We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Reported for missed payment & 100 points down mid Mortgage application. Stresslevel 1000

Lisli

Posts: 2 Newbie

Hi all!! Really new Newbie here

I was reported for a missed payment on a Insurance payment without the creditor following legislation procedure.

I missed a payment on a Friday, on Monday they sent a Default Letter by post and by Wednesday they has already reported me to the Credit Agencies for a missed payment, all of this without me even having received the letter they sent me. The letter came of the Friday, 3 days after they reported me. I was completely unaware of the missed payment. My credit score went down by 100 point in the middle of a mortgage application process. I am stressed beyond belief and rather angry that they can do this without informing me nor offering me to remedy the missed payment BEFORE reporting me. :'(

I rang and complained they admitted that they send bulk report to Credit Agencies mid month and those that have missed payments days prior to mid month reporting date are therefore clearly at a huge disadvantage and not to mention at the mercy of Royal Mail efficiency. They said that the report stands and that its only a missed payment and not a default, still, I am now 100 points down and a victim to their administrative calendar. IMO.

They said that the report stands and that its only a missed payment and not a default, still, I am now 100 points down and a victim to their administrative calendar. IMO.

My point is: How can I read and take action upon a letter I have not yet received?

Needless to say I am going to challenge the hell out of this, so have you successfully done something similar? Please note this is not a default as they successfully retook Direct Debit payment 13 days after missed payment which is within the 14 day threshold. But this is a warning to you all to change your DD date so you don't end up like me. 100 points is extremely severe for a missed payment, so please watch out or change your DD date right now!!

Any knowledge on the this? I need amo for my complaint letter

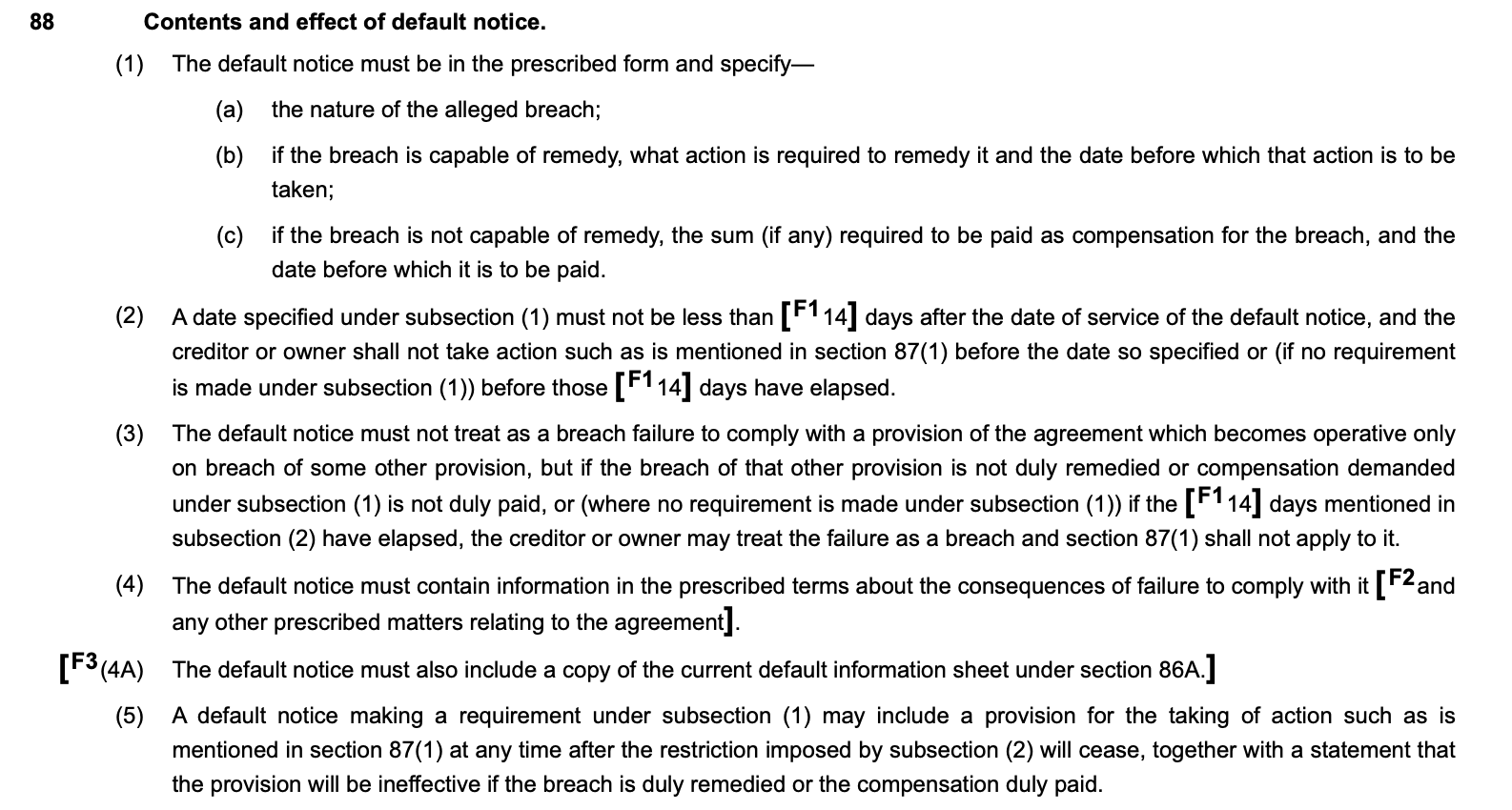

I enclose a screenshot of the Legislation form the Consumer Credit Act that they use Section 87, they but I have added Section 88 of the legislation which I understand refers to a procedure and timeline that they have to comply by. How do you read it? Please help save my sanity.

I was reported for a missed payment on a Insurance payment without the creditor following legislation procedure.

I missed a payment on a Friday, on Monday they sent a Default Letter by post and by Wednesday they has already reported me to the Credit Agencies for a missed payment, all of this without me even having received the letter they sent me. The letter came of the Friday, 3 days after they reported me. I was completely unaware of the missed payment. My credit score went down by 100 point in the middle of a mortgage application process. I am stressed beyond belief and rather angry that they can do this without informing me nor offering me to remedy the missed payment BEFORE reporting me. :'(

I rang and complained they admitted that they send bulk report to Credit Agencies mid month and those that have missed payments days prior to mid month reporting date are therefore clearly at a huge disadvantage and not to mention at the mercy of Royal Mail efficiency.

My point is: How can I read and take action upon a letter I have not yet received?

Needless to say I am going to challenge the hell out of this, so have you successfully done something similar? Please note this is not a default as they successfully retook Direct Debit payment 13 days after missed payment which is within the 14 day threshold. But this is a warning to you all to change your DD date so you don't end up like me. 100 points is extremely severe for a missed payment, so please watch out or change your DD date right now!!

Any knowledge on the this? I need amo for my complaint letter

I enclose a screenshot of the Legislation form the Consumer Credit Act that they use Section 87, they but I have added Section 88 of the legislation which I understand refers to a procedure and timeline that they have to comply by. How do you read it? Please help save my sanity.

0

Comments

-

Stopped reading after the thread title. The 3 digit score is irrelevant and not seen by any lender and not used in credit decisions. At all.2

-

You seem to be confusing the requirements for applying a default notice, which has not been applied to your credit record, with a missed / late payment marker which has been likely correctly applied. Why did the payment fail / you did not make the payment ? When going through the mortgage process you need to be on top of anything likely to damage your file.

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

1 -

Lisli said:100 points is extremely severe for a missed payment,

LOL. It's no more severe than 1 point or a billion points.

One missed payment is not the end of the world. Your timing could have been better, but it's a good reminder for you to ensure payments are made on time.

The missed payment marker is correct, as it reflects you missing the payment.

3 -

OK, to try and ease your stress levels.Point 1, you can safely ignore the drop in your score - it forms no part in any lending decision, and in fact is not even visible to a lender.Point 2, you've have a missed/late payment reported, not a default. This is an accurate statement of the facts, so you have no grounds on which to challenge it. Yes, it's perhaps unfortunate timing it terms of when it happened in relation to the lender's reporting cycle, but there's no point in crying over spilt milk. And bear in mind that most lenders have different reporting cycles (i.e. when they send their data to the CRAs). Some are monthly, some are weekly, some are mid-week, some are end of calendar month, etc. etc. So it's pointless trying to game the system by changing your DD date anyway.Point 3, whilst it's obviously less than ideal, a single late payment marker in an otherwise well-managed credit history will have a negligible effect. Lots of late payments, a default, a CCJ, those would severely hamper your chances of obtaining further credit. An isolated incident - barely even worth worrying about.1

-

You are quoting the wrong legislation, you received a default sums in arrears letter, not a default notice, two very different things.

As others have said, one late payment is neither here nor there.I’m a Forum Ambassador and I support the Forum Team on the Debt free wannabe, Credit file and ratings, and Bankruptcy and living with it boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.For free non-judgemental debt advice, contact either Stepchange, National Debtline, or CitizensAdviceBureaux.Link to SOA Calculator- https://www.stoozing.com/soa.php The "provit letter" is here-https://forums.moneysavingexpert.com/discussion/2607247/letter-when-you-know-nothing-about-about-the-debt-aka-prove-it-letter2 -

Just to clear things up I had a late payment letter which instructed me that a re-take of the DD payment would be taken a few days later. The second DD was taken successfully. However in the same letter (4 Pages) I had a Default Notice, which explained what the procedure would be should I not make payment on the second DD. As per legislation they included the "Default Notice" in the envelope in anticipation that the second DD wouldn't be successful. That way they kill two birds with one postage stamp. However this created mixed signalling in my opinion. 1/ You will be fine if you do as we say 2/We will take action.

The reason I missed payment is because I have an injury making me unable to walk for long nor work for the last two months, so I guess I was not aware of the late payment as I was busy confined to a chair in agony 24/7. Despite this I am up to date with all bills, apart from the missed payment. I believe that if the procedure for the severer Default Notice is two weeks before action, how does the same it not apply for a missed payment? It appears that company policies are only upheld if they themselves sit inside legislation. Secondly there is no way I can read a letter before I receive it and then find out that they have taken action anyway by reporting it.

Further to that Experian and Equifax both stipulate that a late payment should not be reported before 30 days have passed, in my case it was 3 working days.

Anyway, I will take this a learning curve, I shall comply with the majority perception of how things are and stay in my lane........not! I will still challenge it.

Thank you for your answers, I appreciate it!

0 -

You've been looking at the American sites.Lisli said:

Further to that Experian and Equifax both stipulate that a late payment should not be reported before 30 days have passed, in my case it was 3 working days.

Another step on the learning curve.2 -

What you believe is irrelevant, they are different things. Your payment was late, that is a fact, they reported that fact.Lisli said:Just to clear things up I had a late payment letter which instructed me that a re-take of the DD payment would be taken a few days later. The second DD was taken successfully. However in the same letter (4 Pages) I had a Default Notice, which explained what the procedure would be should I not make payment on the second DD. As per legislation they included the "Default Notice" in the envelope in anticipation that the second DD wouldn't be successful. That way they kill two birds with one postage stamp. However this created mixed signalling in my opinion. 1/ You will be fine if you do as we say 2/We will take action.

The reason I missed payment is because I have an injury making me unable to walk for long nor work for the last two months, so I guess I was not aware of the late payment as I was busy confined to a chair in agony 24/7. Despite this I am up to date with all bills, apart from the missed payment. I believe that if the procedure for the severer Default Notice is two weeks before action, how does the same it not apply for a missed payment? It appears that company policies are only upheld if they themselves sit inside legislation. Secondly there is no way I can read a letter before I receive it and then find out that they have taken action anyway by reporting it.

Further to that Experian and Equifax both stipulate that a late payment should not be reported before 30 days have passed, in my case it was 3 working days.

Anyway, I will take this a learning curve, I shall comply with the majority perception of how things are and stay in my lane........not! I will still challenge it.

Thank you for your answers, I appreciate it!

Take it as a learning point, chalk it up to experience and move on. You made a mistake, even in the middle of a mortgage application it likely makes little difference unless you were incredibly marginal in the first place, it will make no difference in a few months provided you do not do the same again, with a small amount of time lenders do not care about minor administrative errors, they are looking for patterns.

Finally, if something like this causes you to experience stress and anger at the levels you appear to have experienced, please consider getting help from your GP and/or other medical professionals.1 -

Keep a spreadsheet of your regular payments and check it every few days; or put them into your calendar and set an alert for the day before so that you make sure funds are available to cover the payment. Takes about 2 minutes.0

-

Maybe a bank account which both pre-warns of a DD payment going out and then confirms it has gone out. That way you will know to check you have the funds in place so that you don't get missed payments.

I have a pot with my bank that I load the money into (automatically) to cover DD's and they are then taken from that ring fenced pot.

Sounds like a similar setup would work for you if your unfortunate injuries do not allow you to concentrate for periods of time and having as much automated as possible would work better.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards