We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Nationwide take over of Virgin Money

Comments

-

Nationwide currently has an excellent CET1 ratio of 26.5%. After the takeover goes through (if it does) the combined group will have a CET1 ratio of 17.6%. Still decent, but potentially having an impact on how much it can lend, which would in turn increase rates.Hoenir said:Explain how the growth in the size of the NW balance sheet has a correlation with higher mortgage rates.4.7kWp (12 * Hyundai S395VG) facing more or less S + 3.6kW Growatt inverter + 6.5kWh Growatt battery. SE London/Kent. Fitted 03/22 £1,025/kW + battery £24950 -

This would only make sense ifSection62 said:If we trust in the Nationwide board that they have found a potential cash cow to increase profits for Nationwide members, then it follows that forum members who are VM customers stand to disbenefit. If Nationwide are going to squeeze the pips of VM to generate all this profit from their non-mutual bank then what does that mean for those of us who have VM products as well/instead?

(a) Virgin Money was currently being run for the benefit of its customers. It isn't, it's a bank; customers don't see the benefit of the bank's profit unless the bank deigns fit to reinvest that profit back in to their products and services.

(b) Virgin Money/Clydesdale Bank customers were to continue indefinitely as second tier bank customers, when every indication is that for most straight-forward savings, mortgage or current account customers the intention will be to move them over to Nationwide - they're just allowing themselves plenty of time to do it.

There's a commission designed to ensure mergers do not lead to a significant reduction in competition in any marketplace. I've seen no indication that they might get involved, but if they do I would suggest both parties are reasonably sure that there will be no issue found.More generally, competition tends to be good for moneysavers, less competition tends to be a bad thing. Much of the discussion on these forums has been about the impact of this deal on Nationwide members, very little about the impact on VirginMoney customers.

This is a non-issue in my view. There are hundreds of competitors for savings and mortgages, their share of the market will not become dominant in either. There are fewer current account providers, perhaps a dozen but again the purchase will still leave them some distance behind both Natwest Group and Lloyds Banking Group in terms of market share.

In addition to my previous points - nobody is beholden to Clydesdale Bank plc. Had the takeover not happened, a billionaire could have bought the bank, held back investment and then asset stripped it.Section62 said:If we trust in the Nationwide board that they have found a potential cash cow to increase profits for Nationwide members, then it follows that forum members who are VM customers stand to disbenefit. If Nationwide are going to squeeze the pips of VM to generate all this profit from their non-mutual bank then what does that mean for those of us who have VM products as well/instead?If the customer doesn't like the way their service provider and/or their ultimate owners treat them, they can move with ease somewhere else. Plenty of noise was made when the business was rebranded about customers being unhappy to see their bank rebranding in support of Branson... the answer was if you don't like it you know where the door is.

This is all totally academic because not once have I seen it suggested that Virgin Money customers stand to disadvantage from being taken over and ultimately integrated in to Nationwide.

Nationwide are not beholden to what you want them to be, and you are not beholden to what Nationwide wants to be. If you don't like it, you can have your say at AGM. If the majority decide to support the board and you don't like that, then leave.Section62 said:I didn't join Nationwide to see it become a building society which exhibits "muscular mutuality". I joined it to get good value financial products.

(or if you like just leave a token £100 in an eligible savings account - don't give up the dream right?)0 -

At the moment Nationwide are beholden to no one (except the regulators), they've got the best of both worlds. If they were a bank they'd be accountable to shareholders. As a (supposedly) mutual they're accountable to members, but thanks to their clever use of a charity donation for every member voting and an easy one click to support the board option it would take something very drastic for their decisions not to be upheld.

The "eligible savings" carpetbaggers argument really doesn't hold - the charitable assignment's been in place for decades and I don't think many members would qualify for a payout on demutualisation. Why would Nationwide ever go that route when they can earn banker's pay without the accountability?4.7kWp (12 * Hyundai S395VG) facing more or less S + 3.6kW Growatt inverter + 6.5kWh Growatt battery. SE London/Kent. Fitted 03/22 £1,025/kW + battery £24950 -

You're completely right, it isn't going to happen, for a whole host of reasons - charitable assignment is just one.Officer_Dibble said:The "eligible savings" carpetbaggers argument really doesn't hold - the charitable assignment's been in place for decades and I don't think many members would qualify for a payout on demutualisation. Why would Nationwide ever go that route when they can earn banker's pay without the accountability?

Most have moved on but there's still some diehards out there, variously seeing demutualisation as somewhere between a possibility and an eventual certainty, as ridiculous as it might seem to you or I.

And yet you think a member vote on the merger might somehow deliver a different verdict?Officer_Dibble said:At the moment Nationwide are beholden to no one (except the regulators), they've got the best of both worlds. If they were a bank they'd be accountable to shareholders. As a (supposedly) mutual they're accountable to members, but thanks to their clever use of a charity donation for every member voting and an easy one click to support the board option it would take something very drastic for their decisions not to be upheld.0 -

We're in the "something very drastic" territory here. If Nationwide thought the deal would be sealed easily by the members they'd have called a meeting immediately.

i doubt very much that a meeting would stop the deal going through, but it would enable the discussion that the board are trying to quash, hold them accountable and make it easier to make them fall on their swords in the highly likely event that the deal doesn't go as well as they hope.4.7kWp (12 * Hyundai S395VG) facing more or less S + 3.6kW Growatt inverter + 6.5kWh Growatt battery. SE London/Kent. Fitted 03/22 £1,025/kW + battery £24950 -

First of all, unless the vote was actually required (and the law is clumsy unfortunately), then they couldn't do that - read Nils Pratley's article for an explanation why.Officer_Dibble said:We're in the "something very drastic" territory here. If Nationwide thought the deal would be sealed easily by the members they'd have called a meeting immediately.

Secondly, timing is absolutely critical in any large scale takeover - the longer things drag on, the more opportunities you leave open for competitors to get their act together and submit a bid. Due diligence is a lengthy and expensive process and there's a competitive advantage to moving fast. Organising and waiting on the results of a member ballot is not a quick process.

So we're back in the lip service category of things. If they don't need to, and the result is a forgone conclusion, what's the point? The vast majority of members don't care about their membership rights/abilities at all. The members who do care even a tiny bit will mostly defer to the board's judgement.Officer_Dibble said:i doubt very much that a meeting would stop the deal going through, but it would enable the discussion that the board are trying to quash, hold them accountable and make it easier to make them fall on their swords in the highly likely event that the deal doesn't go as well as they hope.

You're then left with a small percent of a small percent who are intent on throwing their weight around however fruitless it is or they understand it to be. Why inhibit the business with such nonsense?

4 -

Agree the Standard has taken a much more active interest and challenging position.Officer_Dibble said:It's a shame that MSE haven't put their clout behind the campaign to protect Nationwide members from the financial weakening of their society this deal will bring, or at least to allow them the vote they should be entitled to.

The Evening Standard's more on the ball:

https://www.standard.co.uk/business/nationwide-virgin-money-branson-b1152336.html

"To my mind £2.20 a share is already too much for this ragtag bank formed of various mergers and given a red lick of smiley paint."Some of the press wrote an article in March when the deal was proposed and term agreed - along the lines of ‘members should have a vote’ or ‘unclear why this is a good deal for members’ - but then haven’t written much since (eg FT, Guardian)ThisIsMoney/Dail Mail and the Sunday Times would be the notable exceptions, the latter featuring a graphic with the Nationwide CEO rolling the dice in a casino, where the dice are depicted as houses, surrounded by nervous / anxious onlookers. The Telegraph also wrote a piece last week about the £80m set to be paid out to the professional advisors supporting Nationwide and Virgin Money - including Nationwide spending an estimated £1.4m on PR alone.

The Telegraph also wrote a piece last week about the £80m set to be paid out to the professional advisors supporting Nationwide and Virgin Money - including Nationwide spending an estimated £1.4m on PR alone.

https://www.telegraph.co.uk/business/2024/04/22/city-advisers-80m-nationwides-29bn-virgin-money-takeover/

MSE have now written about the campaign (see link below from Friday), with Martin Lewis promoting the article same day on Twitter.

https://www.moneysavingexpert.com/news/2024/04/nationwide-members-petition-vote-virgin-money/

https://x.com/martinslewis/status/1783871690654560270The campaign appears to be maintaining a list of press mentions of the campaign itself:

https://nationwide-virgin-money-member-vote.org.uk/2024/04/20/press-coverage-for-the-campaign/

… and for the takeover more broadly:

https://nationwide-virgin-money-member-vote.org.uk/2024/04/20/press-coverage-of-the-proposed-takeover-of-virgin-money-by-nationwide/3 -

I think that’s a key issue that’s worth discussing further:WillPS said:

First of all, unless the vote was actually required (and the law is clumsy unfortunately), then they couldn't do that - read Nils Pratley's article for an explanationOfficer_Dibble said:We're in the "something very drastic" territory here. If Nationwide thought the deal would be sealed easily by the members they'd have called a meeting immediately.

- if the board’s opinion changed on a member vote (e.g. the legal advice turns out to be wrong/unsafe, pressure too great, other stakeholders urging board to reconsider etc), i.e. it formed a new opinion that it IS a legal requirement after all, then the takeover code doesn’t prohibit a member vote, as the code is not above the law.

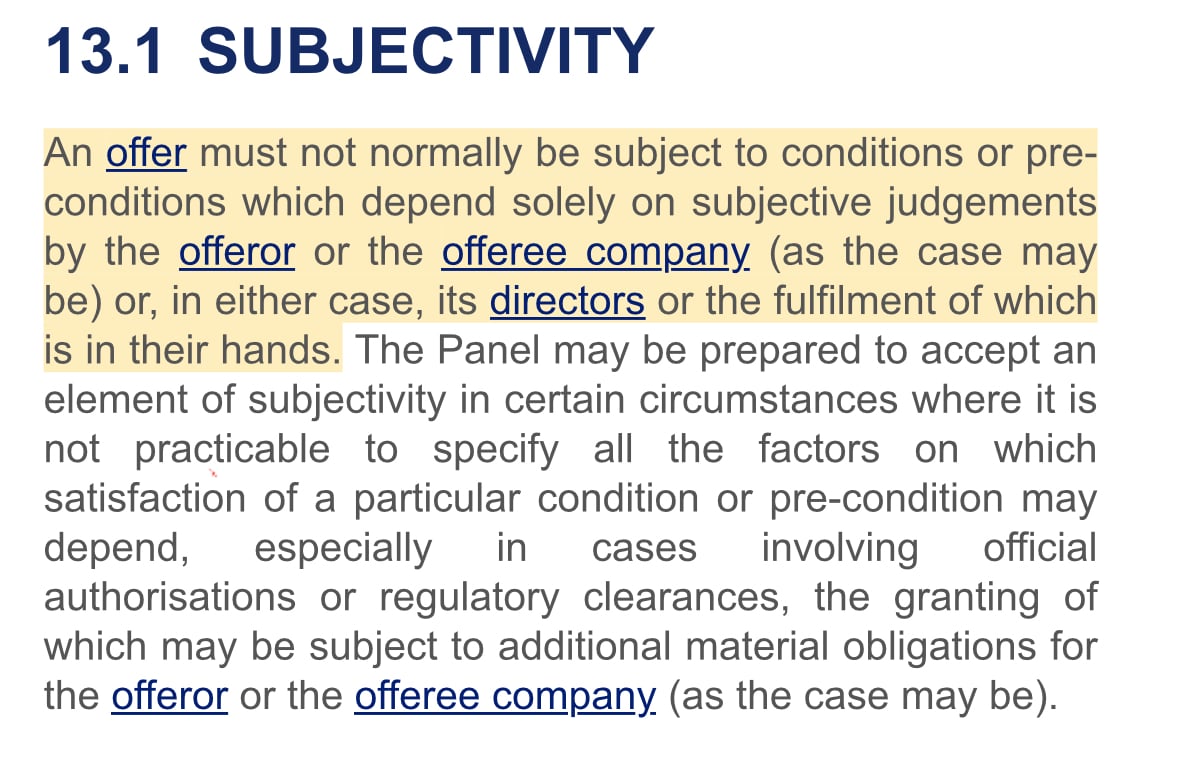

- if the board’s opinion remains that it isn’t legally required, but instead want to offer members a vote anyway, then the takeover code suggests you can’t add subjectivity (Takeover Code 13.1) as conditions to the deal as Nils Pratley suggests: However, there’s clearly some wiggle room / opportunity for interpretation and leeway when you read this part of the code in full. For example, whether a member vote is defined as something that depends “solely on subjective judgements” or whether the Panel is willing “to accept an element of subjectivity” given the circumstances - regulatory clearances being a clear further callout.One could argue that an individual member’s decision has elements of subjectivity in terms of how they decide to vote. But the outcome of that vote, ie the majority of members either accept or reject the deal, is an objective result - it’s a clear pass or fail for the board to consider. And that’s before you even bring into the debate the potential for a regulatory direction on matters.

However, there’s clearly some wiggle room / opportunity for interpretation and leeway when you read this part of the code in full. For example, whether a member vote is defined as something that depends “solely on subjective judgements” or whether the Panel is willing “to accept an element of subjectivity” given the circumstances - regulatory clearances being a clear further callout.One could argue that an individual member’s decision has elements of subjectivity in terms of how they decide to vote. But the outcome of that vote, ie the majority of members either accept or reject the deal, is an objective result - it’s a clear pass or fail for the board to consider. And that’s before you even bring into the debate the potential for a regulatory direction on matters.

The lack of time for a member vote argument is hard to swallow when you consider the minimum timeline to date that was known when the deal was announced:WillPS said:

Secondly, timing is absolutely critical in any large scale takeover - the longer things drag on, the more opportunities you leave open for competitors to get their act together and submit a bid. Due diligence is a lengthy and expensive process and there's a competitive advantage to moving fast. Organising and waiting on the results of a member ballot is not a quick process.

? - deal planning underway

7 March - deal proposed announcement

21 March - offer terms agreed announcement

19 April - scheme convening hearing for VM shareholders (high court date)

22 May - VM shareholders vote on resolution

and scheme (SGM etc)

This suggests to me that Nationwide had over two months to announce and hold a member vote - and probably even longer to prepare for given this deal was in planning before the 7 March announcement. The timeline out to 22 May was predictable from March also, given most of these dates were in the takeover documents published and follow a standard timeline. Regulatory approvals aren’t a given and are unlikely to be quick, which is why it’s been suggested the deal couldn’t complete any earlier than Q4.So we're back in the lip service category of things. If they don't need to, and the result is a forgone conclusion, what's the point? The vast majority of members don't care about their membership rights/abilities at all. The members who do care even a tiny bit will mostly defer to the board's judgement.

You're then left with a small percent of a small percent who are intent on throwing their weight around however fruitless it is or they understand it to be. Why inhibit the business with such nonsense?I think the suggestion that if a vote is/was held it would be a foregone conclusion is a bold one.Yes, Nationwide have only communicated headline positives directly to members with no mention of the costs and risks of the deal, and presented it as a done deal - using language like when and will, not if and would/may etc.Yes, Nationwide members have previously turned out in low numbers and voted overwhelmingly in favour of the board’s recommendation in the past at AGMs.

But given

- the mostly negative press coverage

- the scale of the deal

- the special circumstances

- the importance to the future of the society and the UK

- the fact that Nationwide’s own extensive polling showed that less than half are in favour (despite the Nationwide PR strategy / communication to date), and more than half are neutral / undecided

…that suggests to me that a member vote returning a majority result in favour of the deal is not obvious.If it was a foregone conclusion, I think the board would have held one. The fact that it legally could have done, in compliance with the takeover code, and there was plenty of time, suggests the board isn’t secure in members backing this deal at all.3 -

You've gone from presenting a contrary opinion to the respected business columnist in a "broadsheet" newspaper, which is fair enough in and of itself, to being so convinced that you are right that your contrary opinion (shared and published by nobody of any repute) has by the end of your post become fact. I put it to you that those blinkers are doing your critical faculties a disservice!26left said:

I think that’s a key issue that’s worth discussing further:WillPS said:

First of all, unless the vote was actually required (and the law is clumsy unfortunately), then they couldn't do that - read Nils Pratley's article for an explanationOfficer_Dibble said:We're in the "something very drastic" territory here. If Nationwide thought the deal would be sealed easily by the members they'd have called a meeting immediately.

- if the board’s opinion changed on a member vote (e.g. the legal advice turns out to be wrong/unsafe, pressure too great, other stakeholders urging board to reconsider etc), i.e. it formed a new opinion that it IS a legal requirement after all, then the takeover code doesn’t prohibit a member vote, as the code is not above the law.

- if the board’s opinion remains that it isn’t legally required, but instead want to offer members a vote anyway, then the takeover code suggests you can’t add subjectivity (Takeover Code 13.1) as conditions to the deal as Nils Pratley suggests:However, there’s clearly some wiggle room / opportunity for interpretation and leeway when you read this part of the code in full. For example, whether a member vote is defined as something that depends “solely on subjective judgements” or whether the Panel is willing “to accept an element of subjectivity” given the circumstances - regulatory clearances being a clear further callout.One could argue that an individual member’s decision has elements of subjectivity in terms of how they decide to vote. But the outcome of that vote, ie the majority of members either accept or reject the deal, is an objective result - it’s a clear pass or fail for the board to consider. And that’s before you even bring into the debate the potential for a regulatory direction on matters.

...If it was a foregone conclusion, I think the board would have held one. The fact that it legally could have done, in compliance with the takeover code, and there was plenty of time, suggests the board isn’t secure in members backing this deal at all.

How would Nationwide have put forward a meaningful offer if they had deferred to their members? What would VM shareholders be asked to vote on?26left said:

The lack of time for a member vote argument is hard to swallow when you consider the minimum timeline to date that was known when the deal was announced:WillPS said:

Secondly, timing is absolutely critical in any large scale takeover - the longer things drag on, the more opportunities you leave open for competitors to get their act together and submit a bid. Due diligence is a lengthy and expensive process and there's a competitive advantage to moving fast. Organising and waiting on the results of a member ballot is not a quick process.

? - deal planning underway

7 March - deal proposed announcement

21 March - offer terms agreed announcement

19 April - scheme convening hearing for VM shareholders (high court date)

22 May - VM shareholders vote on resolution

and scheme (SGM etc)

This suggests to me that Nationwide had over two months to announce and hold a member vote - and probably even longer to prepare for given this deal was in planning before the 7 March announcement. The timeline out to 22 May was predictable from March also, given most of these dates were in the takeover documents published and follow a standard timeline. Regulatory approvals aren’t a given and are unlikely to be quick, which is why it’s been suggested the deal couldn’t complete any earlier than Q4.

AIUI, ignoring the subjectivity issue which could well have torpedo'd the whole thing from the start, VM would not be in a position to put the offer terms to their shareholders. That being the case, you are leaving a 2-3 month window for any of Nationwide's competitors to put together a takeover deal of their own.

All to say nothing of the multimillion £ opportunity cost of not getting things done as quickly as possible.

Meanwhile you're misrepresenting the news as being overwhelming negative when it has most been neutral (even when you read the newspaper articles shared by the clown-show campaign as being on their side), and there's even a reasonable amount of favourable coverage coming through.Do your own research reader, a Google News search for "nationwide virgin money" is a good place to start.1 -

Anyone know when I get my free money?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards