We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Bonds vs Equities

Comments

-

I'm not sure I agree that companies that pay dividends are "different". A good quality business is a good quality business. If a company retains it profits and reinvests in new products or sales outlet expansion, such as Apple, then over the long term the share price will increase as the future profits from those endeavours are added to the market valuation. A high dividend payer, such as British American Tobacco that releases profits to shareholders will see its long term share price reflect the distributions.Linton said:

I believe you are mistaken because the type of companies that pay good dividends are different in kind to those that aim for high growth. For evidence see what happened in the tech boom and crash around 2001. Whilst the global indexes were collapsing Woodford’s high income funds continued as if nothing had happened to provide good returns.GazzaBloom said:

But if you look at capital + divs taken is that any different to selling off some capital from an index fund? The total value has to be the same if divs are just a distribution of a company's profits rather than them being retained. Divs are just forced on you and reduce the stocks capital value, selling an index is no different except you choose when to take the "dividend".Audaxer said:

That's true. I'm retired and have an income portfolio which includes some of the 'dividend hero' ITs. It isn't 100% equities as it also includes a couple of bond funds. I have been wondering recently if I really need the bond funds, and whether I should sell them and put the proceeds into the equity income ITs. I've not decided yet but think I'd be okay with the increased volatility.jimjames said:

Although if you have income producing funds in your portfolio especially those that have maintained their dividends over decades then I suspect it might be less of an issue if the market drops as your income is less linked to the current market price. I maybe should have added that the portfolio composition may well change at retirement even if it remains 100% equities.Linton said:

Yes, it all depends on your requirements. When you are looking purely at the long term and do not need your investments to maintain your current standard of living 100% equity could well be right for you. However as you approach and pass retirement age with limited guaranteed income long term returns are likely to decrease in importance as you focus more on how you manage your finances in the meantime.jimjames said:100% equity here and has been for the last 25+ years. I don't see that changing anytime soon.

Or am I mistaken?

Also receiving dividends is a different experience for the investor to having to extract money from a collection of predominantly growth funds. The income investor receives a pretty stable ongoing income without any need to continual decisions on what to sell just to maintain your day to day expenditure. Dividends are much less volatile than capital values. With income investing you can simply ignore capital value volatility.

From my experience the best answer is both dividends and sake of capital. Use dividends for ongoing income to a significant extent like an annuity and use sale of capital for one-off major expenditure and as part of strategic management.

Dividends are not magic free money, they are profits from business that are either retained as value within the business for future use or distributed to shareholders, or a mix of both.

In the short term both the high dividend stock and no dividend stock may be affected by the popularity, sentiment or black swan events and vagaries of the stock market but long term a good quality company is a good quality company and will deliver a good total return whether via dividends or capital share price expansion.

I do take the point that in a sudden market downturn that income returns through dividends can offer real comfort vs deciding whether to sell down capital or not and it's something I am thinking about when moving from accumulation to decumulation.1 -

Woodford’s funds that performed spectacularly well during the tech crash of the 2000’s were unit trusts investing in dividend paying UK shares. Dividend paying Unit trusts/OEICs must pay out all the dividends they receive.Prism said:

Those investment trusts muddy the water though. Some do invest in high dividend payers but many other do not and invest in the same mix of companies that other funds use. They can constuct their own dividends by selling capital or holding actual dividends back and reinvesting them to sell later. Any investor can achieve the same themselves by selling capital and combining with a dividend if required.Linton said: I believe you are mistaken because the type of companies that pay good dividends are different in kind to those that aim for high growth. For evidence see what happened in the tech boom and crash around 2001. Whilst the global indexes were collapsing Woodford’s high income funds continued as if nothing had happened to provide good returns.

Some higher dividend paying investment trusts (ITs have much more freedom) do base their dividends on growth investments, but I think that is a small number, the only one I know that does is EAT. More I think will smooth out dividends. In either case such funds will presumably choose their underlying investments with the objective of supporting their financial management strategy. I doubt they simply run a global tracker in parallel with a cash buffer.You could do the same if you put in sufficient time and effort, but surely that is true of most funds. One advantage of using a number of funds is diversification, you are not dependent on a single implementation of a single strategy. For that reason I take my investment income both directly from a portfolio of income funds and via a cash/lower risk buffer funded by ad hoc rebalancing with more growth oriented investments. The intention is that under no circumstances will long term investments be sold to directly support short term expenditure.2 -

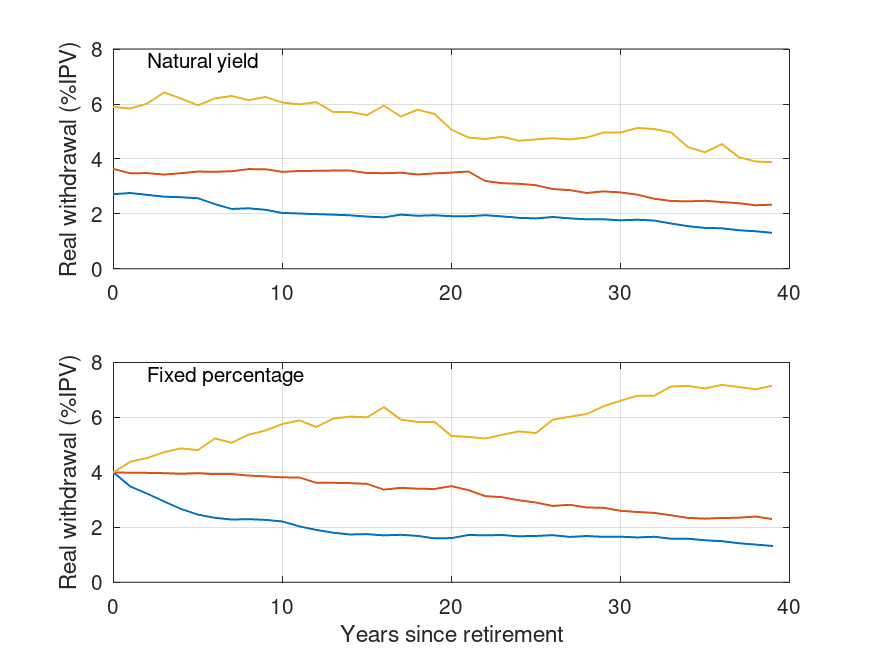

While a proper (i.e. extended) comparison of dividend funds and growth funds is difficult (largely because the historical values from more challenging times don't tend to be available), for someone invested in 50/50 mix of the FTSE100 (or historical equivalent) and UK bonds and cash, the difference between taking natural yield or a fixed percentage of the portfolio (the latter is not constant inflation adjusted withdrawals) is illustrated in the following figure (returns and yield data from 1872-2019 are from macrohistory.net, 40 year rolling periods have been used, fees and taxes have been ignored) where the three lines are, from the top, 90th percentile, median, and 10th percentile.Linton said:

I believe you are mistaken because the type of companies that pay good dividends are different in kind to those that aim for high growth. For evidence see what happened in the tech boom and crash around 2001. Whilst the global indexes were collapsing Woodford’s high income funds continued as if nothing had happened to provide good returns.GazzaBloom said:

But if you look at capital + divs taken is that any different to selling off some capital from an index fund? The total value has to be the same if divs are just a distribution of a company's profits rather than them being retained. Divs are just forced on you and reduce the stocks capital value, selling an index is no different except you choose when to take the "dividend".Audaxer said:

That's true. I'm retired and have an income portfolio which includes some of the 'dividend hero' ITs. It isn't 100% equities as it also includes a couple of bond funds. I have been wondering recently if I really need the bond funds, and whether I should sell them and put the proceeds into the equity income ITs. I've not decided yet but think I'd be okay with the increased volatility.jimjames said:

Although if you have income producing funds in your portfolio especially those that have maintained their dividends over decades then I suspect it might be less of an issue if the market drops as your income is less linked to the current market price. I maybe should have added that the portfolio composition may well change at retirement even if it remains 100% equities.Linton said:

Yes, it all depends on your requirements. When you are looking purely at the long term and do not need your investments to maintain your current standard of living 100% equity could well be right for you. However as you approach and pass retirement age with limited guaranteed income long term returns are likely to decrease in importance as you focus more on how you manage your finances in the meantime.jimjames said:100% equity here and has been for the last 25+ years. I don't see that changing anytime soon.

Or am I mistaken?

Also receiving dividends is a different experience for the investor to having to extract money from a collection of predominantly growth funds. The income investor receives a pretty stable ongoing income without any need to continual decisions on what to sell just to maintain your day to day expenditure. Dividends are much less volatile than capital values. With income investing you can simply ignore capital value volatility.

From my experience the best answer is both dividends and sake of capital. Use dividends for ongoing income to a significant extent like an annuity and use sale of capital for one-off major expenditure and as part of strategic management.

The spread in values is fairly similar for poorer retirements (i.e., median and below), while the spread in the upside is much greater for the fixed percentage approach (but this comes at the expense of a greater reduction in capital). In other words, it doesn't matter that much between using either natural yield or a fixed percentage of the portfolio when investing in the same things. However, one big difference is the initial withdrawal rate - clearly this is the same for all retirements when using the fixed percentage approach but depends on prevailing dividends and bond yields when using natural yield.

The argument between growth or dividends/value is a different one and not one I'm going to pursue.

Finally, the amount of income volatility that retirees can tolerate is a function of expenses and income (including guaranteed income) as well as personal preference. For example, a couple with full state pensions and a £100k initial portfolio, might expect their natural yield income from the above graph to vary between 21+2=23k and 21+6=27k, i.e. about 20% variation from peak to trough. For a couple with full state pension and a £1m portfolio, their income might vary from 21+20=41k to 21+60=81k, i.e. a 100% variation from peak to trough.

1 -

I dont think a 50/50 equity/bond ratio is necessarily a good idea for income investing. The problem is inflation - very broadly, all other things being equal, given sufficient time etc etc one would expect dividends to increase with inflation. On the other hand natural bond income is fixed from the time you buy the bond by definition. In any case until very recently natural bond income was derisory unless one used higher risk corporate bonds which could have been problematic. I am not yet sure about how best to use safe bonds now that interest rates are at sensible levels.OldScientist said:

While a proper (i.e. extended) comparison of dividend funds and growth funds is difficult (largely because the historical values from more challenging times don't tend to be available), for someone invested in 50/50 mix of the FTSE100 (or historical equivalent) and UK bonds and cash, the difference between taking natural yield or a fixed percentage of the portfolio (the latter is not constant inflation adjusted withdrawals) is illustrated in the following figure (returns and yield data from 1872-2019 are from macrohistory.net, 40 year rolling periods have been used, fees and taxes have been ignored) where the three lines are, from the top, 90th percentile, median, and 10th percentile.Linton said:

I believe you are mistaken because the type of companies that pay good dividends are different in kind to those that aim for high growth. For evidence see what happened in the tech boom and crash around 2001. Whilst the global indexes were collapsing Woodford’s high income funds continued as if nothing had happened to provide good returns.GazzaBloom said:

But if you look at capital + divs taken is that any different to selling off some capital from an index fund? The total value has to be the same if divs are just a distribution of a company's profits rather than them being retained. Divs are just forced on you and reduce the stocks capital value, selling an index is no different except you choose when to take the "dividend".Audaxer said:

That's true. I'm retired and have an income portfolio which includes some of the 'dividend hero' ITs. It isn't 100% equities as it also includes a couple of bond funds. I have been wondering recently if I really need the bond funds, and whether I should sell them and put the proceeds into the equity income ITs. I've not decided yet but think I'd be okay with the increased volatility.jimjames said:

Although if you have income producing funds in your portfolio especially those that have maintained their dividends over decades then I suspect it might be less of an issue if the market drops as your income is less linked to the current market price. I maybe should have added that the portfolio composition may well change at retirement even if it remains 100% equities.Linton said:

Yes, it all depends on your requirements. When you are looking purely at the long term and do not need your investments to maintain your current standard of living 100% equity could well be right for you. However as you approach and pass retirement age with limited guaranteed income long term returns are likely to decrease in importance as you focus more on how you manage your finances in the meantime.jimjames said:100% equity here and has been for the last 25+ years. I don't see that changing anytime soon.

Or am I mistaken?

Also receiving dividends is a different experience for the investor to having to extract money from a collection of predominantly growth funds. The income investor receives a pretty stable ongoing income without any need to continual decisions on what to sell just to maintain your day to day expenditure. Dividends are much less volatile than capital values. With income investing you can simply ignore capital value volatility.

From my experience the best answer is both dividends and sake of capital. Use dividends for ongoing income to a significant extent like an annuity and use sale of capital for one-off major expenditure and as part of strategic management.

The spread in values is fairly similar for poorer retirements (i.e., median and below), while the spread in the upside is much greater for the fixed percentage approach (but this comes at the expense of a greater reduction in capital). In other words, it doesn't matter that much between using either natural yield or a fixed percentage of the portfolio when investing in the same things. However, one big difference is the initial withdrawal rate - clearly this is the same for all retirements when using the fixed percentage approach but depends on prevailing dividends and bond yields when using natural yield.

The argument between growth or dividends/value is a different one and not one I'm going to pursue.

Finally, the amount of income volatility that retirees can tolerate is a function of expenses and income (including guaranteed income) as well as personal preference. For example, a couple with full state pensions and a £100k initial portfolio, might expect their natural yield income from the above graph to vary between 21+2=23k and 21+6=27k, i.e. about 20% variation from peak to trough. For a couple with full state pension and a £1m portfolio, their income might vary from 21+20=41k to 21+60=81k, i.e. a 100% variation from peak to trough.

Your charts show an inital natural income of less than 4%. That strikes me as rather low. Though as you say you are assuming the same underlying investments for both cases. A key aspect of my case is that one would not do that. Using different types of equity in different ways adds to diversification.

On the variabililty question I would only advocate i ncome investing for covering part of ones day to day expenditure and would use liability planning for selling investments for one-offs.Under those circumstances significant variability of income could be an issue.

Another point is that only the worst case scenarios are of interest. Excess income is rather easier to manage than insufficient.

1 -

If dividends are less volatile than capital value, then having a bit more in equities and less in bonds makes sense. The era in which one is investing makes a huge difference - anyone constructing their retirement portfolio in the 1980s could have made use of 10%+ yields across a range of maturities of government bonds (fixing those rates for when inflation finally dropped would have been prescient!). One advantage of using dividends and coupons in those days was that it reduced stockbroker fees and ran itself (e.g., my father's portfolio from that period, which consisted on individual stocks and bonds, was set up to provide dividends/coupons at regular intervals throughout the year - after he died, money just turned up in my mum's account without her having to do anything).Linton said:

I dont think a 50/50 equity/bond ratio is necessarily a good idea for income investing. The problem is inflation - very broadly, all other things being equal, given sufficient time etc etc one would expect dividends to increase with inflation. On the other hand natural bond income is fixed from the time you buy the bond by definition. In any case until very recently natural bond income was derisory unless one used higher risk corporate bonds which could have been problematic. I am not yet sure about how best to use safe bonds now that interest rates are at sensible levels.

Your charts show an inital natural income of less than 4%. That strikes me as rather low. Though as you say you are assuming the same underlying investments for both cases. A key aspect of my case is that one would not do that. Using different types of equity in different ways adds to diversification.

On the variabililty question I would only advocate i ncome investing for covering part of ones day to day expenditure and would use liability planning for selling investments for one-offs.Under those circumstances significant variability of income could be an issue.

Another point is that only the worst case scenarios are of interest. Excess income is rather easier to manage than insufficient.

Dividend yields in the UK stock market have varied between 2% (1919) to nearly 12% (1974 - dividend amounts didn't drop too much even during that crash, hence the high yield) with them falling between 3% and 6% most of the time. Anyway, the 1919 case represents the low starting value.

Tolerance of income variability is probably one of those things that puts the personal into personal finance and is the sort of thing that makes this forum interesting reading - flooring with state pension, DB pensions, and (possibly) annuities all help reduce reliance on the risk portfolio regardless of what approach is adopted.1 -

As I see it, the benefit of dividend paying ITs, for essential income in particular, is that you have a very good idea of what income you can expect every quarter, no matter what happens in the market. You are correct in that you could sell capital to give yourself a 'dividend' every quarter as income, or sell whenever you need income. That's fine for those happy to do that for their essential income, but I suspect many retirees managing their own portfolios may be more reluctant to sell in a falling market. Therefore there could be more decision making needed and worry about whether to sell or wait for the market to recover.GazzaBloom said:

But if you look at capital + divs taken is that any different to selling off some capital from an index fund? The total value has to be the same if divs are just a distribution of a company's profits rather than them being retained. Divs are just forced on you and reduce the stocks capital value, selling an index is no different except you choose when to take the "dividend".Audaxer said:

That's true. I'm retired and have an income portfolio which includes some of the 'dividend hero' ITs. It isn't 100% equities as it also includes a couple of bond funds. I have been wondering recently if I really need the bond funds, and whether I should sell them and put the proceeds into the equity income ITs. I've not decided yet but think I'd be okay with the increased volatility.jimjames said:

Although if you have income producing funds in your portfolio especially those that have maintained their dividends over decades then I suspect it might be less of an issue if the market drops as your income is less linked to the current market price. I maybe should have added that the portfolio composition may well change at retirement even if it remains 100% equities.Linton said:

Yes, it all depends on your requirements. When you are looking purely at the long term and do not need your investments to maintain your current standard of living 100% equity could well be right for you. However as you approach and pass retirement age with limited guaranteed income long term returns are likely to decrease in importance as you focus more on how you manage your finances in the meantime.jimjames said:100% equity here and has been for the last 25+ years. I don't see that changing anytime soon.

Or am I mistaken?

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards