We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Most Tax Efficient Gilt Today

MoneyMan01

Posts: 230 Forumite

What is the most tax efficient Gilt available today, for the shortest length of time?

I basically want to store some money until the new tax year, as I have maxed out premium bonds, and I am getting taxed 40% on what I am earning above the £500 interest.

0

Comments

-

TheDarkKnight93 said:What is the most tax efficient Gilt available today, for the shortest length of time?I basically want to store some money until the new tax year, as I have maxed out premium bonds, and I am getting taxed 40% on what I am earning above the £500 interest.Depending on how long you want to invest for you don't have a massive amount of choice but if very short term TG24 22/04/24?

0

0 -

Do you mean you need to store the money for the next 2 weeks, or for some period between 2 weeks and 54 weeks? Planning to keep money in gilts for just 2 weeks seems inefficient, to me - you'll just be betting on interest rate sentiment, and incurring transaction costs.0

-

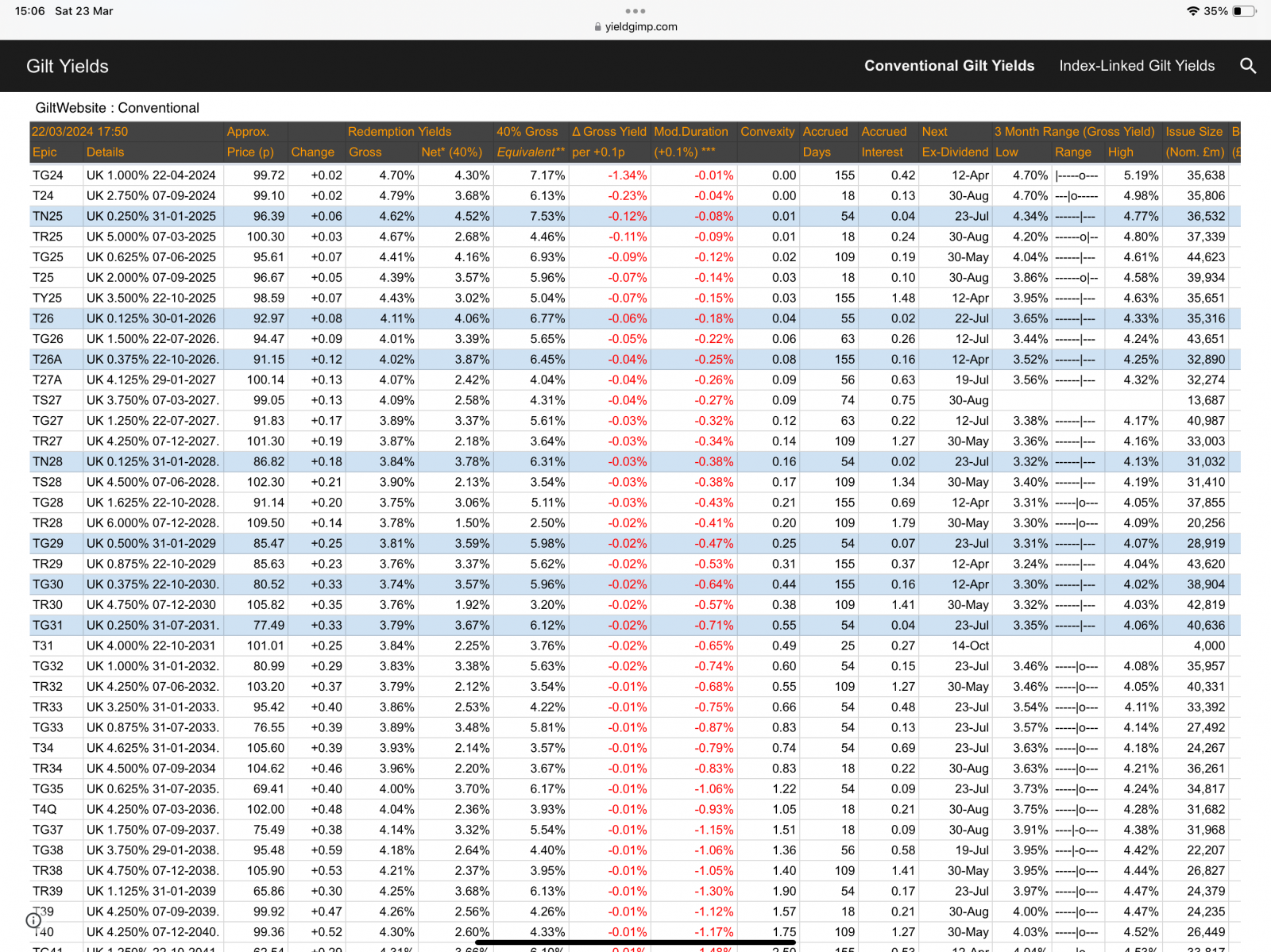

Sorry, I should of been more clear - I am just stating that I need to put money into a Gilt, as I have basically used up my tax free allowance for this year, and by me saying "until the new tax year", I was referring to not wanting to be stung on the amount I have above the £500 interest, getting taxed at 40%.I am also trying to understand Gilts, as this is the first time I am looking into them.From that table above, if I understand it correctly, TG24 would only be until the 22nd of April, and would only make 0.28p?Do all Gilt's pay £100 out at the end date?Is the % in the details column, the coupon value?Given my situation I should look for the lowest possible coupon value, correct?How can I work out what the equivalent % my money will be returning on the end date?I see the "Gross" perecentage column with figures, is that what my return would be, if bought today?What does the "40% Gross" column mean?What are the key items I should read and understand from that table above?Apologies for all the what may seem obvious questions, as I say, this is my first time looking into this, so I want to make sure I understand it all correctly.0

-

Have a read of this

https://www.hl.co.uk/news/what-you-need-to-know-about-buying-government-bonds-gilts

0 -

So for example, if I were to go for TN25, and to keep things more simple, if I put £10,000 in, would that mean:- I buy this for £96.39 per Gilt, then this would give me £100, per gilt, on 31/01/2025, so gains of £3.61 per £100. Meaning I would have £10,361 in my account on 31/01/25?- Regarding the "coupon" part, is the 0.25% on my amount of £10,000? So add £25 to the £10,361? If that is not correct, what part is the 0.25% calculated on?If the above is correct, let's say there is a £5 trade fee, so on my initial £10,000, plus £361, plus £25, minus £5 fee, giving me a total of £10,381, giving a total return of 3.81% on my money? So why does that sheet show 4.62% gross?0

-

Because it isn't a full year until TN25 matures - the returns in the table are annualised.TheDarkKnight93 said:So for example, if I were to go for TN25, and to keep things more simple, if I put £10,000 in, would that mean:- I buy this for £96.39 per Gilt, then this would give me £100, per gilt, on 31/01/2025, so gains of £3.61 per £100. Meaning I would have £10,361 in my account on 31/01/25?- Regarding the "coupon" part, is the 0.25% on my amount of £10,000? So add £25 to the £10,361? If that is not correct, what part is the 0.25% calculated on?If the above is correct, let's say there is a £5 trade fee, so on my initial £10,000, plus £361, plus £25, minus £5 fee, giving me a total of £10,381, giving a total return of 3.81% on my money? So why does that sheet show 4.62% gross?

Did you read Hoenir's link? Including at maturity, coupons are paid every six months and when you buy you'll pay the outstanding accrued interest to the seller so you won't buy them for £96.39, it'll be £96.39 + the accrued interest. You then effectively get it back with the next coupon and you can deduct it for tax purposes.0 -

That makes sense regarding the table being annualised.I did read the link, but I am struggling to fully understand the coupon side of things. Is TN25 100p? I thought every Gilt was £100?If so, 0.25% of £100 being 0.25p. Times that by 100 (£10,000 into £100 (£96.39 buying it at), would mean £25 interest paid to me?Or is it 0.25% on £96.39, being 0.24p. So 0.23p interest per guilt (times 100 based on buying £10,000), so £23 interest?If I can get my head around the above, then the accrued interest owed to the seller can be worked out.When I buy, will it show me exactly what I will get in return, including platform fees, minus accrued interest that I need to pay, plus what I will gain at maturity?0

-

it is 0.25% on £100, half is paid every 6 months.0

-

*gilt, lowercase 'g.' "£100" is the nomenclature. Whenever I've bought them it's been in units of a par value of 100p but really it doesn't matter, it'll be 0.25% per unit on the par value, per year. If you buy 10,000 units @ 96.39p they'll pay 0.25p per unit or £25 p.a., or rather £12.50 every six months (they pay every six months). Like shares, gilts have a bid/offer spread so the actual offer price might be a smidgen above that indicated in the table. At maturity you'll receive 100p per unit (the par value).TheDarkKnight93 said:That makes sense regarding the table being annualised.I did read the link, but I am struggling to fully understand the coupon side of things. Is TN25 100p? I thought every Gilt was £100?If so, 0.25% of £100 being 0.25p. Times that by 100 (£10,000 into £100 (£96.39 buying it at), would mean £25 interest paid to me?Or is it 0.25% on £96.39, being 0.24p. So 0.23p interest per guilt (times 100 based on buying £10,000), so £23 interest?If I can get my head around the above, then the accrued interest owed to the seller can be worked out.When I buy, will it show me exactly what I will get in return, including platform fees, minus accrued interest that I need to pay, plus what I will gain at maturity?

iWeb should tell you the accrued interest you'll need to pay but I doubt it'll work out your return for you, in my experience that's not something that execution only stockbrokers will do.0 -

For simplicity and to make comparisons straightforward. Bonds generally are quoted in nominal terms of £100. The amount that you pay for this £100 of stock will be dependent on the coupon of the stock (i.e. 0.25% or 8.5%) and the current prevailing level of interest rates. Historically bonds used to be traded in round £100 nominal units with a minimum value of £1k for Government Gilts etc.TheDarkKnight93 said:I did read the link, but I am struggling to fully understand the coupon side of things. Is TN25 100p? I thought every Gilt was £100?

Stocks with low coupon yields were issued in the QE era when interest rates were low. As interest rates have risen their market price fell. This has created the window of opportunity for individual UK taxpayers to exploit the CGT advantage gain. Correspondingly higher coupon bonds can trade above par nominal value. Though in both cases the market price will as the redemption date approaches progressively narrow towards par value again.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards