We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

The age old 85k question.

Bazzalona13295

Posts: 914 Forumite

A question which hopefully won't take too much time to answer. The 85k that is covered, does this include interest? Not going to get near the 85k (be nice one day) but the terminology I've read is 'customer deposits which can be taken in different ways.

0

Comments

-

I don't believe so. I'm pretty certain it's just £85K, so if you have £85K deposited in a bond, for example, and the bank/BS failed, you would just get you £85K back, not any interest it had earned as well.

1 -

That is how I read it, thanks.Cloth_of_Gold said:I don't believe so. I'm pretty certain it's just £85K, so if you have £85K deposited in a bond, for example, and the bank/BS failed, you would just get you £85K back, not any interest it had earned as well.1 -

Perhaps someone else can confirm but my understanding is that interest that is earned but not yet paid *is* included in the cover up to that £85k so if you deposit, say, £65k in a savings account that pays annual interest and the bank goes under 11 months later you will get your £65k plus 11 months interest.0

-

That's not my understanding, but I could be wrong. I'm under the impression that you get back your deposit plus interest up to £85K to the point of the Bank failure and they aim to pay you within 7 days.

It's £170K guarantee for joint accounts.1 -

Accrued interest is covered, but only if you leave sufficient headroom, which is why it is advisable not to have deposits right up to the limit.FSCS covers money that financial institutions are obliged to pay you, so you are also covered for things like compensation from a Financial Ombudsman decision.

0 -

Thanks for all the replies.

The 85k is a figure I'll not get near but my thinking was if I had say almost 2 years interest on 30k that would be (very roughly) pushing 3.5 - 4k, decent amount to lose if not covered.

It was the wording of 'customer deposit' as interest accrued isn't really applicable to that.0 -

Which financial institution do you think might fail and you have concerns about?1

-

Bazzalona13295 said:Thanks for all the replies.

The 85k is a figure I'll not get near but my thinking was if I had say almost 2 years interest on 30k that would be (very roughly) pushing 3.5 - 4k, decent amount to lose if not covered.

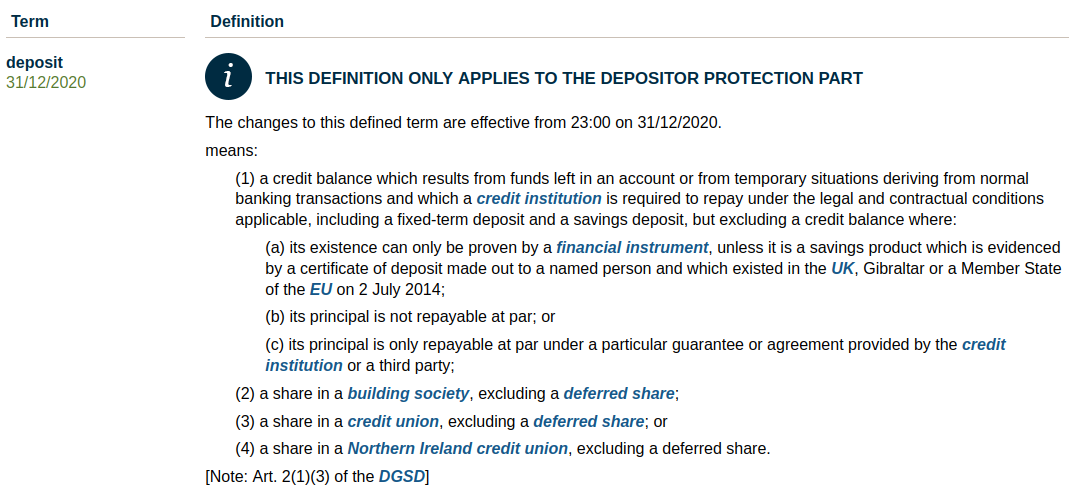

It was the wording of 'customer deposit' as interest accrued isn't really applicable to that.You'd need to turn to the PRA rulebook for the definition of "deposit", which is: So if funds were left in an account for some period of time, the question to ask is what would the institution be obligated to repay the consumer under the contract? For the vast majority of accounts, where interest is calculated daily, interest up to the point the contract was dissolved by the institution would be credited. For fixed term accounts, in practice, the option to have the same treatment was given, along with the option to delay compensation until the end of the fixed term and receive full interest in line with the contract. Though this may depend somewhat on the T&Cs of the specific account.It's important to note, though, that depositor protection is just one limb of the FSCS, which on the whole protects claims of several different natures related to institutions carrying out regulated activities with or without authorisation.1

So if funds were left in an account for some period of time, the question to ask is what would the institution be obligated to repay the consumer under the contract? For the vast majority of accounts, where interest is calculated daily, interest up to the point the contract was dissolved by the institution would be credited. For fixed term accounts, in practice, the option to have the same treatment was given, along with the option to delay compensation until the end of the fixed term and receive full interest in line with the contract. Though this may depend somewhat on the T&Cs of the specific account.It's important to note, though, that depositor protection is just one limb of the FSCS, which on the whole protects claims of several different natures related to institutions carrying out regulated activities with or without authorisation.1 -

Mainly Metro. Not done anything so its hypothetical but I suppose whoever the bank is the same principle apllies.Hoenir said:Which financial institution do you think might fail and you have concerns about?0 -

None.

If a bank was about to fail it's more likely to be taken over.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.6K Work, Benefits & Business

- 603K Mortgages, Homes & Bills

- 178.1K Life & Family

- 260.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards