We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Item lost by Royal Mail, seller only paying out £150 out of the items £700 value

Comments

-

Yes as has been stated many times here there seems to be no legislation on this - or at least none that anyone can find

I believe it is because when a label.is provided the courier is deemed to he acting as the agent of the seller in the return process

No links to back this up but if you find any it will solve one of the big debates on here.0 -

I would have thought this was fairly clear:Olinda99 said:Yes as has been stated many times here there seems to be no legislation on this - or at least none that anyone can find

I believe it is because when a label.is provided the courier is deemed to he acting as the agent of the seller in the return process

No links to back this up but if you find any it will solve one of the big debates on here.

(15) A refund under this section must be given without undue delay, and in any event within 14 days beginning with the day on which the trader agrees that the consumer is entitled to a refund.

https://www.legislation.gov.uk/ukpga/2015/15/section/20/enacted

So, by my interpretation it depends on the T&Cs at point of sale (if they state in the case of faulty goods the goods need to be inspected before a return is accepted), and in the absence of any relevant terms, it depends on the communication from the trader when the customer informs them they're rejecting the goods.

EDIT: From the supporting notes:Subsection (15) requires a trader to provide any refund due to the consumer without undue delay and at the latest within 14 days from when the trader agrees that the consumer is entitled to it. For example, if a consumer rejects goods because of a technical fault which cannot be seen without testing or detailed examination, the 14-day period would start once the trader had carried out the appropriate tests and found the goods were indeed faulty.

In contrast, if it was clear from looking at the goods that they breached the relevant requirement under the Act, there is unlikely to be any reason for the trader not to agree immediately that the consumer is entitled to a refund. In any case, there must be no undue delay, so the trader could not delay payment unnecessarily, for example in order to wait for time-consuming tests which are completely irrelevant.https://www.legislation.gov.uk/ukpga/2015/15/notes/division/3/1/3/4/2

I'm not an early bird or a night owl; I’m some form of permanently exhausted pigeon.0 -

It is (or at least was) possible to edit labels (to commit fraud), I'm not sure tracking itself is always sufficient, I'd expect evidence to be something from the courier with a record of at least the postcode and building number/name which may be on the tracking or on a proof of posting type of receipt.DullGreyGuy said:a photo of the collection note or the link to the tracking after they have dropped it off and the clock starts.

The legislation for cancelling a contract seems to cover this by mentioning (10)(b)DullGreyGuy said:

The legislation gets a bit messy because there's a time limit for refunding but receipt of goods could be after the time limit has ended and yet the merchant is entitled to deduct for excessive handling which could be discovered post the time limit for refund.https://www.legislation.gov.uk/uksi/2013/3134/regulation/34

(9) If (in the case of a sales contract) the value of the goods is diminished by any amount as a result of handling of the goods by the consumer beyond what is necessary to establish the nature, characteristics and functioning of the goods, the trader may recover that amount from the consumer, up to the contract price.(10) An amount that may be recovered under paragraph (9)—(a)may be deducted from the amount to be reimbursed under paragraph (1);(b)otherwise, must be paid by the consumer to the trader.

In the event the consumer has correctly cancelled their contract (rather than using a company policy or rejecting goods) with the CCRs imposing the timeframe for refunding based on evidence provided coupled with a deduction only being permitted for "excessive handling" it would appear the trader carries the risk either way.

With goods being rejected as per the OP, as above noted by Arbitrary, the trader should refund within 14 days of agreeing the goods do not conform, a phone fault is probably something that needs to be inspected. Even if it were a case of someone ordered a black phone and was sent a silver one whether the trader could seek some kind of damages I don't know. You could perhaps say that about damages with the CCRs as well but as above the CCRs are more specific on reimbursement.As to the point in general I've not seen a definitive answer to this issue, it's certainly makes sense that the person paying for the label carries the risk but then the law doesn't always make sense.In the game of chess you can never let your adversary see your pieces1 -

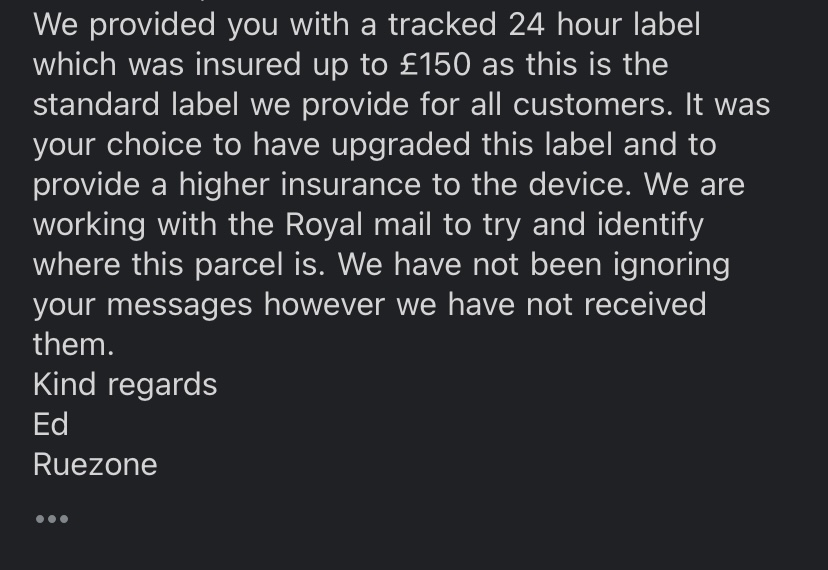

I had emailed them multiple times, asking for them to start an investigation with Royal Mail and to provide me with a resolution, as it was up to them to make sure that the label was fully insured. I received no reply. I then emailed them today threatening a dispute via my bank. And now they seemingly received my email and sent a reply within 20 mins. Lol. This company is a joke. I am going to be opening a dispute with my bank.

0 -

I'm curious, did the return label state it only insured the item for £150.00 or are they trying to pull a fast one?

I'd rather be an Optimist and be proved wrong than a Pessimist and be proved right.0 -

It's irrelevant, but did they offer you an upgraded label or make it clear that the issuance was only to £150 (at your risk) when they provided the label?

I'm just curious - I wouldn't get into a dialogue with them about it at all; just ask them to confirm for the last time they are refusing to refund you and 1. report them to trading standards (won't change anything for you but it'll be noted somewhere on the system) and 2. do a charge back.

I'm not an early bird or a night owl; I’m some form of permanently exhausted pigeon.0 -

If they provide a refund label it is on them to match the insurance to the product value. To me that email is ridiculous back pedalling. It seems they took a chance that most people wouldn’t return the items and the ones that did the items would get to them safely and so need to pay for more insurance. Not a bad calculation as I think insured refunds you pay per label you give rather than per label used. But means that they limit the amount of compensation they can get, but it’s certainly not on you to worry about!Adxmmm said:

I had emailed them multiple times, asking for them to start an investigation with Royal Mail and to provide me with a resolution, as it was up to them to make sure that the label was fully insured. I received no reply. I then emailed them today threatening a dispute via my bank. And now they seemingly received my email and sent a reply within 20 mins. Lol. This company is a joke. I am going to be opening a dispute with my bank.I’d speak to Klarna that would be your best bet. Your bank (if you mean a bank like Lloyds etc) probably won’t help as the transaction they have is with them and Klarna and not with the retailer.I’ve heard mixed things with Klarna, but the following article may help: https://www.klarna.com/uk/blog/regulation-will-take-time-but-protecting-consumers-doesnt-have-to/

The final thing to do is go through the courts to claim the money back. You’d be eligible for small claims which is generally fine for most people. Before you go to court, send a letter before action as this is the final chance for them to come back to the negotiating table. I think you’ve got a good case and in reality if this is a decent sized company who outsources it’s legal issues the law firm will more than likely refund you as it’s not a clear win for them, and lawyers times are expensive and small claims court has no right to claim legal fees back automatically. In most cases lawyers will do some calculation and just pay out as it’ll cost nearly the same even if they win. Of course this option does take some effort; but it depends how much your time is worth to you. For this amount, I’d say it’s worth it personally.1 -

I was looking at the CRA for a different thread, and I think this section is relevant:

i.e. you would have the risk - until you handed the item over to the carrier who was not chosen by you and was commissioned by the trader to deliver the goods (back to them).

That's if you want to keep arguing with them rather than just going for charge back.I'm not an early bird or a night owl; I’m some form of permanently exhausted pigeon.0 -

£150 cover is standard for RM Tracked so the company are probably correct in that aspect.peter_the_piper said:I'm curious, did the return label state it only insured the item for £150.00 or are they trying to pull a fast one?

Passing of risk covers when risks passes from the trader to the consumer (which has occurred), sadly neither the CRA or the CCRs state when risk passes in instances where consumers return goods.ArbitraryRandom said:I was looking at the CRA for a different thread, and I think this section is relevant:

i.e. you would have the risk - until you handed the item over to the carrier who was not chosen by you and was commissioned by the trader to deliver the goods (back to them).

That's if you want to keep arguing with them rather than just going for charge back.

I can only assume you'd have to look towards common law for the answer, I don't know what the answer is and have never seen anything posted to state such with credibility.

Generally speaking, in most cases the person seeking help on here who is actually going to go to small claims would ideally hope 1) their position is correct 2) the company is smart enough to know such and not drag it through small claims.

In instances were 1 doesn't apply(because it's unknown) they'd have to hope the company simply doesn't want the expense of defending.

Whilst small claims is the ultimate option in a situation like this I'm not sure what legal reasoning would be put forward for risk during return being passed upon the parcel successfully being handed over the courier.

Just to add @born_again might confirm but I believe a chargeback would fail as the tracking doesn't show the goods were received by the retailer.ArbitraryRandom said:2. do a charge back.

If OP paid on a credit card they may have S75 cover but ultimately that goes back to above, unless the credit provider knows more than us and agrees OP's responsibility ended once the courier got the parcel.In the game of chess you can never let your adversary see your pieces0 -

Thankfully - in my experience at least, the judges at small claims have quite a lot of discretion and tend to be fairly reasonable (due to the nature of small claims being designed to avoid needing legal representation).Whilst small claims is the ultimate option in a situation like this I'm not sure what legal reasoning would be put forward for risk during return being passed upon the parcel successfully being handed over the courier.

Hence suggesting the argument would be a 'reasonable' person could assume - in the absence of any other contractual term - that the risk is passed on a return in a similar way to the original delivery (especially given the act explicitly states any costs associated with the return are on the trader, so it would be unreasonable to expect the OP to pay out of pocket for enhanced protection).

That's why I was asking the OP earlier if they were informed at any point the return would be at their risk and if they had been given an option to choose an alternative carrier/upgrade the insurance (not that I think it changes the situation materially, but it could be argued the OP should have challenged before posting).I'm not an early bird or a night owl; I’m some form of permanently exhausted pigeon.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards