We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

How do you avoid higher rate tax on savings interest

Comments

-

Appreciate all the feedback here it’s really useful. It does seem like each individual step I’ve proposed it entirely legal and proper. For example, HMRC state I can legally decide to transfer an unlimited amount of money to a family member. They also state they can subsequently earn interest on that money and only pay any income tax due.

There doesn’t appear to be anything against the recipient of the money then deciding to gift it back at a future date.

But based on the comments here I can see how HMRC may view this differently down the line.

My only question is how is that tax evasion and not tax avoidance?0 -

eskbanker said:

It's not unusual for people to aim to minimise tax rather than to maximise net return, but of course 100% of nothing is rarely better than 60% of something!lr1277 said:If you don't want to pay tax on the income don't generate an income. There might be savings accounts that pay minimal interest and many current accounts that pay no interest.I don't disagree with you, but it depends on the OP's primary aim.Pay no tax or have an income that keeps up with inflation but that income is then taxable.But if you believe house/asset prices are going down, why do you need a growing asset? In which case an account paying 0% interest might be suitable, if your analysis is assets are going down in value.2 -

Did you not read the post about 'gift with reservation'. Suggest you google the term.saverspavers61 said:Appreciate all the feedback here it’s really useful. It does seem like each individual step I’ve proposed it entirely legal and proper. For example, HMRC state I can legally decide to transfer an unlimited amount of money to a family member. They also state they can subsequently earn interest on that money and only pay any income tax due.

There doesn’t appear to be anything against the recipient of the money then deciding to gift it back at a future date.

But based on the comments here I can see how HMRC may view this differently down the line.

My only question is how is that tax evasion and not tax avoidance?1 -

Perhaps because you would be mis-representing a non-gift as a gift for monetary gain. Which sounds to me like fraud. Other than for a tax benefit how else could you exlpain the purpose of the transactions to the court.saverspavers61 said:Appreciate all the feedback here it’s really useful. It does seem like each individual step I’ve proposed it entirely legal and proper. For example, HMRC state I can legally decide to transfer an unlimited amount of money to a family member. They also state they can subsequently earn interest on that money and only pay any income tax due.

There doesn’t appear to be anything against the recipient of the money then deciding to gift it back at a future date.

But based on the comments here I can see how HMRC may view this differently down the line.

My only question is how is that tax evasion and not tax avoidance?

I am not a lawyer So I suggest you consult your solicitor before proceeding.1 -

Given what I am seeing in the area I wish to make a future house purchase, then I am betting that prices will be lower in a year than they are now. I don’t know that for sure of course but I sold my property at what many consider to have been the peak of prices and I am in my current position as a result of that.lr1277 said:eskbanker said:

It's not unusual for people to aim to minimise tax rather than to maximise net return, but of course 100% of nothing is rarely better than 60% of something!lr1277 said:If you don't want to pay tax on the income don't generate an income. There might be savings accounts that pay minimal interest and many current accounts that pay no interest.I don't disagree with you, but it depends on the OP's primary aim.Pay no tax or have an income that keeps up with inflation but that income is then taxable.But if you believe house/asset prices are going down, why do you need a growing asset? In which case an account paying 0% interest might be suitable, if your analysis is assets are going down in value.

In terms of my primary aim, it’s as simple as this. As a result of the house sale and my current position as a renter, I’m sitting with a usually large amount of cash which I wouldn’t normally have.

I don’t want to tie the funds up in illiquid assets as I may decide to purchase a property much sooner than 18 months should the right opportunity present itself. Easy access savings accounts are also paying some of the best interest rates of recent times.

My predicament, and the reason I made this post, is that while trying to maximise my savings with interest, I’m paying over 40% in tax.It seems entirely reasonable to me to want to minimise the tax burden on any earned interest. While some would achieve this via an ISA, I don’t have that option available for the vast majority of the funds given the ISA deposit limits relative to the amount in question, and I may need access to the funds at short notice.

So my proposal was to take the risk of transferring to someone else, who is both a family member and trustworthy, in order to reduce tax liability.

Focusing purely on the question of tax avoidance versus tax evasion, I’m not sure there’s a definitive answer on that from what I’ve seen so far. I suppose the point is that’s something which would be decided at a future date by HMRC was I to press ahead.0 -

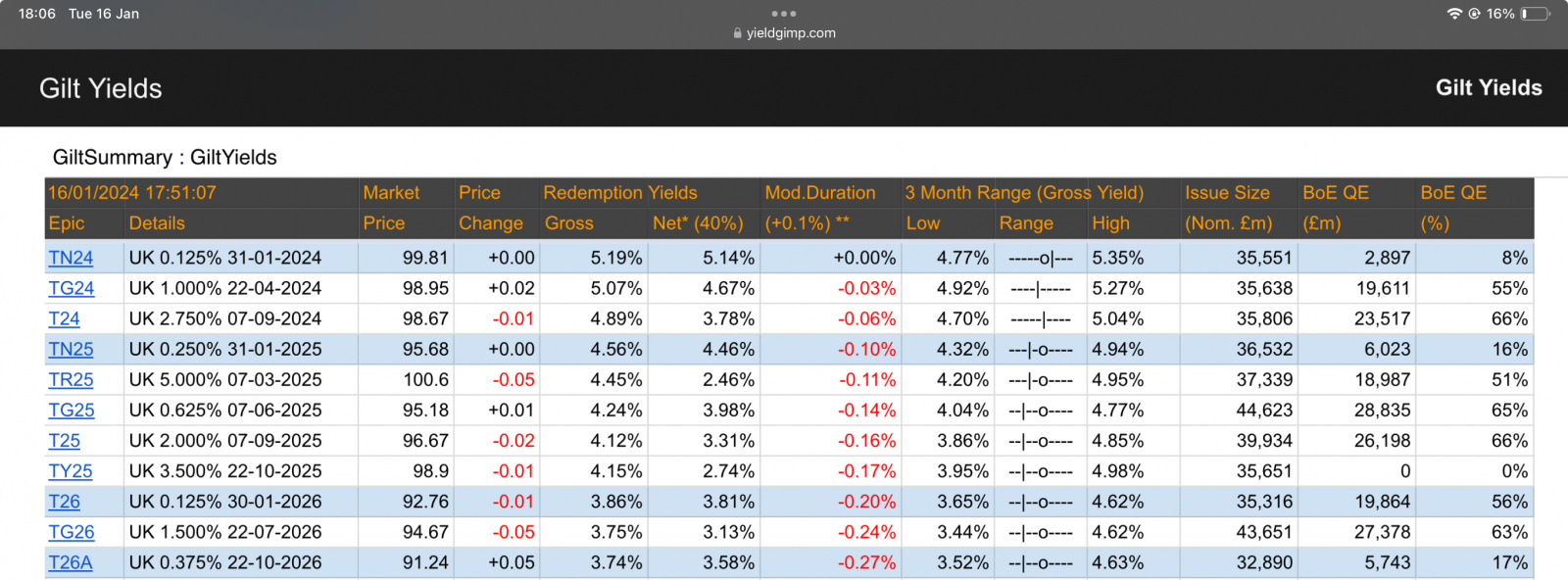

Yes, I scrolled to the end to write this. Try to find a low coupon gilt(s) of the right duration trading below par and hold it to maturity and the capital gain is tax free e.g., TG25 matures in about 18 months from now, TN25 in a year. Just need a stockbroker.phlebas192 said:Take a look at investing in UK gilts. These can be very tax efficient with most of the 'interest' actually being capital gains and there is no capital gains tax to pay on UK gilts. Sorry, I can't post links yet, but it you google "How to buy gilts to beat the taxman on your savings" you should find an article about it on This is Money.Also, if you don't have them already, Premium Bonds for £50k.Mucking around with transferring money to other people is a recipe for disaster.

https://www.yieldgimp.com/4 -

Yes I did thanks. First time I’ve heard of this term after MANY attempts at trying to find an answer to my scenario via HMRC website or Google.BoGoF said:

Did you not read the post about 'gift with reservation'. Suggest you google the term.saverspavers61 said:Appreciate all the feedback here it’s really useful. It does seem like each individual step I’ve proposed it entirely legal and proper. For example, HMRC state I can legally decide to transfer an unlimited amount of money to a family member. They also state they can subsequently earn interest on that money and only pay any income tax due.

There doesn’t appear to be anything against the recipient of the money then deciding to gift it back at a future date.

But based on the comments here I can see how HMRC may view this differently down the line.

My only question is how is that tax evasion and not tax avoidance?It does look to describe my situation quite well. The following paragraphs are pretty relevant.“When there is a gift of money and the money itself becomes property subject to a reservation of benefit, there are a few scenarios in which the taxation rules for reservation of benefit apply.It is possible for a gift of money to fall into the rules, for example if I were to gift £100,000 to an individual and retain access to the account this may fall foul of the rules. Similarly, if the gifted money is invested to earn interest and I receive the interest back, this may also constitute a gift with reservation of benefit.”

Similar to a previous poster in November, I wonder what would be the case if only the original amount of £250,000 was transferred back to me and the interest remained with my parent.

They would get the benefit of the interest and would not be liable for tax due to their low income and personal allowance availability. They also have the funds held in savings accounts in their name.

0 -

There are easy access ISAs, and even fixed-term ISAs have to let you access the money at any point, albeit with interest rate penalties; my first step would be to use this year's £20k, then next year's £20k from April. Also potentially pension (but I realise you want the cash available for a potential house purchase). Premium bonds for another £50k. I'll not get into the wisdom of lending the cash to a relative (but I'd be very reluctant myself).It seems entirely reasonable to me to want to minimise the tax burden on any earned interest. While some would achieve this via an ISA, I don’t have that option available for the vast majority of the funds given the ISA deposit limits relative to the amount in question, and I may need access to the funds at short notice.0 -

Now for the curveball. I’ve actually spoken a financial advisor about this already (the person and company shall remain nameless) and they confirmed that the approach I’ve outlined is entirely legal and allowable.

I didn’t want to say that upfront as it might sway opinion. I don’t think I’ve ever been in a position before where I’ve taken professional advise but just didn’t feel quite right with it. Hence me coming here for a broader opinion.The link to the article on settlements legislation seems very relevant and I’m going to take the time to read in detail before going back to challenge the financial advisors professional opinion.2 -

I think it sounds totally reasonable and within all legal grounds.

Would I give up that much money to save a few grand, not on your nelly.

I won’t put more than 81k in a 5% account, I only risk £50 if bank folds.

250k at 5% = £12,500, - £5,000 tax = £7,500.

You would risk 250k for 5k.

Death of parent, theft by parent, would I trust my dad, without a thought.

Any other family member, no not even with a fiver.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.7K Spending & Discounts

- 247.8K Work, Benefits & Business

- 604.8K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards