We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Nationwide's 'Fairer Share' £100 payment for eligible members

Comments

-

As you would expect, because Natwest is making a profit for the shareholders (and there will be other structural differences too like the size of the branch network etc).onlyconnect said:

Nationwide does have better savings rates than most high street banks. NatWest for example has much lower savings rates.TheBanker said:Or, perhaps more fundamentally, we could ask why Nationwide has made an excess profit of £340m in the first place. They need to make sufficient profit to invest in the future of the society, but as they have no shareholders they should not be generating surplus profit for distribution. So we're back to the point about why they're not increasing savings rates and/or reducing mortgage rates.

Tim

The question is why Nationwide's savings and mortgage rates have been set in such a way that results in a £300m+ profit, when there are no shareholder dividends to be paid.

(Note - I do recognise that some of Nationwide's profit will have come from non-core products such as credit cards and insurance, and from their subsidiary BTL mortgage business)2 -

It has to be run as a profit seeking business as, given it cannot raise capital from its 'owners', it's about the only way it can generate loss-absorbing capital. Post the Co-op Bank failure it worked extremely hard to build its CET1 capital levels from modest to eye-popping levels - currently 26.5%(!).TheBanker said:

As you would expect, because Natwest is making a profit for the shareholders (and there will be other structural differences too like the size of the branch network etc).onlyconnect said:

Nationwide does have better savings rates than most high street banks. NatWest for example has much lower savings rates.TheBanker said:Or, perhaps more fundamentally, we could ask why Nationwide has made an excess profit of £340m in the first place. They need to make sufficient profit to invest in the future of the society, but as they have no shareholders they should not be generating surplus profit for distribution. So we're back to the point about why they're not increasing savings rates and/or reducing mortgage rates.

Tim

The question is why Nationwide's savings and mortgage rates have been set in such a way that results in a £300m+ profit, when there are no shareholder dividends to be paid.

(Note - I do recognise that some of Nationwide's profit will have come from non-core products such as credit cards and insurance, and from their subsidiary BTL mortgage business)I guess it's decided that it doesn't need to build its capital any further plus recently most banks and BS' have seen a boost in their profits since rates began to rise. IIRC Coventry BS recently announced very good results as well.

https://www.nationwide.co.uk/about-us/governance-reports-and-results/results-and-accounts/ 4

4 -

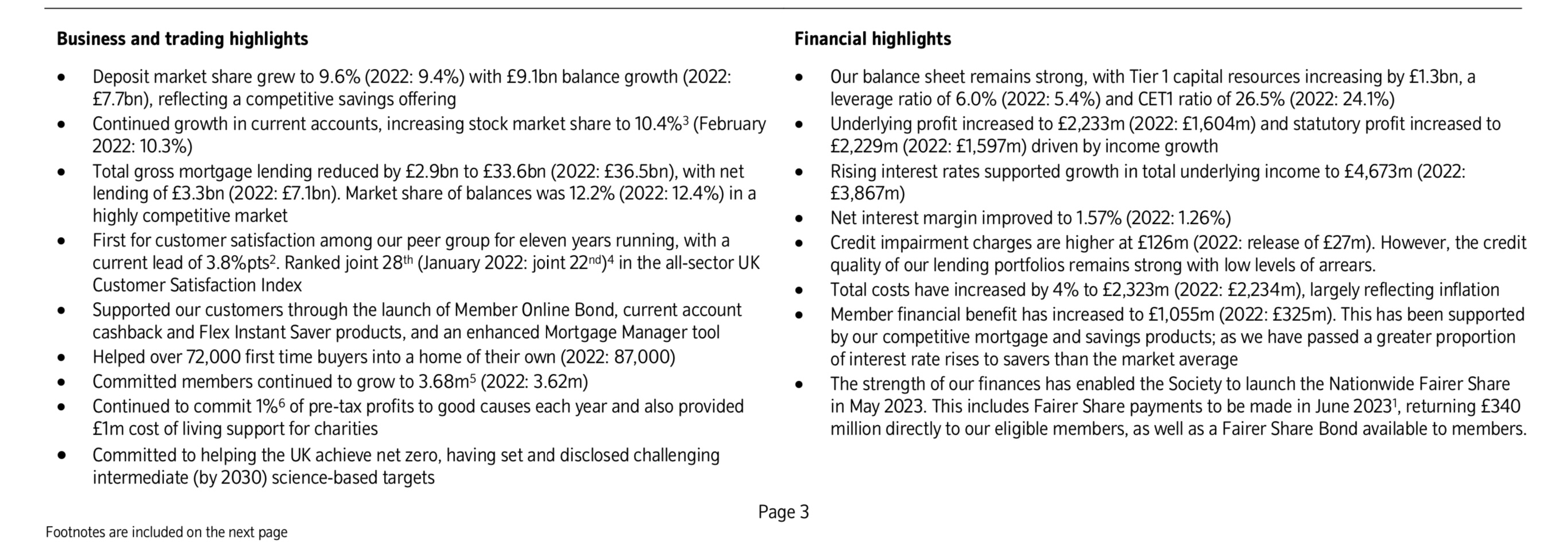

As others have said, the simple way Nationwide could distribute their surplus profits would have been to offer better interest rates so that there weren't any surplus profits in the first place! In their financial year to 4 April 2023, Nationwide's net interest margin increased to 1.57%. It was 1.26% in the previous year. I highly doubt that increase happened by accident, and will have been mainly as a result of deliberate management decisions when setting interest rates. Time after time, as base rates increased, Nationwide passed on less than the full increase, and increases have also been passed on more slowly than most other building societies. Yorkshire Building Society had a net interest margin of 1.30%, and Coventry's was 1.16% by way of comparison.

Nationwide's savings rates are generally awful. Their top savings rate is their regular savings account, Smart to Save, currently paying 5.25%. However, this only allows £50 to be paid in per month. Even most of the big banks offer both higher rates, and higher deposit limits on their regular savers (e.g. First Direct, HSBC subsidiary 7% with £300pm limit, Lloyds 6.25% with £250pm limit, NatWest and Royal Bank of Scotland with 6.17% with £100pm limit, Halifax and Bank of Scotland with 5.5% with a £250pm limit).

Nationwide's highest currently available instant access rate is the Flex Instant Saver, which pays 2.5% and is exclusively available to their current account holders (lucky them!). Now let's look at Yorkshire Building Society. The LOWEST rate they offer on ANY of their savings accounts is 3.05%, with no requirement to hold other products in order to get that rate. Nationwide's lowest rate on legacy accounts (and also the rate on the only instant access account available to non current account holders) is only 1.25%. Yorkshire's lowest rate on any of their legacy accounts is 3.05%.

So Nationwide's highest instant access account (a current account loyalty product) pays 0.55% less than Yorkshire's lowest instant access account (even including all of their legacy accounts) - let that sink in for a minute!

Nationwide don't even bother to offer an instant access ISA. They have a limited access ISA, which pays 3.2% and allows 3 withdrawals a year. Yorkshire's instant access ISA pays 3.25%, with unlimited withdrawals. Yorkshire also offer a stunning loyalty ISA for those who have been a member for at least 12 months, paying 4.5% on the first £20,000 (with 4% on the excess over £20,000).

So the solution to this problem is simple - just pay better interest rates.

7 -

Band7 said:

I am not really expecting answers. I just wanted to demonstrate that, IMO, it's nigh on impossible to come up with an affordable solution that would satisfy everyone.I don't think anyone is suggesting there would be a scheme which would satisfy everyone.The argument being put forward is that the solution should satisfy the majority of members, and with only ~20% of the membership getting £100 it is difficult to see that solution satisfying 50%.If Nationwide couldn't think of a more equitable solution then at the very least the scheme should have been put to members at the AGM. IMV this is roughly the mutual equivalent of a special dividend - i.e. outside the normal day-to-day business of the building society - and therefore members should have had more say in how the money is distributed (or kept and distributed at a later date).The arguments this money needs to be distributed quickly are largely bogus. The linkage made to the 'cost of living crisis' is laughable.Nationwide already has a structure in place to allow members to vote - the AGM - so all they had to do was either to seek approval for this scheme, or else offer members a choice of solutions and go with the one which obtained the most AGM votes.In the past Nationwide has had to donate money to charity for each AGM vote cast to incentivise people to vote (in an otherwise pointless exercise). Having a vote on how the profits are distributed would be a much better incentive for individuals to vote for the option that suits them best. It would be a more effective way of getting members involved in its democratic process.3 -

Of course Nationwide makes profits from credit card and loan customers, even if those are not considered members if they don‘t also hold another account with Nationwide.TheBanker said:Credit card and loan customers are not members (unless they qualify as a member by holding a current account, savings account or mortgage as well). So they do not need to be included in a distribution of the society's profits.

As the profits have been generated by savers and mortgage holders

Your argument falls seriously down when demanding share payments based on contribution to profits, and at the same time excluding people who have contributed to profits.0 -

onlyconnect said:

Nationwide does have better savings rates than most high street banks. NatWest for example has much lower savings rates.TheBanker said:Or, perhaps more fundamentally, we could ask why Nationwide has made an excess profit of £340m in the first place. They need to make sufficient profit to invest in the future of the society, but as they have no shareholders they should not be generating surplus profit for distribution. So we're back to the point about why they're not increasing savings rates and/or reducing mortgage rates.

Tim???Natwest's Digital Regular Saver pays 6.17% AER (up to £150/month, max balance £5000)How is that 'much lower' than Nationwide's offer?Moreover, comparing Nationwide's rates with 'high street banks' isn't a fair comparison. Nationwide is a mutual and we are supposed to get better rates. A fairer comparison would be with other building societies. Also, people don't normally go to high street banks to get the best rates on their savings. Traditionally you went to a building society for that, now you follow sites like MSE to find the best place on any given day. Nationwide is seriously lacking in that regard.3 -

Are you sure? I'm not convinced that NatWest actually currently does have lower interest rates than Nationwide, never mind "much lower" rates. NatWest don't have a huge range of savings accounts, but I've gone through every savings account they currently offer:onlyconnect said:

Nationwide does have better savings rates than most high street banks. NatWest for example has much lower savings rates.TheBanker said:Or, perhaps more fundamentally, we could ask why Nationwide has made an excess profit of £340m in the first place. They need to make sufficient profit to invest in the future of the society, but as they have no shareholders they should not be generating surplus profit for distribution. So we're back to the point about why they're not increasing savings rates and/or reducing mortgage rates.

Tim- Regular savings - NatWest pays 6.17%, Nationwide pays 5.25%

- Instant access - NatWest pays variable rates depending on the balance. They pay 1% up to £24,999, which increases to 1.66%, 2.17% and 2.57% as the balance increases. Nationwide pay a flat 1.25% on all balances, so if the balance is under £25,000 than Nationwide are better, and if the balance is higher then they are worse.

- 1 year fixed rate - NatWest pay either 4.28% (up to £99,999) or 4.39% above that. Nationwide pay 4.1%.

- 2 year fixed rate - NatWest pay either 4.39% (up to £99,999) or 4.49% above that. Nationwide now pay 4.75% under their new "Fairer Share" account, launched as part of the same initiative as the £100 giveaway.

- Children's account - NatWest pay 2.27%. Nationwide don't currently offer one.

- 1 year Fixed rate ISA - NatWest pay 4.2%. Nationwide pay 4.1%.

- 2 year fixed rate ISA - NatWest pay 4.3%. Nationwide don't offer one.

- Instant access Cash ISA - NatWest pay 1.26% up to £25,000 and 2.53% above that. Nationwide don't offer an instant access ISA currently, but their previous Instant Access ISA (which is no longer available) pays 1.25% up to £9,999, 1.35% between £10,000 and £49,999 and 1.5% over £50,000.

On all of the other accounts, NatWest actually pays more interest than Nationwide.5 -

masonic said:Given turnout is usually so low, perhaps offer everyone voting a fiver and let Martin Lewis and others help promote it.Only if they get rid of the 'quick vote' option - otherwise they risk getting results which Kim Jong Un would find embarrassing.Personally I don't think there should be any financial incentive to vote, not even the charity donation. If the board and senior management aren't doing enough that members want to get involved in the democratic process they should be taking a long hard look at what they are doing and why members feel so detached.The charity incentive and quick vote tends to mask the true level of apathy.

2 -

I'm not demanding anything.Band7 said:

Of course Nationwide makes profits from credit card and loan customers, even if those are not considered members if they don‘t also hold another account with Nationwide.TheBanker said:Credit card and loan customers are not members (unless they qualify as a member by holding a current account, savings account or mortgage as well). So they do not need to be included in a distribution of the society's profits.

As the profits have been generated by savers and mortgage holders

Your argument falls seriously down when demanding share payments based on contribution to profits, and at the same time excluding people who have contributed to profits.

The members are the owners, the non-members do not own part of the society.

Normally profit would be distributed to owners based on how many shares they own. Clearly this wouldn't work for a mutual. Hence my suggestion that the profit should be distributed in a way that favours those members who generated it.4 -

spider42 said:

....onlyconnect said:

Nationwide does have better savings rates than most high street banks. NatWest for example has much lower savings rates.TheBanker said:Or, perhaps more fundamentally, we could ask why Nationwide has made an excess profit of £340m in the first place. They need to make sufficient profit to invest in the future of the society, but as they have no shareholders they should not be generating surplus profit for distribution. So we're back to the point about why they're not increasing savings rates and/or reducing mortgage rates.

Tim

On all of the other accounts, NatWest actually pays more interest than Nationwide.

TL;DR - Nationwide's marketing department do a fantastic job at convincing people they are better off with their savings at a mutual rather than a high street bank.

2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.3K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards