We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Interactive Invester SIPP transfer

Comments

-

Has anyone had their cashback yet?0

-

I'm 68, single (divorced with independent adult offspring), retired with full SP and a very small (<£300/pcm) DB pension from brief employment with L&G in my 20s. When I took redundancy in 2018 I opened a SIPP with HL, into which I transferred my tiny DC pension and the redundancy. I've been adding £2880 pa since retiring, and the total held by HL is now about £51k.I've taken the 25% tax-free so my HL account is now in two parts, a drawdown account with £32k - which provided the lump sum, but I haven't taken anything else from it - and a second account with £19k, which my £2880 goes to each year, £14.5k is cash and £4.5k is Fundsmith Sustainable Equity (why? I don't remember). For reasons I really can't articulate, but I probably read something about Fundsmith in the weekend papers, I chose to invest in funds mainly on HL's starred list, but also Fundsmith Equity (not good recently) and Baillie Gifford Positive Change (not good ever). The others are HSBC FTSE 250 Index, HSBC Global Strategy Dynamic Portfolio, and L&G US Index, which has grown more than the rest.With such a small amount I've been paying very little attention to HL's fees, and am only now having that lightbulb moment of realising the managed funds were a seriously bad idea. I'm paying about £11/month for the drawdown account, so I think I should get rid of both the Fundsmith and BG funds and stick to an index fund, as the % fee on those looks really low.With just over £50k I don't think I can get the most attractive rate with Interactive Investor, but if they offer similar investment options perhaps it's still worth leaving HL? What order should I approach this though? Do I tell HL to switch the Fundsmith and BG balances into something like L&G International Index, or Global Equity Index (or an HSBC or Fidelity equivalent, or Vanguard FTSE Dev World Ex UK) first, then switch the final selection to II?I can find my way around the HL app and website without it being too frightening, and I've found them patient and helpful whenever I've needed to ring them, so possibly just reducing fees by changing everything to index funds will discourage me from leaving anyway, but the cashback and TCB incentives have piqued my interest, so to speak!0

-

The cost of index funds will be the same whether you are using HL or II as your platform, so it really comes down to platform costs and functionality.

With a balance of £51k, HL will cost you about £229pa, rising as the balance rises. II would cost £156pa (assuming you have just the SIPP account), but dealing fees might need to be added to that, unless you use their regular investing facility........it's £4 per transaction, but regular investing is free.

A big difference with II is that they do not operate separate drawdown and uncrystallised pots, as HL do.....they apply a notional % split, so in your case, with HL you have a £32k drawdown pot and a £19k (currently) uncrystallised pot, but with II, you'd have a single £51k pot split around 63% drawdown and 37% uncrystallised. In itself, that's not much of an issue, but all your investments are similarly split......you can't have different investments in drawdown and uncrystallised pots. Some might see this as a drawback, others might not bother either way, and some might see it as simpler.......no right or wrong really, you just need to be aware.

1 -

With II, you get a credit of £3.99 per month, which represents one free trade.MK62 said:With a balance of £51k, HL will cost you about £229pa, rising as the balance rises. II would cost £156pa (assuming you have just the SIPP account), but dealing fees might need to be added to that, unless you use their regular investing facility........it's £4 per transaction, but regular investing is free.

1 -

michaels said:

I wonder if they negotiate bulk discount on the fund charges but can't see how that works with ETFs.Albermarle said:These cash back deals are rife at the moment.

It seems crazy that II can offer £1500 to transfer a £250K pension, when they only charge fees of about £20 a month ( do not know the fees exactly ) .

HL will give me £1000 to transfer a £100K ISA, which I will mainly have in ETF's and the max annual charge is £45 pa+ maybe £30 in trading fees.

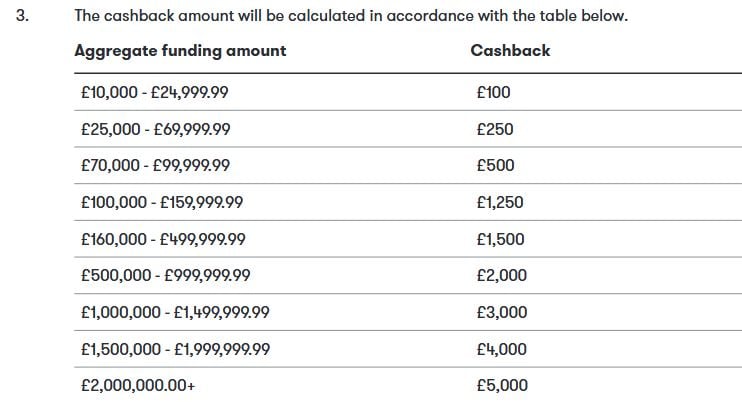

It must be about market share rather than profits.Isn't cashback is less generous this year? 2024 cashback:

2024 cashback:

0 -

Unfortunately, not on the £12.99pm Pension Builder Plan......you need the £21.99pm Investor+SIPP plan for that.Somebody said:

With II, you get a credit of £3.99 per month, which represents one free trade.MK62 said:With a balance of £51k, HL will cost you about £229pa, rising as the balance rises. II would cost £156pa (assuming you have just the SIPP account), but dealing fees might need to be added to that, unless you use their regular investing facility........it's £4 per transaction, but regular investing is free.2 -

MK62 said:The cost of index funds will be the same whether you are using HL or II as your platform, so it really comes down to platform costs and functionality.

With a balance of £51k, HL will cost you about £229pa, rising as the balance rises. II would cost £156pa (assuming you have just the SIPP account), but dealing fees might need to be added to that, unless you use their regular investing facility........it's £4 per transaction, but regular investing is free.

A big difference with II is that they do not operate separate drawdown and uncrystallised pots, as HL do.....they apply a notional % split, so in your case, with HL you have a £32k drawdown pot and a £19k (currently) uncrystallised pot, but with II, you'd have a single £51k pot split around 63% drawdown and 37% uncrystallised. In itself, that's not much of an issue, but all your investments are similarly split......you can't have different investments in drawdown and uncrystallised pots. Some might see this as a drawback, others might not bother either way, and some might see it as simpler.......no right or wrong really, you just need to be aware.Thank you for explaining that, it sounds far simpler to have just the one pot if that's how Interactive Investor would set it up, assuming I'd still be able to take a tax-free amount from the uncrystallised part of it in the future.I've never done any transactions (trades) with HL, other than adding money to the account each year. I put £200/month into a regular saver and when that matures it almost covers the £2880 that then goes into the SIPP. This year's one has just gone into HL and I should get the HMRC top-up around the end of February, the cashback for switching to II is only until the end of January (and only £100 for the small amount I have), so would I even be able to switch it while the HMRC's payment is pending? And should I get the expensive Fundsmith and Baillie Gifford funds moved to a cheaper index fund before switching from HL?0 -

II will set it up that way, and yes, you can take TFLS from the uncystallised percentage of the pot.twiglet98 said:MK62 said:The cost of index funds will be the same whether you are using HL or II as your platform, so it really comes down to platform costs and functionality.

With a balance of £51k, HL will cost you about £229pa, rising as the balance rises. II would cost £156pa (assuming you have just the SIPP account), but dealing fees might need to be added to that, unless you use their regular investing facility........it's £4 per transaction, but regular investing is free.

A big difference with II is that they do not operate separate drawdown and uncrystallised pots, as HL do.....they apply a notional % split, so in your case, with HL you have a £32k drawdown pot and a £19k (currently) uncrystallised pot, but with II, you'd have a single £51k pot split around 63% drawdown and 37% uncrystallised. In itself, that's not much of an issue, but all your investments are similarly split......you can't have different investments in drawdown and uncrystallised pots. Some might see this as a drawback, others might not bother either way, and some might see it as simpler.......no right or wrong really, you just need to be aware.Thank you for explaining that, it sounds far simpler to have just the one pot if that's how Interactive Investor would set it up, assuming I'd still be able to take a tax-free amount from the uncrystallised part of it in the future.I've never done any transactions (trades) with HL, other than adding money to the account each year. I put £200/month into a regular saver and when that matures it almost covers the £2880 that then goes into the SIPP. This year's one has just gone into HL and I should get the HMRC top-up around the end of February, the cashback for switching to II is only until the end of January (and only £100 for the small amount I have), so would I even be able to switch it while the HMRC's payment is pending? And should I get the expensive Fundsmith and Baillie Gifford funds moved to a cheaper index fund before switching from HL?

Personally I wouldn't let the £100 cashback sway the decision......I'd look at that as a small bonus should you decide to transfer. If you transfer, any monies arriving at HL after transfer (tax relief, dividends etc) should be forwarded on by HL.

As to the choice of funds themselves, that's a personal decision.......but you have the choice of selling everything to cash at HL and transferring as cash to II (quicker), or to transfer in-specie, providing II offers the same funds and share classes as HL, but this is often quite a bit slower. The former method has you out of the market for a period, but this can work either way depending on what happens in the market during that period. (as an aside, neither Fundsmith nor the BG fund are my cup of tea atm, but others might view that differently........there's no way to know how either will fare in the future vs an index fund, but such is the nature of investing)

As to whether you should transfer or not, again it's personal decision, but for me it's not clear cut really.....the fee advantages are small atm, though would grow as the pot increases........but if you do decide to transfer, you might as well do it now.1 -

MK62 said:As to whether you should transfer or not, again it's personal decision, but for me it's not clear cut really.....the fee advantages are small atm, though would grow as the pot increases........but if you do decide to transfer, you might as well do it now.

Thank you so much for taking the time to give such a helpful and considered reply (edited to reduce space), I really appreciate it!

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards