We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Drawdown pot

RodMaximus

Posts: 4 Newbie

Just looking for opinions, I have had my pension pot with SJP since around Covid outbreak, just bad timing, as we have all had disastrous years, and seen our funds dwindle, then the war, my question is, my funds are still down from my original investment, some two years on, my question I guess, is are we all in the same boat? Is this going to be a long haul, or do you see recovery, obviously with interest rates high, and high inflation, we are losing money, quit or stick it out?

Be grateful for opinions.

1

Comments

-

RodMaximus said:... my funds are still down from my original investment, some two years on, my question I guess, is are we all in the same boat?It all depends on how you've invested your funds.Looking at a middle-of-the-road 60% equity fund like VLS60, it's up about 8% vs. the immediate pre-COVID value.What are you invested in?RodMaximus said:Just looking for opinions, I have had my pension pot with SJP since around Covid outbreak,The other drag on your funds is platform fees and adviser charges. SJP aren't generally considered to be a low-cost provider.How did you choose them, vs. any of the other options?N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1 -

SJP are eye wateringly expensive. You're probably paying somewhere between 2.00% and 2.50% in fees annually. This is pretty bad when markets are shooting up, even worse when markets are pretty stagnant, which they have been for the last couple of years.

While most funds have been disappointing in the time period you have been invested the best way to get better returns is to move to a provider which doesn't charge such high fees. I believe SJP charge an exit fee if you are with them for less than 5 years, so bear this in mind if you do plan to leave. It might be worth waiting until there is no exit fee.1 -

@RodMaximus I think you have a previous thread on the same subject:

https://forums.moneysavingexpert.com/discussion/6451021/drawdown-pension-fundsIn that thread, various helpful people were asking who you were invested with and what your funds were. Now you've said that it's SJP, your poor performance makes a little bit more sense.Do you know what funds your advisor has invested your money in?N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.0 -

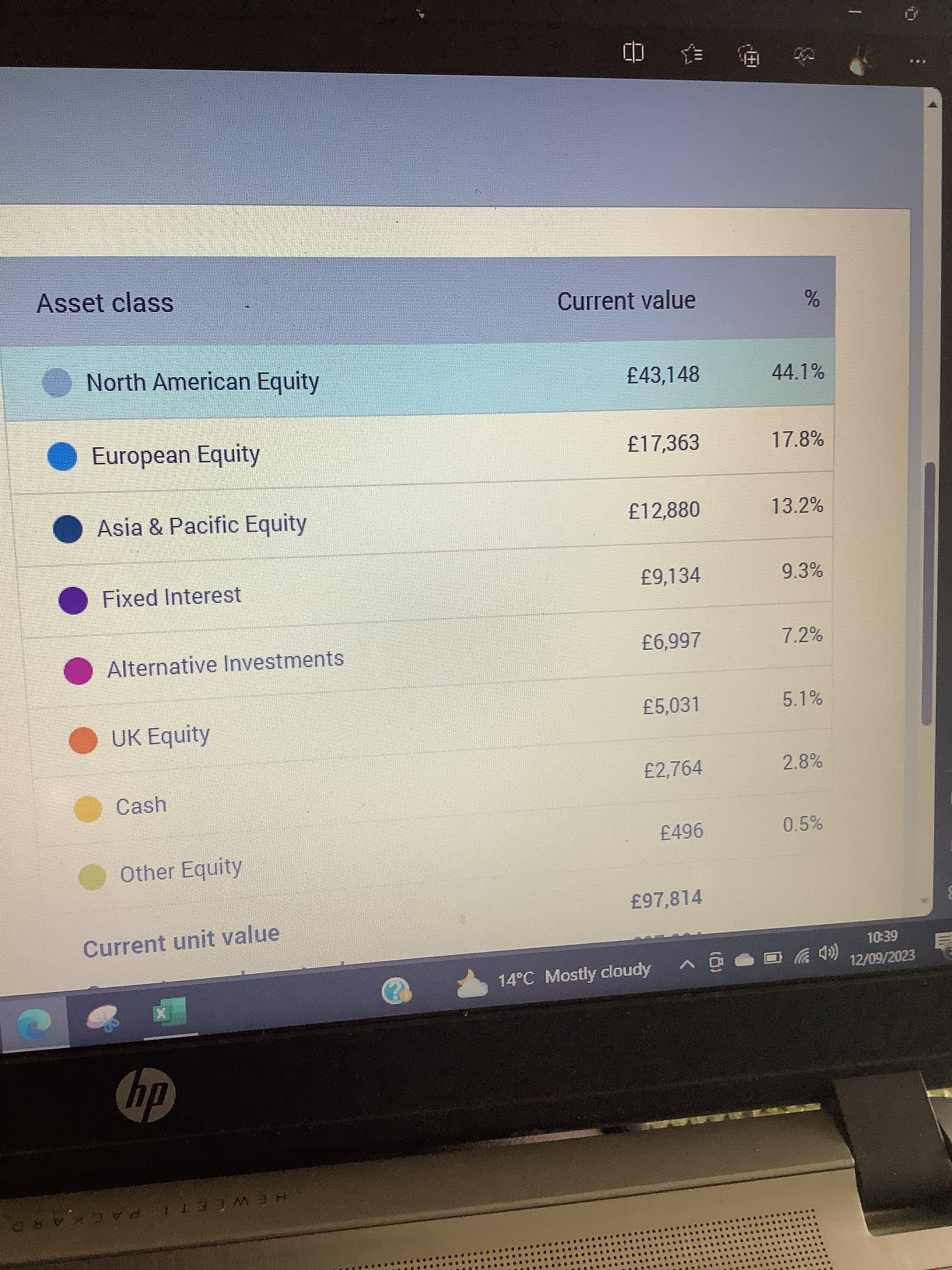

Hi QrizB thanks for reply, doesn’t sound like your are keen on SJP, love to have more detail on that, but looking at what funds,,will this picture be enough info?

0

0 -

RodMaximus said:Hi QrizB thanks for reply, doesn’t sound like your are keen on SJP, love to have more detail on thatSJP have a reputation on this forum for high fees and mediocre performance. I'm sure your advisor has a nice car, a posh office and treats you like royalty - all the while skimming his cut from your investments no matter how well or poorly they perform.

That's about 80% equity, so a higher risk mix than the VLS60 fund that I mentioned earlier. It's more like VLS80, which is up roughly 15% since the pre-COVID days.RodMaximus said:... looking at what funds,,will this picture be enough info?N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 35 MWh generated, long-term average 2.6 Os.1 -

It’s also going to depend on what you mean since “around the Covid outbreak”. If you entered those funds right at the top of the market you would see worse numbers on performance to date. The exact date can have a big effect0

-

Below is a review of SJP by a well respected channel, Pensioncraft:

https://www.youtube.com/watch?v=F-UP-XDUPWM

https://www.youtube.com/watch?v=F-UP-XDUPWM

It is a few years old now, but as you have requested some more information I think you will find it very interesting.Think first of your goal, then make it happen!2 -

Here's something more recent on SJP:

0 -

If the figures shown in JohnWInder link are accurate to OP's product then OP is paying circa 1.35% for something they could get for 0.8% with open market advice and 0.2% - 0.3% without. Annual costs as % pot value. £1350/£800/£300 on 100k.

Ignoring initial and exit one offs on which the difference is amortised over many years. And exit can be 0 anyway a few years after contributions stop.

Nonetheless it is £600 pa or £50 pcm too much. Forever. Per 100k.

It's a good business model for somebody. SJP in this instance but they are one of many and amazingly not the most expensive either. Just a big in the UK well known one who get a regular kicking in the Times.

With pension investments - consider the analogy of Audi for VW group. Functionally the same as other options.

Built from the same parts bin (underlying sector/geo equities and bond funds). Carry you and family to destination (saving for retirement pension pot). But *price* for this and the velben good and branding aspects is not the same. And people will react to that in different ways. Recoil in horror at the price or respond to the targeting.

Advice

The question beyond cost is whether the "financial advice", prompting on family affairs, tax guidance, handholding vs market events/investment education is being delivered to OP's expectations and a realistic take on time spent per year for fees paid.

And if this advisor is being proactive in the choices they make about their time - with this customer at their pot size. Do they get support in a useful way or are they neglected to regulatory minimums until they call. And how treated when they do.

Are they trusted by OP based on advice and guidance received to date. That financial advice relationship has a value if so. Or it may be further source of disappointment (due to neglect) if OP is outside the sweet spot for target clients.

Product

My subjective opinion is that mainstream portfolio shapes overcomplicated and obfuscated by SJP don't carry enough value to deliver against their additional cost. And that your speculative investment risk gets juiced up and the net fees position drops back closer to market returns. So you get little "alpha" net fees. And take a bit more risk to pay them first before you get your market return. The incentive to land it not far off market (with occasional upside surprises) is obvious. To avoid people leaving the profitable milking shed - this is the outcome which suits them.

If these products regularly and sustainably outperformed market total return indices and low cost funds which track them they would market that heavily and provide data supporting that claim. The silence is deafening.

The cost is the cost. The alpha you don't seem to get much of is what it is.

The advice is the advice.

Bottom line

It's not the product vs passive market performance.

Or even the excess cost drag.

It's whether you find value in this current advice relationship. Or you don't.

You may tolerate the costs for a while if so. If you don't then do something else - just not with a tied wealth manager next time around.

Watch out - according to the Economist this week - the big global investment banks are all poised to expand into this lucrative low regulated capital requirements wealth management market. Not sure how many will bother with the UK but much hilarity incoming if so

1 -

‘Quit or stick it out’ what’s the alternative? we’re all in the same global market so continue to invest in equities for the long term as this has shown to show growth over the long term. Consider controlling variables such as platform and fees but otherwise set and forget.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.8K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.2K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.4K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards