We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

C’mon, fess up.

Comments

-

Not necessarily 'savings' but to at the start of 2022, as we had built up unreasonably large amount of 'cash/emergency' savings, we decided to invest a relatively significant sum into an index fund.

We don't need the money and plan to have it invested for many years so the drop isn't terribly important... but with the benefit of hindsight, we pretty much couldn't have timed the peak of the market any better....

But I understand we're all in the same boat! Investing in 2022 was certainly an adventure...

Know what you don't1 -

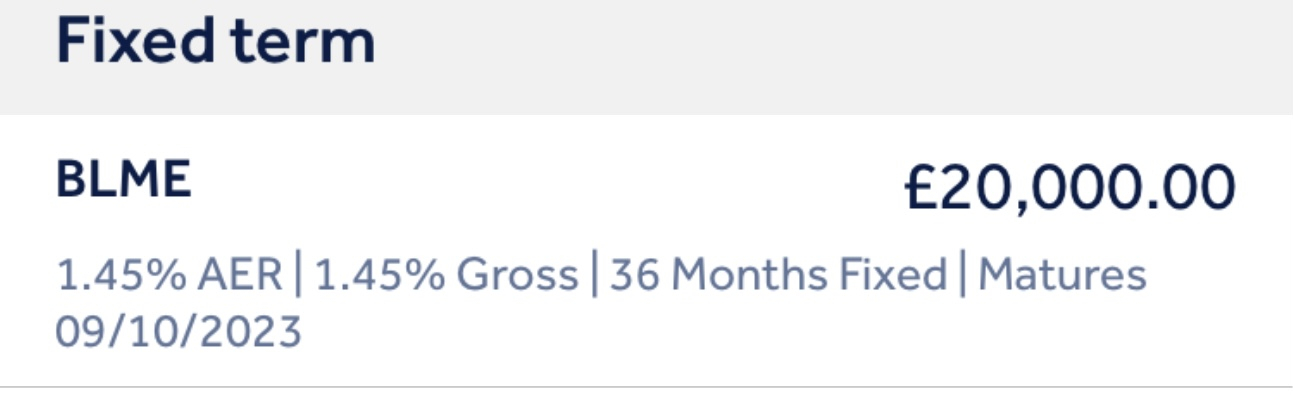

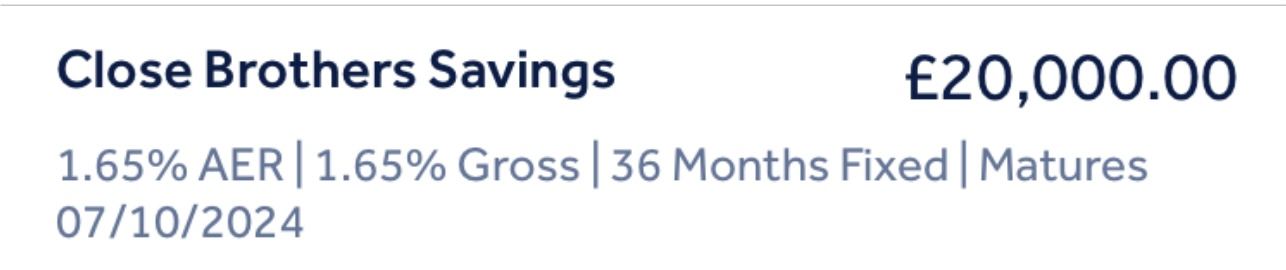

A 2.6% and a 2.72% 1 year bonds maturing in the next fortnight. Don't regret them as such, at the time they were great, that's why I did two in a short space of time.0

-

4.5% fixed for 1 year beginning of April. Then the stubborn inflation figures were released and rates have been going up ever since. I timed it to perfection, but not in a good way. Ah well...

My worse mistake was not to fix my mortgage in 2021 for about 1.25%. I was currently paying less on a tracker and couldn't be bothered, thinking rates might go up "a bit." How wrong I was! I was not tied in, I could have done the switch with the same lender in 10 minutes, but didn't think it was worth it.0 -

As someone once said, there's a reason why you've got a huge great windscreen and a tiny rear view mirror.5

-

I did the same but luckily I held half back and then invested that at the lows of June and October so managed to average out my unrealised losses.Exodi said:Not necessarily 'savings' but to at the start of 2022, as we had built up unreasonably large amount of 'cash/emergency' savings, we decided to invest a relatively significant sum into an index fund.

We don't need the money and plan to have it invested for many years so the drop isn't terribly important... but with the benefit of hindsight, we pretty much couldn't have timed the peak of the market any better....

But I understand we're all in the same boat! Investing in 2022 was certainly an adventure...1 -

I have a couple of QIB 2 year fixes with Raisin @.......now don't laugh, 1.7%! Luckily they are both coming to an end soon. At the time they would have been near the top of the table, just shows how times change. Since I have a fixed interest ladder these two fixes only account for ~10% of my total fixes, so shows the benefit of having a ladder!'Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it' - Albert Einstein.0

-

Two bad mess ups that seemed a good idea in 2020 and 2021 sadly with no early maturity option …

2 -

It did look like 5 year fixes had peaked at the end of last year (at around 5%) and were dropping to mid 4-5% March/April and low 4% for ISA - so although theyve gone up a lot since then they still give a good income - especially compared with rates a year ago.

Any fixes maturing now can get a much better rate - but fixes are still rising so now may not be a great time to re-invest.

Even for fixes maturing next year the rates on offer may still be good the way things are going.

1 -

But its equivalent to 5% ish in taxable it's not the end of the worldMiddle_of_the_Road said:

As did I. Very bad timing.Catplan said:Funded a 4.2 fixed Isa in April.1 -

A 3 year fixed rate of a stratospheric 0.96%, starting in April 2021. Yes, no-one reasonably foresaw Russian invading Ukraine, but a reasonable thought would have been "the downside of just using an instant access, notice or short-term account instead would just be 0.3% pa, perhaps, and the possibility of interest rates going up in those 3 years, by more than that, for whatever reason, must be significant" - and it turned out to be "by way more than that".1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards