We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

New to ISA's - how many can I open?

Comments

-

Look good to me! I use Chip for instant access, as it really is instant, but there are plenty of other providers on the links above.Gareth77 said:So I am saving to then over pay the mortgage in 3 years time. From the above it feels like I should

1) put 20K in a fixed term ISA (to avoid tax and this is the max I can put in a ISA) for 2 years

2) put 20K in a fixed term savings (say Natwest 5%) for 2 years

3) put the rest in an easy access account (incase something happens and I need it) - and keep saving to that each month1 -

One suggested amendment would be on bullet 2), maybe look at a 1-year fixed term savings as next tax year your ISA allowance will reset and you will be able to then put that into another 1-year ISABeddie said:

Look good to me! I use Chip for instant access, as it really is instant, but there are plenty of other providers on the links above.Gareth77 said:So I am saving to then over pay the mortgage in 3 years time. From the above it feels like I should

1) put 20K in a fixed term ISA (to avoid tax and this is the max I can put in a ISA) for 2 years

2) put 20K in a fixed term savings (say Natwest 5%) for 2 years

3) put the rest in an easy access account (incase something happens and I need it) - and keep saving to that each month1 -

For and ISA Virgin have upped their rates today 1y 5.05% 2y 5.155 and 3y 5.20% early access charges are No to bad either.Gareth77 said:So I am saving to then over pay the mortgage in 3 years time. From the above it feels like I should

1) put 20K in a fixed term ISA (to avoid tax and this is the max I can put in a ISA) for 2 years

2) put 20K in a fixed term savings (say Natwest 5%) for 2 years

3) put the rest in an easy access account (incase something happens and I need it) - and keep saving to that each month

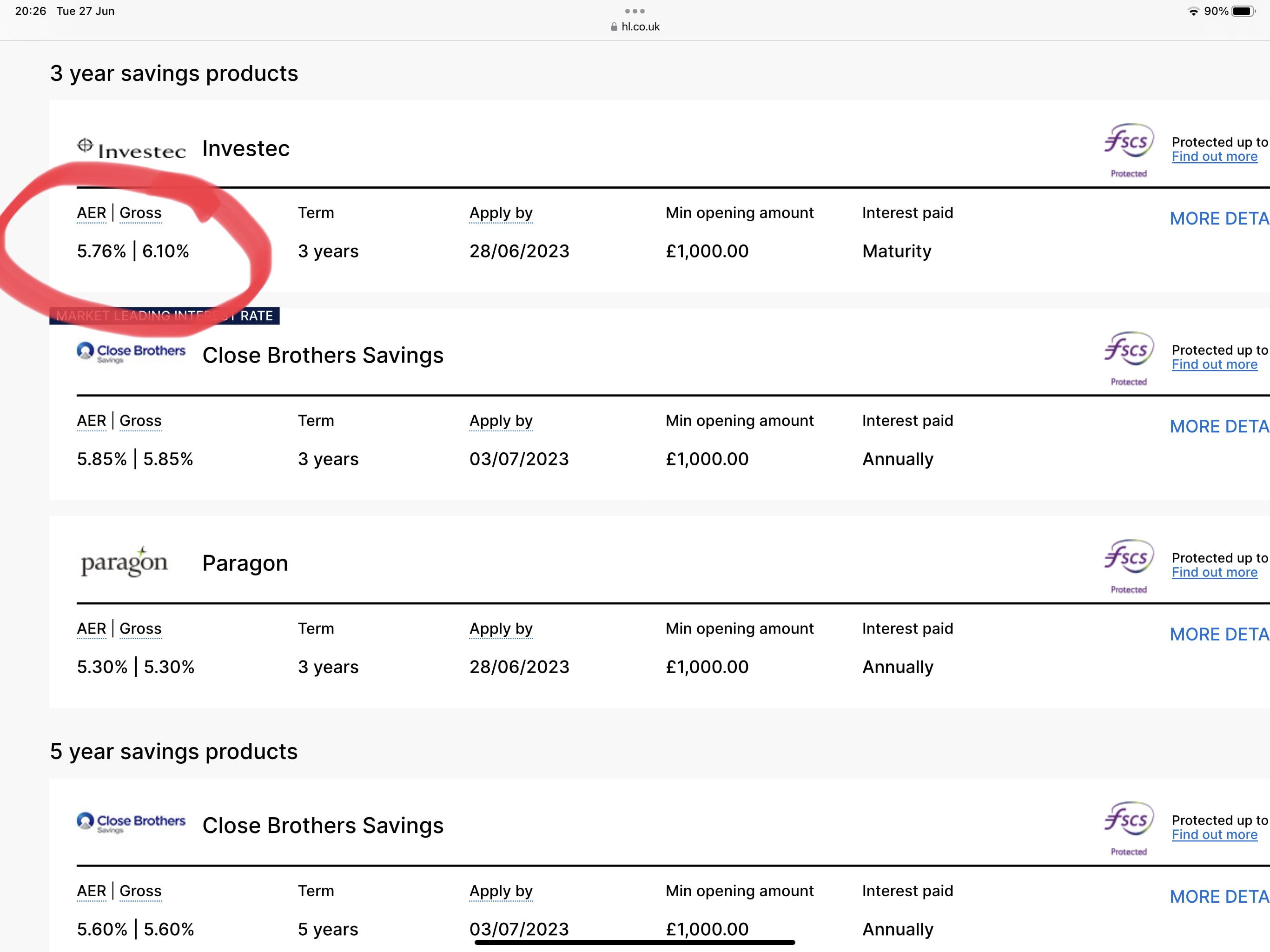

If you fixed for 3 year and compounded the interest there is an account paying 6.1%.

https://www.hl.co.uk/investment-services/active-savings/fixed

1 -

The interest in that one is only payable in maturity though so you wouldn’t be able to compound the interest until after 3 years, hence the lower AER than the other bonds in that list? Also, I think the interest will all get taxed in year 3 which might be worse for some people.Bigwheels1111 said:

For and ISA Virgin have upped their rates today 1y 5.05% 2y 5.155 and 3y 5.20% early access charges are No to bad either.Gareth77 said:So I am saving to then over pay the mortgage in 3 years time. From the above it feels like I should

1) put 20K in a fixed term ISA (to avoid tax and this is the max I can put in a ISA) for 2 years

2) put 20K in a fixed term savings (say Natwest 5%) for 2 years

3) put the rest in an easy access account (incase something happens and I need it) - and keep saving to that each month

If you fixed for 3 year and compounded the interest there is an account paying 6.1%.

https://www.hl.co.uk/investment-services/active-savings/fixedNorthern Ireland club member No 382 :j0 -

Some cash ISA providers will allow you to invest money into separate ISA accounts which are lumped together in a single ISA wrapper. This would allow you to (say) invest £10k in a 1yr fix and £10k in a 2yr fix, or (say) split £5k instant access, £15k 1yr fix.

This may be important when you first start switching from "everything's in instant access accounts", as you really don't want to lock up all your savings for an extended period. You really want to have a situation where you have one or more fixed term account maturing each year, so that you know that the money is then instantly accessible either to be left instant access or rolled over into another fixed term account.

Once you have built up a decent sized pot of Cash ISA money, then you have a lot more flexibility as you can divide "old"/previous years money between as many ISAs and providers as you like.

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards