We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

LifeStrategy 60 v MyMap 5

Aminatidi

Posts: 650 Forumite

I have around £180K currently sat in FTSE Global All Cap in a Vanguard ISA.

I'm was going to switch in LS60 as having done some soul searching if there is ever a real stress scenario I couldn't handle a 50% drawdown.

There's £125K in an unwrapped account at IWeb in HSBC Global Strategy Balanced and one thought was transfer the ISA from Vanguard to IWeb to minimise platform fees.

I've always taken the view that the Vanguard, BlackRock and HSBC multi-asset funds will always be there or there about for a given risk level.

Anyone have any thoughts on LS60 v MyMap 5 please?

I can only find the top 10 holdings for MyMap but it looks like there's a little less of a UK/home bias there?

I'm was going to switch in LS60 as having done some soul searching if there is ever a real stress scenario I couldn't handle a 50% drawdown.

There's £125K in an unwrapped account at IWeb in HSBC Global Strategy Balanced and one thought was transfer the ISA from Vanguard to IWeb to minimise platform fees.

I've always taken the view that the Vanguard, BlackRock and HSBC multi-asset funds will always be there or there about for a given risk level.

Anyone have any thoughts on LS60 v MyMap 5 please?

I can only find the top 10 holdings for MyMap but it looks like there's a little less of a UK/home bias there?

0

Comments

-

Make it easy and buy a global tracker and a STMMF such as Royal London. STMMF is currently 5% PA. Go 70% STMMF and 30% WORLD TRACKER as a cautious approach . If the market crashes 50% ( which is really a rare event) then your 30% becomes 15%. Remember these crash figures are peak to trough and there's usually a bit of recovery short term anyway. The STMMF is still accumulating in the meantime. If it did crash then you could always rebalance at say every 20% fall in the global market add 5% from the STMMF. You'll be in control much more that way and if it's not going to be life changing sums of money then you're still ticking along.

Chart Tool | Trustnet

You'll not have the volatility of bonds/gilts to deal with either . They're more volatile than you think even in calmer waters.

FsZwd6qXwAImInR (900×561) (twimg.com)

Vanguard UK Gilt UCITS ETF, UK:VGOV Advanced Chart - (LON) UK:VGOV, Vanguard UK Gilt UCITS ETF Stock Price - BigCharts.com (marketwatch.com)

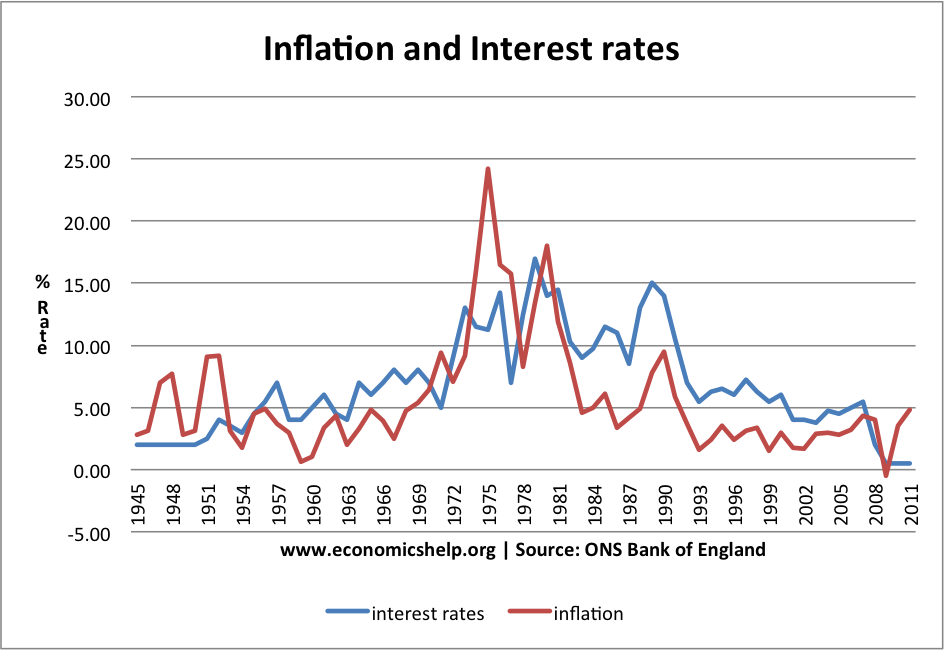

I'll post this one yet again as many say you're losing out in cash. Well most of the time ( source BOE below ) rates have been above inflation. Next year this might be the case in the UK ?

inflation-interest-rates-1945-2011.png (944×650) (economicshelp.org)

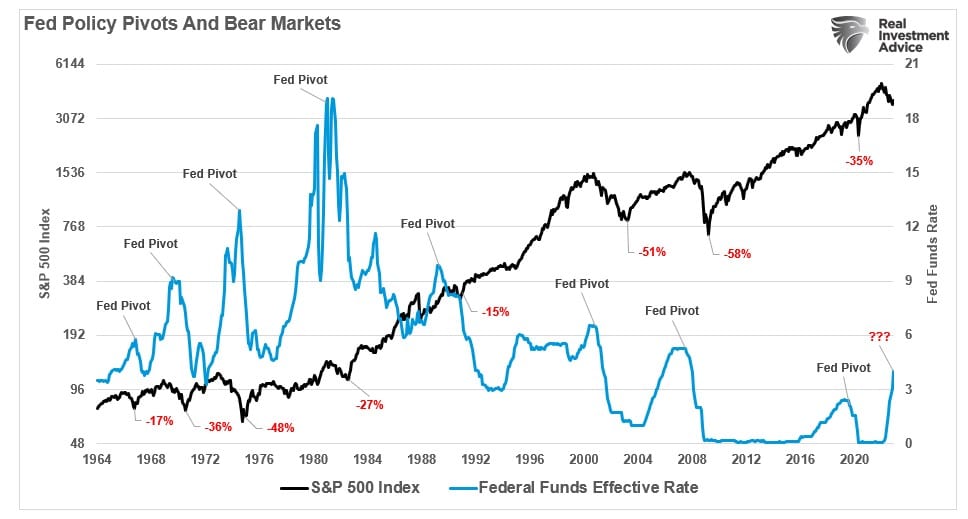

No doubt a gilt/bond fund such as VGOV could replace the STMMF again that's up to the individual. The earlier chart I posted shows US bonds since 1980 clearly there's volatility most years and could be as much as 10%. Why not now as it sounds like the OP doesn't want it ? Well rates have headed higher for a year in a stronger economy than many thought . Idea being to contain inflation that's if the theory works . What if the economy stalls and some kind of recession. Chances are rates will be cut and stock market will fall as history and the data suggests. Bond funds should rise that 10% and maybe more ? Works the other way when rates rise again. Chance you take. Regarding inflation can you really control it ? .Another I've posted .1960 rates from a similar low base are above inflation but it doesn't contain inflation and ends up in double figures. You can only let these things play out. Good luck.

FYDN7BzVUAAsgbc (1200×503) (twimg.com)

Fed-Funds-and-Bear-Markets.jpg (968×519) (realinvestmentadvice.com)

1 -

That is a very appealing idea. But isnt the STMMF still lagging behind inflation? Royal London something like 3.5% YTD where inflation was 4.5%.coastline said:Make it easy and buy a global tracker and a STMMF such as Royal London. STMMF is currently 5% PA. Go 70% STMMF and 30% WORLD TRACKER as a cautious approach . If the market crashes 50% ( which is really a rare event) then your 30% becomes 15%. Remember these crash figures are peak to trough and there's usually a bit of recovery short term anyway. The STMMF is still accumulating in the meantime. If it did crash then you could always rebalance at say every 20% fall in the global market add 5% from the STMMF. You'll be in control much more that way and if it's not going to be life changing sums of money then you're still ticking along.0 -

Qyburn said:

That is a very appealing idea. But isnt the STMMF still lagging behind inflation? Royal London something like 3.5% YTD where inflation was 4.5%.coastline said:Make it easy and buy a global tracker and a STMMF such as Royal London. STMMF is currently 5% PA. Go 70% STMMF and 30% WORLD TRACKER as a cautious approach . If the market crashes 50% ( which is really a rare event) then your 30% becomes 15%. Remember these crash figures are peak to trough and there's usually a bit of recovery short term anyway. The STMMF is still accumulating in the meantime. If it did crash then you could always rebalance at say every 20% fall in the global market add 5% from the STMMF. You'll be in control much more that way and if it's not going to be life changing sums of money then you're still ticking along.I've capitalised the tenses to highlight the issue. Everything was lagging behind inflation in the recent past. Nobody can know the current or future performance vs inflation.The current STMMF return is about 4.8%, but nobody knows what it will be over the next year, neither inflation.1 -

If you want to keep up with inflation you could buy index-linked gilts. Last time I looked, a couple of months ago, they were selling at quite a good price, presumably because the market was expecting interest rates to rise and inflation to fall. I bought some TR24 index-linked gilts, maturing next March, and I reckon I will earn about RPI + 1% (and RPI is usually higher than CPI).1

-

"Why choose bonds":It is not entirely accurate. Bonds are issued at the market price, not a par, but he accurately presents the overall case for buying bonds. The price of bonds has fallen dramatically. Formerly, they were over priced, now they are much cheaper. Private investors typically buy when an asset price has risen and sell when it has fallen. They buy high and sell low. That is a bad idea.

0 -

Thanks all but this seems an answer to a slightly different question

")

I'm asking what views are on MyMap v LS right now.0 -

It does not matter. Just pick one of them.

0 -

I'm not a fan of VLS due to the significant overweighting in the UK. That is not necessarily good or bad depending on your strategy, but it is not what I would want. I don't believe any of the MA fund usual suspects have an appropriate geographical UK representation (haven't looked closely for a while).Aminatidi said:Thanks all but this seems an answer to a slightly different question

I'm asking what views are on MyMap v LS right now.

I have been monitoring BR MyMap for a while and it is one I am considering for a post retirement easier (lazier?) investment strategy. It is one of the newer family of MA funds on the market (obviously BR had/have their 'Consensus' funds), so I am just playing the waiting game atm. HSBC Global Strategy would be my 'go to' MA fund provider at present, although as mentioned I haven't spent a lot of time more recently investigating / reviewing the MA fund sector.Personal Responsibility - Sad but True

Sometimes.... I am like a dog with a bone0 -

Yes I think "strategy" might be pushing it a bit but I've tended to think with LS you're going to end up there or there about as Geoff says above and I really don't intend/want to be trying to "performance chase" here I just to want to pick one and be done with it.

In the General account that is HSBC Global Strategy Balanced.

There's no reason it couldn't be the same in the ISA if I did move it to IWeb but rightly or wrongly something about Vanguard just seems to sit right with me.

Not sure if I'm drinking the kool-aid there though.0 -

There is nothing much wrong with Vanguard, but it may not be the cheapest for you. Nonetheless, if your holding is unsheltered, bear in mind that iWeb, Interactive Investor and Jarvis may follow the others and apply heavy percentage platform fee to OEICs. At least Vanguard has a relatively low cap on their platform fee, and may reduce it in future. (The corresponding account is free in the US.)Aminatidi said:

There's no reason it couldn't be the same in the ISA if I did move it to IWeb but rightly or wrongly something about Vanguard just seems to sit right with me.

0

https://www.youtube.com/watch?v=kY7Wjct28jU

https://www.youtube.com/watch?v=kY7Wjct28jU

{kind=link}

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards