We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

If I don't buy annuity, give me the name of 3 funds to do the same in a SIPP drawdown scenario

AustinZ

Posts: 32 Forumite

Annuities are attractive now, because of interest rates going up, but some people totally dismiss them as wasting your pension and giving it all in admin fees to providers and no control over them.

So give me 3 funds that can buy in my SIPP to do the same job for then next 10 or 20 years, and I could just do drawdown and avoid buying annuity...

(No replies with 60% stock, 30% bond, 10 gilts and cash etc. etc. - just 3 exact fund names sold in UK, let's see if we can do it... !)

So give me 3 funds that can buy in my SIPP to do the same job for then next 10 or 20 years, and I could just do drawdown and avoid buying annuity...

(No replies with 60% stock, 30% bond, 10 gilts and cash etc. etc. - just 3 exact fund names sold in UK, let's see if we can do it... !)

1

Comments

-

Well if you want to replicate an annuity, it is basically gilt funds all the way, because that is what annuities are based on. Lower risk (because it's the annuity provider that takes the risk on your behalf and they're not stupid), but obviously lower returns along the way for you.And over 20 years, there aren't many people on here that would look at this as a sensible strategy. But it's your call, if that is your objective and your specific risk appetite.0

-

Nice challenge, but there are annuities that go until death, or have spouse residual payments, or are inflation linked. Don't make it any harder than it already is.

1 -

Vangaurd LifeStrategy 60 or 40 (depending on how volatile you want the fund to be)

HSBC Global Strategy Balanced or Cautious

Fidelity Multi Asset Allocator Growth or Strategic

You don't even need to invest in all 3 of the above funds, 1 will do.

If you are planning to draw down rather than buy an annuity it's a good idea to hold enough cash to last you for at least 3 years. This way you can top up your cash reserves when markets are high and eat into your cash when markets are low.

3 -

Here's a basic list of annuities although an IFA could probably get a bit more ? The level annuity is over 6% . RPI and escalating annuities are around the 4% mark at 60 yo.

Annuity Rates: View Best Annuity Rates from the UK Market (hl.co.uk)

Well you've ask for a fund and it ain't going to go down well on here but I'd rather buy a FTSE tracker than an annuity with a 10- 20 year window.

Current yield is 3.88% so within the escalating range of the annuity.

Dividend Yields - FTSE 100 (dividenddata.co.uk)

In comparison to other countries the FTSE is cheaper regarding valuation but that doesn't mean it will catch up. It's something in its favour.

Six charts that show how cheap UK equities are (schroders.com)

The dividends are forecast higher 2023-24. You will get blips along the way eg GFC 2008 and 2020 pandemic but the general trend is up.

FTSE 100 dividend forecasts slide amid uncertain climate | AJ Bell

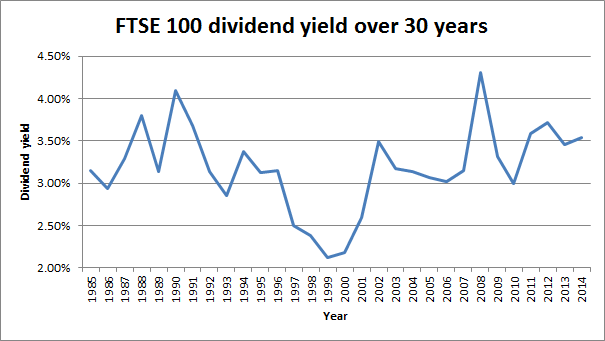

In 1985 the FTSE yield was 3.2% on an index reading of 1000. So £32 pay out a year. Today we have 3.88% on an index of 7250 or £281 pay out.

saupload_FTSE-100-Dividend-yield-over-30-years-2015-05.png (605×341) (seekingalpha.com)

From the inflation calculator £32 in 1985 is £94 today and todays pay out is £281.

Inflation calculator | Bank of England

Given the FTSE is 10% off its all time high and throw in another 10% uplift we're no asking for much even in 10 years. 20% capital gain and a rising dividend set against an annuity of your choice. So there's on simple selection.

FTSE 100 Index, UK:UKX Advanced Chart - (FTSE UK) UK:UKX, FTSE 100 Index Stock Price - BigCharts.com (marketwatch.com)

3 -

AFAIK, there are no mainstream funds which will do the same as an annuity........no matter which way you look at it, no mainstream fund I know of has an income guarantee like an annuity has.

That said, there are plenty of funds, which, given "average" returns over the next 20-30 years, will at least equal and may well outperform an annuity....but there is a risk they won't. Each individual has to evaluate that risk and decide for themselves.

If there were funds available for drawdown that did the same as an annuity, then annuities simply wouldn't exist.......

As for the name of a specific fund which fits the above criteria (ie likely to equal/outperform an annuity given "average" returns), there are plenty tbh... atm, for me, it'd probably be something like HSBC Global Strategy Balanced, but you'll likely get many others opinions too on a likely candidate fund, though none can be relied on without the benefit of hindsight in 20-30 years.

0 -

There is nothing that will safely do the full job of annuities with the same or higher income especially if you want that income to be index linked. What aspect of annuities do you want to sacrifice? Security of income, quantity of income, index linking?1

-

This was my thinking......if you want something that 'replicates an annuity' then why not just buy an annuity? Anything else will have certain associated risks.Linton said:There is nothing that will safely do the full job of annuities with the same or higher income especially if you want that income to be index linked. What aspect of annuities do you want to sacrifice? Security of income, quantity of income, index linking?'Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it' - Albert Einstein.0 -

There's no fund alternative, because the annuity pools longevity risk. Other than perhaps a well defined drawdown plan and a one way ticket to a Swiss clinic."Real knowledge is to know the extent of one's ignorance" - Confucius0

-

I'd agree with some of what you have said here (although the database at macrohistory.net has a yield of 4.3% in 1985 - but that doesn't change the narrative). However, the performance of the FTSE100 has been rather good since 1985 (e.g., a retirement starting in 1985 with 100% allocation to stocks would have had a 30 year SWR of about 9%), so that period may not be a good indicator of future performance (although, of course, it may)...coastline said:Here's a basic list of annuities although an IFA could probably get a bit more ? The level annuity is over 6% . RPI and escalating annuities are around the 4% mark at 60 yo.

Annuity Rates: View Best Annuity Rates from the UK Market (hl.co.uk)

Well you've ask for a fund and it ain't going to go down well on here but I'd rather buy a FTSE tracker than an annuity with a 10- 20 year window.

Current yield is 3.88% so within the escalating range of the annuity.

Dividend Yields - FTSE 100 (dividenddata.co.uk)

In comparison to other countries the FTSE is cheaper regarding valuation but that doesn't mean it will catch up. It's something in its favour.

Six charts that show how cheap UK equities are (schroders.com)

The dividends are forecast higher 2023-24. You will get blips along the way eg GFC 2008 and 2020 pandemic but the general trend is up.

FTSE 100 dividend forecasts slide amid uncertain climate | AJ Bell

In 1985 the FTSE yield was 3.2% on an index reading of 1000. So £32 pay out a year. Today we have 3.88% on an index of 7250 or £281 pay out.

saupload_FTSE-100-Dividend-yield-over-30-years-2015-05.png (605×341) (seekingalpha.com)

From the inflation calculator £32 in 1985 is £94 today and todays pay out is £281.

Inflation calculator | Bank of England

Given the FTSE is 10% off its all time high and throw in another 10% uplift we're no asking for much even in 10 years. 20% capital gain and a rising dividend set against an annuity of your choice. So there's on simple selection.

FTSE 100 Index, UK:UKX Advanced Chart - (FTSE UK) UK:UKX, FTSE 100 Index Stock Price - BigCharts.com (marketwatch.com)

2 -

For a lifetime annuity, there are almost no funds that can guarantee the equivalent income over the next 30 or more years*. However, there is one way which would be to use two bond funds of different durations (e.g., iShares UK Gilts 0-5yr UCITS ETF and either iShares Core UK Gilts UCITS ETF or iShares Over 15 Years Gilts Index Fund) which could be used to approximate a nominal bond ladder and, hence, a level annuity (but without the mortality credits) - the payout for a 40 year ladder with current yields to maturity of about 4.5% would be about 5.2% (compared to the 6.5% payout for a level annuity at 60).

* To be fair, the annuity carries some risks - credit risk (i.e., the insurance company goes out of business), but is currently covered by the FSCS in this event, so the guarantee is pretty strong.

2

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards