do as you wish would now require a series of partial transfers (if this new interpretation is enforced).https://www.gov.uk/guidance/manage-isa-subscriptions-for-your-investors#flexible-isas

Since I've already drip-fed 1/3 of my allocated funds from Flexible cash ISA 1 into Flexible IFISA2 via a 'middle-man' current acct, as you say: " ..if they enforce.." this newer guidance, then I could be facing some punitive action.

I'd expected that the above would count as 50% of my annual ISA allowance (as I placed the other 50% in a separate cash ISA).

Therefore, it leaves me wondering whether, at some point, I will become accused of ISA over-funding by 25% this financial year.

I haven't any experience of apologising to HMRC for an infringement. However, if enforcement becomes a certainty rather than a risk, then I doubt that the enforcer would relent and admit that the series of conflicting issues of guidance has caused confusion and mislead.1 -

I'm in the same boat as you, having parked some money in Chip before moving it to a fixed rate account elsewhere. I'm hoping that an apologetic letter might do the trick, especially since their own advise was not updated until the end of April.

Given that Chip says I've used none of my current year's allowance there also a sporting chance that the data that HMRC will get won't allow them to see that I've broken the new rule.

I've got details of when money went in and out of my ISAs should I need to demonstrate that I never subscribed more than £20k at any one time.1 -

There is detailed information published online describing the structure of the electronic records ISA managers need to submit when they do their annual returns. Currently there isn't sufficient information to determine the maximum subscribed to an ISA during a tax year if there were flexible withdrawals (only the net subscription is provided). So we shall see if that gets changed over the course of this year. My suspicion is that it won't (because ISA managers would need to know they are supposed to be keeping track of this and would also need to update their reporting systems). Perhaps the changes will be set up this year so that next year can be monitored. After all, even HMRC wasn't aware of this change in time for the start of this tax year

0 -

I suspect that the reason the change has been made to the regulations is that HMRC have realised they don't have the ability to police or check it so I very much doubt they will know their new rule has been broken and so even more unlikely they will be in touch.slinger2 said:

Given that Chip says I've used none of my current year's allowance there also a sporting chance that the data that HMRC will get won't allow them to see that I've broken the new rule.Remember the saying: if it looks too good to be true it almost certainly is.1 -

Thank you again to @masonic and @jimjames for your input.

I believe, therefore, that the risk of having my 'collar felt' by HMRC's enforcers for TY24/25 is low, based on the expected pace of change that ISA managers implement these required software changes.

I should add; I acknowledge that you are not responsibly bound by your advice or comments;-).

I also note that HMRC has failed to rid their servers of conflicting information such as these worked examples for flexible ISAs which still hit the Google top 10 hits when searching for contexual advice:

https://assets.publishing.service.gov.uk/media/5a958128e5274a5b849d3b74/worked_examples_of_flexible_ISAs.pdf

...leaving the investor responsible to always check for newer contextual info.1 -

I'm having the same issue with providers choosing not to accept the new rules, although my problem is not with partial transfers, it's with opening a second ISA! Not only does the one where I first opened it not accept a second ISA in the same year, but none of the 5-7 providers that I've checked/asked accept a ISA with new money if I've already opened one this year!!

I won't have any other option but to lose interest and move the initial one, or not add any more money to cash ISAs this year...

Edit: I know, I should have checked this before opening the first one

It seems some building societies around me allow this, so there's hope - not the best rates, but better than paying tax hahaBeing brave is going after your dreams head on0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards