We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Insurance company responded late to third party resulting in liability being admitted

I am attaching the final response of the company. I am planning to take matter to ombudsman. Would it be a good idea?

Comments

-

1) Medical evidence will normally be sort however whiplash is now a fixed tariff injury so for example an injury lasting up to 6 months gets £495. If there is clear evidence like CCTV of an action that would cause such an injury it becomes questionable how much you want to be paying in medical report fees to try and reduce the £495. A consultants report can cost £500 and they may deem a supplementary report is required in X months time. Assuming the report supported that some form of injury existed then your insurers would be liable for its costs.thisisme01 said:My car slightly moved towards bus lane (but not completely into the lane) which caused bus to slow from 20mph to 11mph which a passenger claimed they suffered whiplash. Bus company provided CCTV of passenger experiencing a jolt and the front camera footage showing my car slightly moving towards bus lane. My car insurance company reviewed the footage and claimed that I would be at fault and reduced my no claim bonus and put a claim on my insurance. I complained to insurance company but theyMy question is:1) is it standard procedure to request medical evidence in this case or do companies decide without it?2) The car insurance company responded late to the third party which caused liability to be automatically assumed while in previous discussion they mentioned to me that they would deny liability. Could this have resulted in detrimental effect on my insurance? I complained to insurance company that their failure to promptly respond resulting in liability being automatically admitted but they claim that even if they replied in time to deny liability even then the provided CCTV evidence would have resulted in me being liable

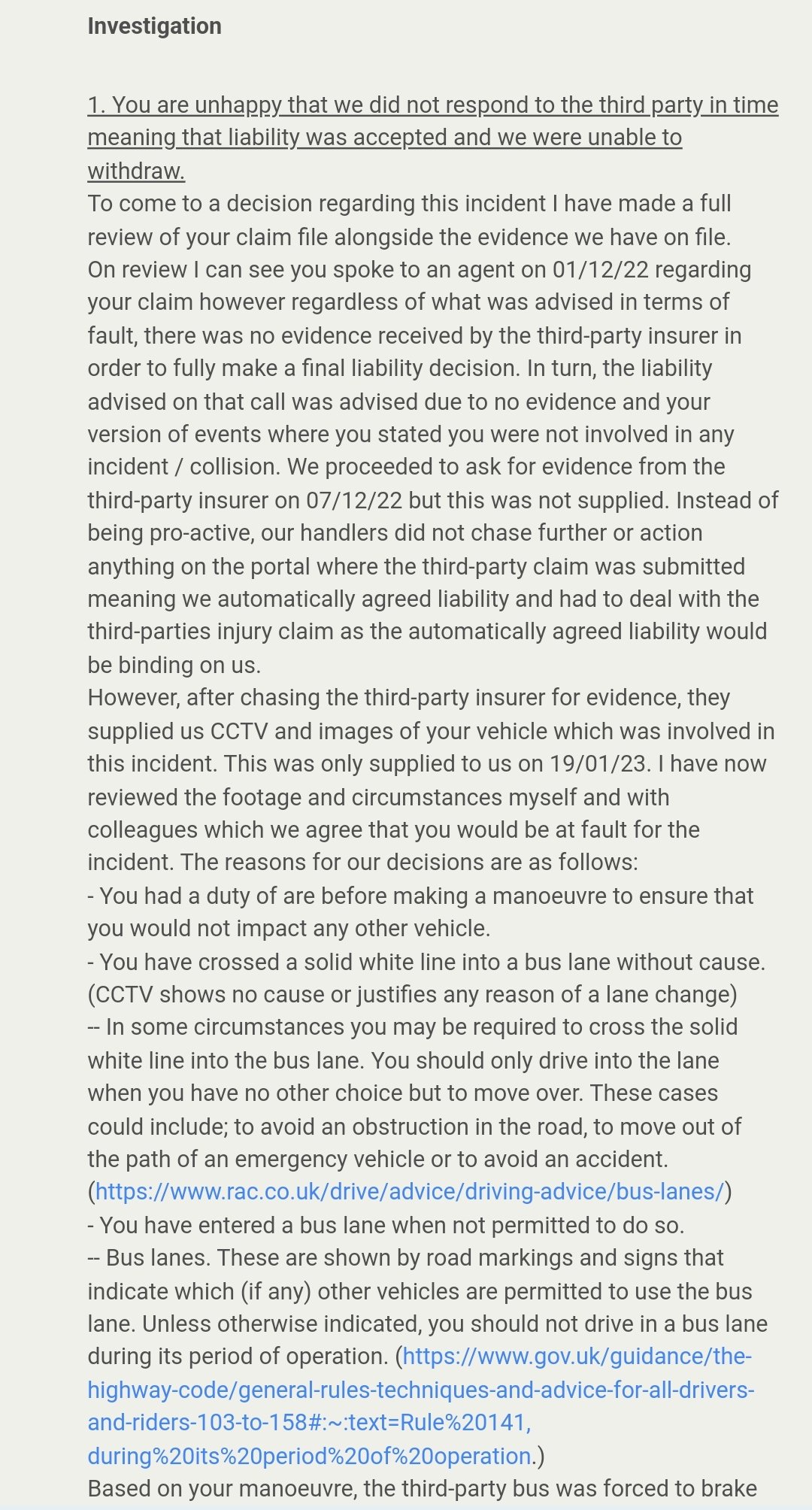

I am attaching the final response of the company. I am planning to take matter to ombudsman. Would it be a good idea?

2) They believe you are liable for the accident based on the CCTV as such it makes no difference if liability was admitted by them after seeing the CCTV or if it was automatic because they failed to update the claims portal in time. At fault isn't differentiated by the mechanism or decision making process that got it there

On what grounds do you think their response is wrong? If your complaint is that you don't think you were liable and their assessment of the CCTV is wrong, that wasn't one of the heads of complaint they have considered and you haven't posted your complaint letter to know if they've missed it or you never raised it.1 -

Thanks for the detailed reply

Over the phone when I spoke with the company representative they said that they would deny liability on the basis that the claimant can provide medical evidence of injury as the speed was only reduced from 20mph to 11mph which would have resulted in a minor Jolt.

After this conversation they failed to update the claims portal in time. I only found this out when I submitted a subject access request and noted conversation of their team.

My complaint wasDear Sirs,

I am writing in reference to the aforementioned claim with claim number xxxxxxxx, lodged in December, concerning a personal injury claim by the claimant purportedly caused by my motor vehicle's alleged attempt to ingress into a bus lane, resulting in the deceleration of the bus speed from 20 mph to 10 mph, thereby purportedly causing the claimant to experience jolting and subsequent impact of her head against the seat in front of her.

On the telephonic communication of 1st December 2022 with a representative from Admiral Insurance, it was communicated that Admiral intended to contest the claim with the claimant's legal representatives, and therefore, would disavow any liability for the alleged incident. The record of the said conversation dated 1st December 2022 also reveals statements to the effect that "they must satisfactorily demonstrate our legal liability in this matter," and that "their chances of success are tenuous at best."

Further, an email communication from the small claims team explicitly stated that "you have recently called us to advise that you did not mean to admit liability but just did not respond within the appropriate timescale", as articulated in paragraph 2, which explicitly avers that "As you did not respond within the 30 working days timeframe, the OIC Portal has now admitted liability automatically", and "You therefore have to deal with the claim regardless"

The case file notes, time-stamped on 18th January 2023 at 10:34 AM, authored by xxx xxx, substantiates this assertion, specifically affirming that "the admission is binding on us - so we will be bound to deal with the claim now as we failed to respond."

The purpose of this complaint is to contend that during the aforesaid telephone conversation, as confirmed by the case file notes, Admiral Insurance did not intend to concede liability and had the intention to challenge the veracity of the claim. However, due to Admiral Insurance's failure to provide a timely response and repudiate liability, as recorded in both the case notes and the email communication from the small claims team, liability was automatically imputed, consequently leading to an unwarranted increase in my insurance premium, an adverse impact on my no-claims bonus and inflicted considerable emotional and psychological distress upon me. Had Admiral insurance promptly responded, the onus of proving liability would have rested on the claimant, thus increasing the evidential buden on the claimant which would have

1) Increased the chances of a favourable outcome of this claim, and

2) Less likelihood of any financial detriments imposed upon me.

In light of the foregoing, I hereby request an impartial investigation into this matter, and I anticipate a timely response to my grievance. Please be advised that I intend to pursue this matter to the fullest extent permissible under the law.

Yours faithfully,

0 -

The insurance company has valued the cost of the claim as 33000

-

The amount of deceleration is not really relevant without a measure of time as well, 20-11 mph over 0.1 seconds (no unreasonable for breaking at those speeds) would result in a force of 4.1g, more than enough to cause whiplash, even if the deceleration took place over 1 second it would still cause .41g, which with whiplash, due to the whipping nature could increase the pressure on the spine to 1.6-2g.thisisme01 said:Thanks for the detailed reply

Over the phone when I spoke with the company representative they said that they would deny liability on the basis that the claimant can provide medical evidence of injury as the speed was only reduced from 20mph to 11mph which would have resulted in a minor Jolt.

That wording seems designed to be deliberately ambiguous, did you move towards the lane, but not enter it, or did you enter the bus lane? If you entered the bus lane then frankly you do not have a leg to stand on, even if it was "not completely into", which would have had to be a fairly severe loss of concentration/control.thisisme01 said:My car slightly moved towards bus lane (but not completely into the lane)0 -

Thanks I haven't got this information as I don't have any recollection of the event and the insurance company said due to data protection they can't share footage with me.MattMattMattUK said:

The amount of deceleration is not really relevant without a measure of time as well, 20-11 mph over 0.1 seconds (no unreasonable for breaking at those speeds) would result in a force of 4.1g, more than enough to cause whiplash, even if the deceleration took place over 1 second it would still cause .41g, which with whiplash, due to the whipping nature could increase the pressure on the spine to 1.6-2g.thisisme01 said:Thanks for the detailed reply

Over the phone when I spoke with the company representative they said that they would deny liability on the basis that the claimant can provide medical evidence of injury as the speed was only reduced from 20mph to 11mph which would have resulted in a minor Jolt.

That wording seems designed to be deliberately ambiguous, did you move towards the lane, but not enter it, or did you enter the bus lane? If you entered the bus lane then frankly you do not have a leg to stand on, even if it was "not completely into", which would have had to be a fairly severe loss of concentration/control.thisisme01 said:My car slightly moved towards bus lane (but not completely into the lane)0 -

That seems slightly odd, purely on the basis that if this "evidence" is being used to demonstrate your guilt, you should have a right to see it. I would ask again and be very specific in requesting the video footage on the basis that if it is evidence you should be able to view it.thisisme01 said:

Thanks I haven't got this information as I don't have any recollection of the event and the insurance company said due to data protection they can't share footage with me.MattMattMattUK said:

The amount of deceleration is not really relevant without a measure of time as well, 20-11 mph over 0.1 seconds (no unreasonable for breaking at those speeds) would result in a force of 4.1g, more than enough to cause whiplash, even if the deceleration took place over 1 second it would still cause .41g, which with whiplash, due to the whipping nature could increase the pressure on the spine to 1.6-2g.thisisme01 said:Thanks for the detailed reply

Over the phone when I spoke with the company representative they said that they would deny liability on the basis that the claimant can provide medical evidence of injury as the speed was only reduced from 20mph to 11mph which would have resulted in a minor Jolt.

That wording seems designed to be deliberately ambiguous, did you move towards the lane, but not enter it, or did you enter the bus lane? If you entered the bus lane then frankly you do not have a leg to stand on, even if it was "not completely into", which would have had to be a fairly severe loss of concentration/control.thisisme01 said:My car slightly moved towards bus lane (but not completely into the lane)0 -

There are a couple of separate questions here...

1) Were you actions negligent when you veered towards the bus lane? Was the bus drivers response to your movements reasonable?

2) Did the resulting deceleration cause and one in the bus injuries and if so what is a reasonable quantum for those injuries?

Bus going from 20mph to 10mph... firstly how have these exact speeds been ascertained? Estimates or from a tacho etc? Secondly, it states that the person hit their head in the process. It's the rate of deceleration that is more likely to cause an injury than the amount of deceleration. Your head hitting a static object tends to be a fairly rapid deceleration!

Your complaint doesn't actually address the first point and that is really what the basis of liability is. You can say you were liable for an accident but deny any losses were sustained.

I would certainly challenge them not being willing to share the external view of the CCTV, its a claim being made against you and you have as much right to see it as your insurers and both have the same GDPR issues. You could apply the same to the internal video but it's more about quantum than liability which isn't the argument here and so pick your fights.

In 99% of cases there may as well be only two options for the value of a claim... £0 or >£0 it makes no difference to you if its £1, £3,300 or £330,000 its all just a fault claim.thisisme01 said:The insurance company has valued the cost of the claim as 33000 -

Thankyou so much ! The comments are really useful. I plan to raise these with ombudsman over the weekend. Would appreciate any tips on how should I frame my complaint for the ombudsman?

0 -

The problem with going to the ombudsman now is your complaint didnt actually cover liability based on actions etc but instead focused on denying any injuries had been sustained. The Ombudsman won't allow you to introduce new elements to your complaint generally, only elements that were in your complaint that the insurer didnt respond to.thisisme01 said:Thankyou so much ! The comments are really useful. I plan to raise these with ombudsman over the weekend. Would appreciate any tips on how should I frame my complaint for the ombudsman?

Acting on behalf of an insurer I have a 100% success rate with the Ombudsman; Acting on behalf of myself its only about 50% which is around the average upheld rate... probably not the person to ask on how best to frame it")

Generally though, keep it to the point and add what necessary but not what's not. I've literally seen complaints mention what they had for breakfast, its hard to get to the crux of a complaint when its 5-6 pages.0 -

That makes a lot of sense. Thanks for this. Would you suggest that I make another complaint to the insurer on the points not mentioned in previous complaint?DullGreyGuy said:

The problem with going to the ombudsman now is your complaint didnt actually cover liability based on actions etc but instead focused on denying any injuries had been sustained. The Ombudsman won't allow you to introduce new elements to your complaint generally, only elements that were in your complaint that the insurer didnt respond to.thisisme01 said:Thankyou so much ! The comments are really useful. I plan to raise these with ombudsman over the weekend. Would appreciate any tips on how should I frame my complaint for the ombudsman?

Acting on behalf of an insurer I have a 100% success rate with the Ombudsman; Acting on behalf of myself its only about 50% which is around the average upheld rate... probably not the person to ask on how best to frame it

Generally though, keep it to the point and add what necessary but not what's not. I've literally seen complaints mention what they had for breakfast, its hard to get to the crux of a complaint when its 5-6 pages.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards