We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Mortgage Redemption penalty advise

Hi, any advice gratefully received 🙏.

In January 2021 my partner took out a 5 year fix with Santander, he ensured this was a portable product as we’d talked about moving in together.

In December 2021 we bought a house together. Prior to buying we ensured I could be added to the mortgage and we could increase the borrowing, Santander agreed and offered us a mortgage in principle, so we based our house choice on this information. However at the last moment Santander informed us that we would be unable to port the mortgage. So we were forced to redeem the mortgage at a cost of £10,000.

We complained to Santander with no success, so took this forward to the Ombudsman, we were also disappointed with the poor customer services and miscommunication with Santander. This was rejected due to Santander T’s and C’s.

We still feel very let down by the process and out of pocket. Is there anything else we can do? 😢

Thank you

Izzy 👍

Comments

-

For what reason? And why were you "forced" to redeem the mortgage?

Porting is always subject to the lender being prepared to issue a new mortgage offer - so if they don't like the property or your finances at the time, it isn't going to happen.2 -

What part of the T&C's did the ombudsman refer to as a reason to side with Santander?1

-

TBH, if you've complained to the Financial Ombudsman Service, and they've rejected your complaint - the only other option would be to take the mortgage lender to court, to claim for breach of contact (or misrepresentation or negligence).

But the Ombudsman is generally more biased towards consumers than a court would be - so it might be a tougher fight.

And you'd need to consider the question... "I presented my evidence to the Ombudsman and they decided against me - so if I presented the same evidence to a court, why would they find in my favour?"

For example... Did the Ombudsman make a mistake about something, and you can explain what that mistake was? Or do you have new evidence?

(And be careful of litigation solicitors who are happy to take your money and fight your case in court - even though they think there's very little chance of you winning in court.)

2 -

Izwiz121 said:

We complained to Santander with no success, so took this forward to the Ombudsman, we were also disappointed with the poor customer services and miscommunication with Santander. This was rejected due to Santander T’s and C’s.

Other posters have asked about the reasons for the Ombudsman's decision....

Is the decision published on the Financial Ombudsman Service's website yet?

If so, do you want to direct people to it, so that they can read it? The decisions are anonymised, so nobody will know who you are.

As a new user you won't be able to post links - but you could just mention the DRN (Decision Reference Number).

Based on what you've said, I've spotted a complaint that sounds a bit like yours - but maybe not quite right. Was this your complaint? https://www.financial-ombudsman.org.uk/decision/DRN-4053254.pdf

1 -

Because our circumstances had changed as we were getting a mortgage together and also because the market had changed. They weren’t obliged to give us a new mortgage offer.Herzlos said:What part of the T&C's did the ombudsman refer to as a reason to side with Santander?0 -

That’s really, really helpful. Thank you 🙏.eddddy said:

TBH, if you've complained to the Financial Ombudsman Service, and they've rejected your complaint - the only other option would be to take the mortgage lender to court, to claim for breach of contact (or misrepresentation or negligence).

But the Ombudsman is generally more biased towards consumers than a court would be - so it might be a tougher fight.

And you'd need to consider the question... "I presented my evidence to the Ombudsman and they decided against me - so if I presented the same evidence to a court, why would they find in my favour?"

For example... Did the Ombudsman make a mistake about something, and you can explain what that mistake was? Or do you have new evidence?

(And be careful of litigation solicitors who are happy to take your money and fight your case in court - even though they think there's very little chance of you winning in court.)0 -

I would have thought that was normal and in keeping, i can't see how the Ombudsman could have ruled any differently.Izwiz121 said:

Because our circumstances had changed as we were getting a mortgage together and also because the market had changed. They weren’t obliged to give us a new mortgage offer.Herzlos said:What part of the T&C's did the ombudsman refer to as a reason to side with Santander?1 -

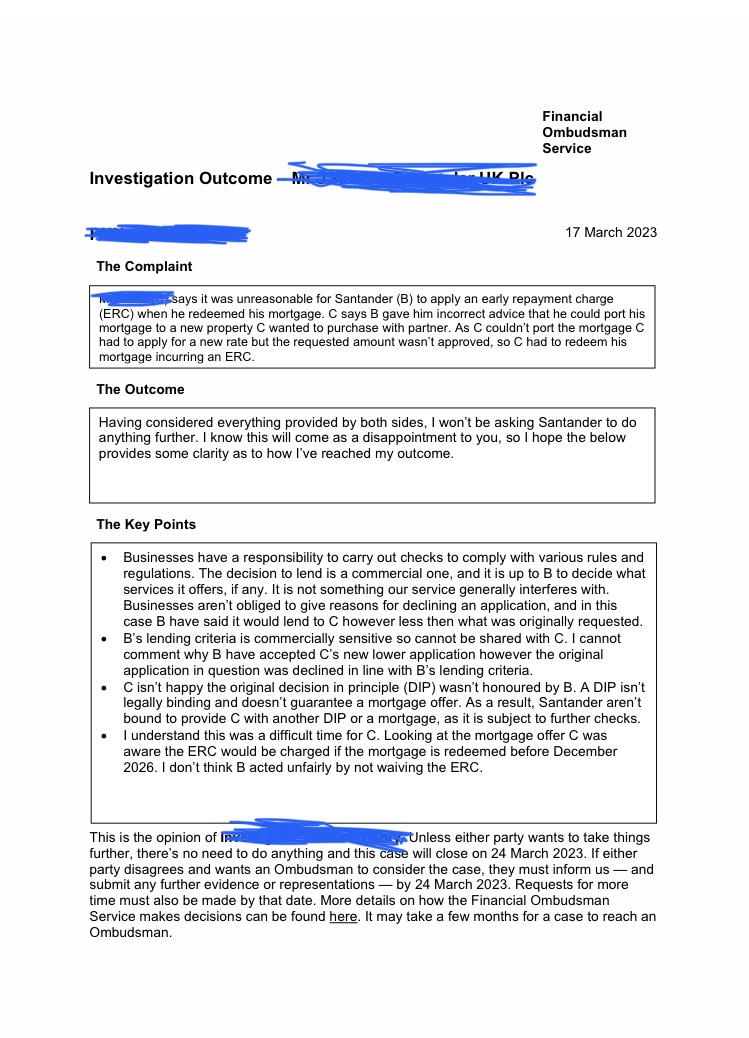

This is the letter from the Ombudsman…

0

0 -

https://www.moneysavingexpert.com/mortgages/porting-your-mortgage/

Does this mean that Santander refused to offer you a joint mortgage for a new property, but some other lender agreed to offer?Izwiz121 said:However at the last moment Santander informed us that we would be unable to port the mortgage. So we were forced to redeem the mortgage at a cost of £10,000.

0 -

I read it as Santander would not port the existing mortgage so it had to be redeemed.

Nothing to say Santander did not offer a new joint mortgage0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.1K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards