We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Buildings insurance, subsidence and a withdrawn mortgage offer

It is galling as they offered us the mortgage itself with full knowledge of this history and having sent out their surveyor to assess the subsidence in person.

Can anyone offer advice on insurers who might have a lower excess in this situation, or mortgage lenders who have different criteria?

For context, the cause of the cracking was clay-shrinkage-related subsidence as a result of vegetation. Trees were removed and a certificate of structural adequacy was issued. Before deciding to pursue the property we engaged a specialist historic surveyor and structural engineers among others (arborists, drains specialists, roofers, the list goes on...)

I appreciate many will still say cut your losses, but I'd like to feel I've tried every avenue before we do so.

Thanks for reading.

D.

Comments

-

Have you talked to an insurance broker and set out the terms £1000 excess and no more. Let them do the leg work for you.

You will likely have to pay a hefty yearly premium to bring the excess down but rarely do insurance companies not have a figure they will be happy to sell a product for.2 -

I have observed that after a building claim like subsidence or similar.

When the house gets a new owner the insurance sector can just wind up the prices and excess as they can.

A few years ago a new buyer was buying a house as per above and the new to be owners requested to use same insurance that had insured the house for 20 years.

Subsidence claim was 12 years before the sale above I mention.

The insurance company wanted 4K annual premium for new owner and old price was £700 PA.

The sale failed and due continuous issues with companies not wanting the risk it took 12 months to sell it and unfortunately 10% below the average price for that road area.

My view is I would always try staying clear of buildings insurance issues and claims unfortunately.

I'm also guessing with the poor building standards and inspections plus climate, subsidence and similar will become more of an issue fir more people.

1 -

There might be 2 options to investigate...

Option 1

The building was insured in 2021 when the claim was made. Presumably the sellers have stuck with that same insurer who paid that claim since then.

Normally, that same insurer would be prepared to continue insuring the property with you as the new policy holder. Have you tried that approach?

Maybe ask the sellers to contact their insurers and ask.

Option 2

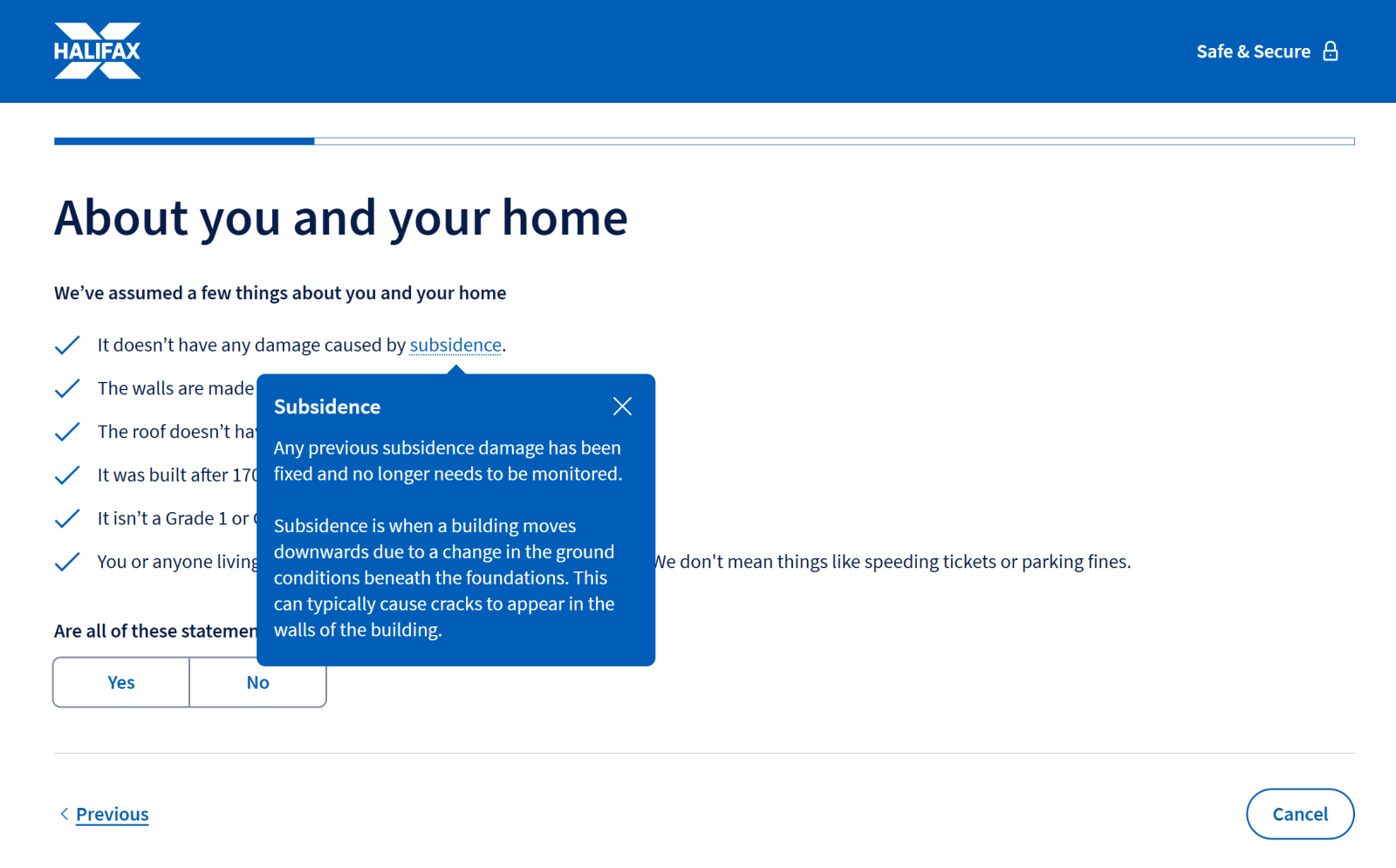

Try going direct to any company brand in the Lloyds bank group (Lloyds Bank, Bank of Scotland, Halifax). They say they'll insure on normal terms, as long as any subsidence damage has been repaired, and there's no further monitoring required. Maybe get a quote online, then phone them or webchat with them to make sure.

Lloyds Bank group is likely to be the cheapest option, as they would insure on normal terms (i.e. the same premium and same excesses as a house which hadn't had subsidence.)...

1 -

Thanks all for the replies.

The vendors' existing insurance is with Adrian Flux - they wouldn't transfer the policy and can only offer us a policy with £5,000 excess for subsidence.

Really appreciate the recommendation of Lloyds @eddddy - I tried them but their underwriter also came back with £2,500 which we are getting a lot.

Many insurance companies/brokers I'm speaking to comment that it's unusual for a lender to stipulate a figure for the subsidence excess, given that the liability is with the insurer. Impossible situation really.

0 -

I just wanted to thank you for this post as we are the seller side but otherwise in the same position. This advice worked for us and has saved our house sale!eddddy said:

There might be 2 options to investigate...

Option 1

The building was insured in 2021 when the claim was made. Presumably the sellers have stuck with that same insurer who paid that claim since then.

Normally, that same insurer would be prepared to continue insuring the property with you as the new policy holder. Have you tried that approach?

Maybe ask the sellers to contact their insurers and ask.

Option 2

Try going direct to any company brand in the Lloyds bank group (Lloyds Bank, Bank of Scotland, Halifax). They say they'll insure on normal terms, as long as any subsidence damage has been repaired, and there's no further monitoring required. Maybe get a quote online, then phone them or webchat with them to make sure.

Lloyds Bank group is likely to be the cheapest option, as they would insure on normal terms (i.e. the same premium and same excesses as a house which hadn't had subsidence.)...Lloyds bank confirmed they do not discriminate against past history of subsidence, as long as any damage is repaired and no monitoring is happening. Same for Halifax etc.0 -

I have understood for years - whether correctly or not - that mortgage lenders need the subsidence excess to be £1K.Danby4244 said:Thanks all for the replies.

The vendors' existing insurance is with Adrian Flux - they wouldn't transfer the policy and can only offer us a policy with £5,000 excess for subsidence.

Really appreciate the recommendation of Lloyds @eddddy - I tried them but their underwriter also came back with £2,500 which we are getting a lot.

Many insurance companies/brokers I'm speaking to comment that it's unusual for a lender to stipulate a figure for the subsidence excess, given that the liability is with the insurer. Impossible situation really.

Just wondering whether @Annemos has any comments about the subsidence and insurance policy side of things, as I know s/he has commented elsewhere on the forum about such things.

0 -

I am so sorry for the late reply. I had not logged in for a spell.Yorkie1 said:

I have understood for years - whether correctly or not - that mortgage lenders need the subsidence excess to be £1K.

Just wondering whether @Annemos has any comments about the subsidence and insurance policy side of things, as I know s/he has commented elsewhere on the forum about such things.

I don't have anything to add, as my knowledge of mortgages is non-existent. But the Lloyds comments above are very interesting. It worked for one but not the other.

I am resigned to staying in my Bungalow now, as I am getting older. So, I fear the Sale-problem will pass to my Neice and Nephew when they inherit the Place. (And potentially if it had to be sold for Care Costs)Heygepetto said:

I just wanted to thank you for this post as we are the seller side but otherwise in the same position. This advice worked for us and has saved our house sale!Lloyds bank confirmed they do not discriminate against past history of subsidence, as long as any damage is repaired and no monitoring is happening. Same for Halifax etc.

Heygepetto, may I ask you, how long ago was your Subsidence Claim opened and how long ago was it closed? I can only imagine the utter relief you felt when you had that fantastic news.

1 -

my claim started in April 2021 and was settled in Jan 2025. No underpinning required, but we fixed the cosmetic damage. All Halifax, Lloyds or Bank of Scotland asked for was this:

No certificate of structural adequacy, or any other details needed. Very easy process with normal level of premium and £1000 subsidence excess for bronze level. If I went up to Silver or Gold cover, I could reduce the subsidence excess even more. I couldn’t quite believe it was so easy so rang them to check snd they verified it was all good.

1 -

Thank you very much for the information.

That is really encouraging news.

I may be looking for insurance myself, soon, unfortunately.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards