We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

When you pay tax on savings, just spoken to HMRC

Comments

-

intalex said:

For basic rate tax payers, they paid interest annually by virtue of it being deducted at source. Overall, this would have benefited quite significantly especially if they were borderline basic rate with the annual interest at basic rate, as otherwise under the new rules they would have been taxed 5 years' worth of interest in the 5th (maturity) year having about 4 years' worth of interest taxed at the higher rate just by virtue of all of it arising in the 5th year.masonic said:No, this is not a new thing. Basic rate taxpayers who took out multi-year fixes prior to the PSA would have had basic rate tax deducted at source from interest that may not have arisen until maturity, but the chance of this resulting in a different overall amount of tax being paid was small. The PSA has just caused many more people to pay a different amount of tax due to the already flawed system.Yes, they would have benefitted if they got away with not declaring interest on an arising basis, but they would have been very few in number. Unlike now, where for a 5 year fix you would only need to put in £5,000 as a basic rate taxpayer or £2,500 as a higher rate taxpayer to underpay tax without any intervention.

The additional tax would have been payable through self-assessment, but they would not need to pay anything until after maturity because they could declare the actual interest arising, just as one can do now.intalex said:And higher/additional rate taxpayers paid the basic rate portion via deduction at source and also funded the higher/additional tax on the savings credited in the tax year from their own cash flows well ahead of being able to access any of that interest.

What rule change? Section 370 of the Income Tax (Trading and Other Income Act) 2005 states "Tax is charged under this Chapter on the full amount of the interest arising in the tax year.", but the rules go back further than that, as ITTOIA 2005 was just a rewrite of existing tax legislation "to make it more consistent and understandable" (no joke). So the rule goes back decades. It is not new.intalex said:

Therefore, the rule change is very much a new thing and 100% does change the game for all savers.Editing to address your edit in a previous post:

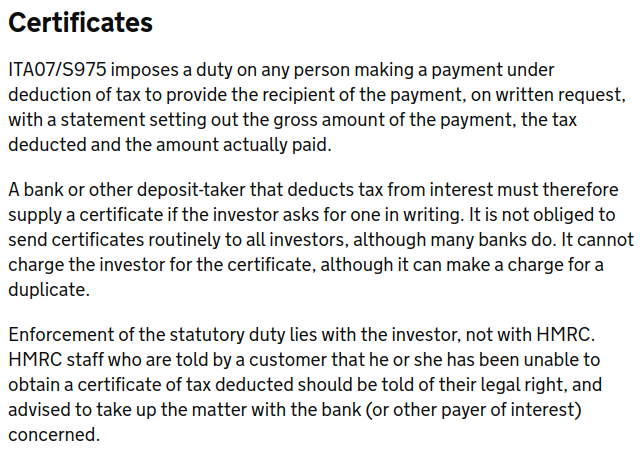

No, the purpose of the tax certificate is to inform the taxpayer how much tax has already been deducted so that they can include this in their tax return. If too much tax was deducted at source, then it would result in them getting a refund when they submit their return.intalex said:EDIT: And the reporting is actually called "Tax Certificate for a Specific Tax Year", so no one can deny that its purpose is to inform taxability for that tax year. This comes from the savings institution, is that the saver's obligation to correct at HMRC's end?

1 -

Hold on, are you saying the pre-PSA rule was also to tax interest on multi-year fixes paying annual interest into the fix, all at maturity? In other words, to comply one had to ask HMRC to repay the tax deducted at source each year and then tax all the interest in the maturity year?masonic said:The additional tax would have been payable through self-assessment, but they would not need to pay anything until after maturity because they could declare the actual interest arising, just as one can do now.

What rule change? Section 370 of the Income Tax (Trading and Other Income Act) 2005 states "Tax is charged under this Chapter on the full amount of the interest arising in the tax year.", but the rules go back further than that, as ITTOIA 2005 was just a rewrite of existing tax legislation "to make it more consistent and understandable" (no joke). So the rule goes back decades. It is not new.intalex said:

Therefore, the rule change is very much a new thing and 100% does change the game for all savers.2 -

So when I had a 7-year fixed rate bond at the end of the 1990s, and tax was deducted at source, officially (to ensure my record was correct) I should have reclaimed the tax deducted each year, and then declared the 6 extra years when the bond matured, and paid tax on it then? Sounds like nonsense to me. I wonder if the "clarification" we see in the HMRC guides relating to the word "arises" was actually there before tax deduction at source ended.

I'm also entertained by HMRC's use of the word "arisen", which seems to be different to a general definition of 'become apparent, appear, come to light' etc that can be found in the dictionary. When interest credited to an account has appeared, or come to light etc, in the list of transactions, it clearly has met this definition, whether or not it is actually useable at that point or at a later date.

1 -

The tax certificate contains (i) the gross interest earned in the tax year, (ii) the tax deducted at source relating to i, and (iii) the net interest "i - ii" credited to the account. Much like a payslip contains gross income, tax & NI deducted and net paid. I'm finding it very hard to believe that the tax certificate's primary purpose is not to report the gross interest (i above) as the taxable income and tax deducted at source (ii above) with both expected to be fed directly into the self assessment to be considered in the overall income and taxation position for that particular tax year.masonic said:Editing to address your edit in a previous post:

No, the purpose of the tax certificate is to inform the taxpayer how much tax has already been deducted so that they can include this in their tax return. If too much tax was deducted at source, then it would result in them getting a refund when they submit their return.intalex said:EDIT: And the reporting is actually called "Tax Certificate for a Specific Tax Year", so no one can deny that its purpose is to inform taxability for that tax year. This comes from the savings institution, is that the saver's obligation to correct at HMRC's end?0 -

The rules around interest arising have not changed. I've previously posted the link to HMRC's site stating where the rule comes from ( https://www.gov.uk/hmrc-internal-manuals/savings-and-investment-manual/saim2440 ) and you can go and access the legislation yourself here: https://www.legislation.gov.uk/ukpga/2005/5/section/370intalex said:

Hold on, are you saying the pre-PSA rule was also to tax interest on multi-year fixes paying annual interest into the fix, all at maturity? In other words, to comply one had to ask HMRC to repay the tax deducted at source each year and then tax all the interest in the maturity year?masonic said:The additional tax would have been payable through self-assessment, but they would not need to pay anything until after maturity because they could declare the actual interest arising, just as one can do now.

What rule change? Section 370 of the Income Tax (Trading and Other Income Act) 2005 states "Tax is charged under this Chapter on the full amount of the interest arising in the tax year.", but the rules go back further than that, as ITTOIA 2005 was just a rewrite of existing tax legislation "to make it more consistent and understandable" (no joke). So the rule goes back decades. It is not new.intalex said:

Therefore, the rule change is very much a new thing and 100% does change the game for all savers.

I can't help you with your second question, because I never would have paid tax at a different rate on an arising basis. I don't think I ever held a multi-year non-ISA fix before about 2015.

1 -

See https://www.gov.uk/hmrc-internal-manuals/corporate-finance-manual/cfm75090intalex said:

The tax certificate contains (i) the gross interest earned in the tax year, (ii) the tax deducted at source relating to i, and (iii) the net interest "i - ii" credited to the account. Much like a payslip contains gross income, tax & NI deducted and net paid. I'm finding it very hard to believe that the tax certificate's primary purpose is not to report the gross interest (i above) as the taxable income and tax deducted at source (ii above) with both expected to be fed directly into the self assessment to be considered in the overall income and taxation position for that particular tax year.masonic said:Editing to address your edit in a previous post:

No, the purpose of the tax certificate is to inform the taxpayer how much tax has already been deducted so that they can include this in their tax return. If too much tax was deducted at source, then it would result in them getting a refund when they submit their return.intalex said:EDIT: And the reporting is actually called "Tax Certificate for a Specific Tax Year", so no one can deny that its purpose is to inform taxability for that tax year. This comes from the savings institution, is that the saver's obligation to correct at HMRC's end?Deposit takers no longer deduct tax from interest, so these have become redundant and some organisations have already phased them out. So it was always about deduction at source. I've never received one in respect of a multi-year fix with no access to interest, so cannot speculate on what figures would have been shown in the intermediate years. Electronic reporting by banks commenced much more recently, so it is unclear whether anything is different between these two.

1 -

S370 just seems to use the word "arisen". It would appear that HMRC have chose to interpret the word "arisen" different to how it is actually defined in the English language.

It's no wonder their staff are in a mess1 -

It is an archaic legal term with a large body of case law behind it. Because of the latter, it has been retained in tax legislation as its meaning is well understood by those in relevant professions. For the avoidance of doubt, I don't count myself among their number. If HMRC are not interpreting it in the correct manner, then this could be challenged in court. But first, HMRC would need to feel someone's collar for underpaid tax.happybagger said:S370 just seems to use the word "arisen". It would appear that HMRC have chose to interpret the word "arisen" different to how it is actually defined in the English language.

It's no wonder HMRC staff are muddled.

1 -

Disappointingly, not by HMRC advisors, which by definition would be the first port of call for taxpayers!masonic said:

it has been retained in tax legislation as its meaning is well understood by those in relevant professions.2 -

I just want to take a moment to thank @masonic for being a real sport in keeping the spirit of this debate healthy and respectful, as it helps some of us gain a clearer picture over the history and context of taxing savings interest. As the discussion goes on the reservations hiding in my gut instinct are also starting to become clearer in my head, especially where I compare the pre- and post- PSA rules and routines. Now back to discussing specific points.

If I understand you correctly, then for multi-year fixes with pay-in (compounding) interest, pre-PSA all tax payers (basic/higher/additional) were supposed to somehow claim back tax deducted at source in the interim years, and then declare (and pay tax on) the full term interest in the maturity year, in order to comply with the definition of "arises" that according to what you stated was the same pre-PSA and hasn't changed post-PSA. The self-assessment forms (both pre- and post-PSA) have provisions to enter interest received gross and interest received net, but no way possible to specify that no interest had arisen (only credited) but that tax had been deducted at source in the interim years - so how could one practically go about claiming the tax deducted at source in the interim years in order to fully comply? I hope you can see that all this is extremely difficult to believe for pre-PSA rules and routines, given that the means to comply to the definition of arisen were simply not provided when tax was deducted at source and have only become feasible when interest started being paid gross.masonic said:intalex said:For basic rate tax payers, they paid interest annually by virtue of it being deducted at source. Overall, this would have benefited quite significantly especially if they were borderline basic rate with the annual interest at basic rate, as otherwise under the new rules they would have been taxed 5 years' worth of interest in the 5th (maturity) year having about 4 years' worth of interest taxed at the higher rate just by virtue of all of it arising in the 5th year.Yes, they would have benefitted if they got away with not declaring interest on an arising basis, but they would have been very few in number. Unlike now, where for a 5 year fix you would only need to put in £5,000 as a basic rate taxpayer or £2,500 as a higher rate taxpayer to underpay tax without any intervention.

The additional tax would have been payable through self-assessment, but they would not need to pay anything until after maturity because they could declare the actual interest arising, just as one can do now.intalex said:And higher/additional rate taxpayers paid the basic rate portion via deduction at source and also funded the higher/additional tax on the savings credited in the tax year from their own cash flows well ahead of being able to access any of that interest.

I have annual certificates available to download via online banking on 2 of my online banks each with 2-year fixes with compounding interest, document titled "Certificate of Interest", showing gross interest earned (i.e. credited) between the tax year dates of 06/04-05/04, states that interest was paid gross and therefore no income tax was deducted, and 1 of the 2 banks states that it's an important document required to complete my tax return. So it's practically the same as before, with gross interest i still specified exactly on the same basis as before (credited not arisen), tax deducted ii is now zero, and so net interest paid iii = i, hence consistent with pre-PSA in terms of information provided and alluding to its relevance in completing tax returns for that tax year.masonic said:Deposit takers no longer deduct tax from interest, so these have become redundant and some organisations have already phased them out. So it was always about deduction at source. I've never received one in respect of a multi-year fix with no access to interest, so cannot speculate on what figures would have been shown in the intermediate years.

If anything, the onus should be on the savings institutions to firstly flag from the outset HMRC's concept of arisen and its tax impact when multi-year fixes are opened with mandatory/optional pay-in (compounding) interest, and secondly their certificates of interest and reporting of arisen interest to HMRC should be aligned accordingly, i.e. no interest reported in interim years and full term interest reported in the maturity year. Unless and until HMRC can get savings institutions to start doing both these things, I'm not sure there are grounds to go after savers who always were and still are simply operating under the clear inference of the annual certificates of interest and (for pre-PSA) the facilities provided through the self assessment form.

4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards