We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Lifetime ISA Interest (cross-posted from another forum).

HomeBuyer24

Posts: 4 Newbie

I'm buying a flat and I'm in between exchange and completion. My solicitor has withdrawn the balance from my Lifetime ISA which will be used towards the purchase. I did originally request them to close the account thus claiming any interest that had accrued since April (interest is generally paid yearly), I don't know how much this will amount to by now but is likely to be in the order or hundreds of pounds. My provider originally told my solicitor that they couldn't do it by that route and that I'd have to close the account myself. When I complained they further said that they couldn't close the account at all until after completion in order to report the outcome of the sale to HMRC, and that if I close the account after then that I'd have to pay a penalty (or leave it in there for another 25 years). I'm annoyed about this as I feel that I'm entitled to use the money towards my deposit which is significantly higher than the money that was ever in the account. The interest on the account is less than both the interest on my mortgage and other savings accounts at the moment.

Has anyone else faced this issue and is there a work around?

Has anyone else faced this issue and is there a work around?

0

Comments

-

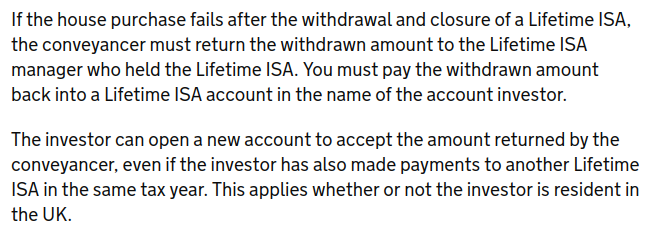

This looks like a provider issue rather than a Lifetime ISA issue. See for example the HMRC advice for ISA managers:

Note: "...after the withdrawal and closure..." and "The investor can open a new account to accept the amount returned..."Let's say you had a £20k balance and a 4% rate, then the accrued interest over 8 months would be £600 and you would lose of that £150 due to the penalty. You could raise a formal complaint about being refused the option to close the LISA to receive the interest penalty free and seek compensation to cover the penalty that will arise from closure of the ISA at the point the complaint is resolved.

Note: "...after the withdrawal and closure..." and "The investor can open a new account to accept the amount returned..."Let's say you had a £20k balance and a 4% rate, then the accrued interest over 8 months would be £600 and you would lose of that £150 due to the penalty. You could raise a formal complaint about being refused the option to close the LISA to receive the interest penalty free and seek compensation to cover the penalty that will arise from closure of the ISA at the point the complaint is resolved.

0 -

Just to note on my other thread, another LISA customer said that she manually closed her account during the sale without problems:One thing I had wanted to know was that if I did that and tried to argue the toss with HMRC over the bonus later, would I only risk the 25% penalty on the interest or jeopardise my HMRC bonuses more broadly. I would be minded to do that as the rate of interest on the account is less than both the interest on my mortgage and the interest I could get on other ISA products on the market. I suspect this would balance out the loss over the time period I would otherwise have to leave it there (LISAs in general offer lower interest than other ISA products, I presume because of the attraction of the HMRC bonuses- which I presume the accrued interest couldn't contribute towards even if transferred over to another provider).

I'm undecided as yet, as to whether to use a LISA for retirement savings. I'm not generally one to turn down a free £1000 but the advice I've seen online is generally lukewarm about this as a means of retirement saving.1 -

Seems very odd for BeeHive to take such an inconsistent approach.There is no arguing the toss with HMRC. If BeeHive have prevented you from operating the account in such a way as to avoid paying the penalty, then they are responsible for compensating you for the penalty. If you don't withdraw, then there is no loss.If you were interested in using a LISA for retirement, then you'd be better off transferring to a S&S LISA. It has its place in limited circumstances, such as where you cannot salary sacrifice (any more money) into a pension and expect to pay basic rate tax on some of your retirement income.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards