We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Vangaurd life strategy 40

Comments

-

InvesterJones said:By showing graphs from 1870 and 1900, are you saying that equities are best invested in for periods of 150+ years? I can't wait that long!Is it the way you interpret those statistical chart, taking conclusion ???Say the chart is extended to another 100 years in the future, to see the result are you saying you will not be waiting until 250 years ?? Certainly 100 years from now is not our era.

0 -

Did I say otherwise ? "History does not repeat but often rhythm". Noone could predict the future with 100% certainty. But talking about probability a certain event will happen in the future is a different thing. If you know that in the past when you toast an unfair coin the head turn up most of time and you need to choose, what one will you choose head or tail ?GeoffTF said:Past performance in markets in which equities did exceptionally well tells us little about the future. There is no guarantee that equities will outperform bonds over the next 100 years, and most of us cannot wait that long anyway.GeoffTF said:he purpose of saving for most of us is to meet our future financial liabilities. It is essential that we do not fail at that, and it does not matter much whether or not we do any better. Globally, the average portfolio is about 40% equities and 60% bonds. Clearly, most of the money believes that your chosen pundits are either wrong or trying to answer the wrong question.Again did I ever say otherwise ? If your goal is to manage your money for a short term then you are not investing, is it ?? If you put your money into a short term duration bond/gilts up to 3 years to be held until maturity then you are not investing.What you are doing is finding a way of avoiding tax, managing cash flow. It makes sense if you have exhausted all of the risk free alternative and to avoid into paying tax while managing your cash flow.There is also what is so called cash alike instrument buying/selling/repurchase an asset or individual stock that could easily be sold and repurchase again, but for this need a particular skill.Certainly It is not suggestible for people who do not want to take risk and to learn a new thing.0 -

I opened a Vanguard LS 60%-40% in 2021, initial deposit of £500 and a regular monthly payment of £10.

Whenever I logged in to my account all I would focus on is the loss amount, so I've stopped checking now.

I was 47 when the account was opened and fingers crossed I'm not planning on touching the money until I'm at least 55. I'm in it for the long haul.SPC 0371 -

We know that the probabilities will be different. The rise of the US over the past 150 years will not continue. The UK has already declined in power and is on a downward path. Our island status will not protect us in the next world war. The growth in prosperity will be brought to an end by over-consumption, notably by climate change. We know all of this, but we do not know when it will happen. Will the global capitalism that used to be promoted by the US survive? Probably not. The future is unknown. Future probabilities will be different from past probabilities.adindas said:

Did I say otherwise ? "History does not repeat but often rhythm". Noone could predict the future with 100% certainty. But talking about probability a certain event will happen in the future is a different thing. If you know that in the past when you toast an unfair coin the head turn up most of time and you need to choose, what one will you choose head or tail ?GeoffTF said:Past performance in markets in which equities did exceptionally well tells us little about the future. There is no guarantee that equities will outperform bonds over the next 100 years, and most of us cannot wait that long anyway.1 -

GeoffTF said:We know that the probabilities will be different. The rise of the US over the past 150 years will not continue. The UK has already declined in power and is on a downward path. Our island status will not protect us in the next world war. The growth in prosperity will be brought to an end by over-consumption, notably by climate change. We know all of this, but we do not know when it will happen. Will the global capitalism that used to be promoted by the US survive? Probably not. The future is unknown. Future probabilities will be different from past probabilities.

Well, you are a bundle of joy and optimism this morning! 0

0 -

The truth is rarely precisely what you want to hear.Adyinvestment said:GeoffTF said:We know that the probabilities will be different. The rise of the US over the past 150 years will not continue. The UK has already declined in power and is on a downward path. Our island status will not protect us in the next world war. The growth in prosperity will be brought to an end by over-consumption, notably by climate change. We know all of this, but we do not know when it will happen. Will the global capitalism that used to be promoted by the US survive? Probably not. The future is unknown. Future probabilities will be different from past probabilities.

Well, you are a bundle of joy and optimism this morning!

0 -

He missed out AI taking over the world and making most humans redundant, leading to end of civilisation etcAdyinvestment said:GeoffTF said:We know that the probabilities will be different. The rise of the US over the past 150 years will not continue. The UK has already declined in power and is on a downward path. Our island status will not protect us in the next world war. The growth in prosperity will be brought to an end by over-consumption, notably by climate change. We know all of this, but we do not know when it will happen. Will the global capitalism that used to be promoted by the US survive? Probably not. The future is unknown. Future probabilities will be different from past probabilities.

Well, you are a bundle of joy and optimism this morning!2 -

adindas said:InvesterJones said:By showing graphs from 1870 and 1900, are you saying that equities are best invested in for periods of 150+ years? I can't wait that long!Is it the way you interpret those statistical chart, taking conclusion ???Say the chart is extended to another 100 years in the future, to see the result are you saying you will not be waiting until 250 years ?? Certainly 100 years from now is not our era.Only if someone was using the end result of 150 years to make a point - which is inevitable if you're showing lines diverging over that period.A better statistic is looking at what the probabilities are of making a return, and what range of return, for a given time frame and different investments. That way you can see that equities have a greater potential return, but also a greater odds of a loss in shorter (<10 years) time frames. As you up the bond proportion it's these odds that get better - ie you are more likely to generate a positive return in the shorter time frame, or put another way, you don't have to wait as long to be more likely to generate a return.

0 -

Not sure if the Pensioncraft video is talking about real returns so I'll throw this up as an example. 150 year history suggests a time period of 15 years or more for a real return on your equity investment.

Fi2rulhWYAEpWdm (699×489) (twimg.com)

From what I read and default pension fund data most investors aren't 100% equity regardless of better returns over decades. Default pension funds are closer to 50/50%.

Some US data over the last 100 years shows 2022 was one of the worst years in a long time.

FlUNZblXoAEcILa (900×446) (twimg.com)

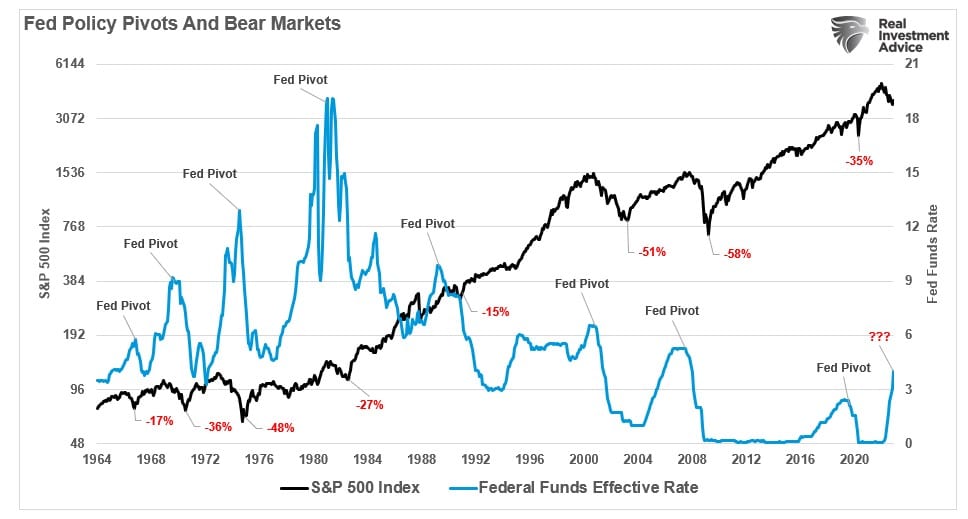

Nobody knows what happens next ? Inflation , base rates , mild or severe recession ? Markets keep guessing ? What we've got is rising rates worldwide and when will it stop ? What happens when they start cutting rates. Here's a few clues and again it's US data. FED cuts could well mean the economy is in trouble and a recession is looming . Grey shaded areas are the recessions.

FtXGZ-SWcAIML5p (900×557) (twimg.com)

It can be negative for equities ? How much nobody knows ?

Fed-Funds-and-Bear-Markets.jpg (968×519) (realinvestmentadvice.com)

Here's a long term chart of the UK bond VGOV without income . Recent falls have been heavy due to rising rates.

Vanguard UK Gilt UCITS ETF, UK:VGOV Advanced Chart - (LON) UK:VGOV, Vanguard UK Gilt UCITS ETF Stock Price - BigCharts.com (marketwatch.com)

Last two years have seen falls from 2500 to 1600. So if there's cuts in rates the fund should see a bounce which is good for holders. Trouble is how much will equities fall in a recession. Swings and roundabouts .

Vanguard UK Gilt UCITS ETF, UK:VGOV Advanced Chart - (LON) UK:VGOV, Vanguard UK Gilt UCITS ETF Stock Price - BigCharts.com (marketwatch.com)

1 -

Albermarle said:

I know you have been negative about bonds for some time now, and you were proved right big time in 2022.

However the forward outlook is maybe more positive than you think, according to Vanguard anyway, who are predicting a 5% year on year return for UK bonds for the next 10 years.

After some consideration my brain seems to have concluded the investment bond market has now had enough of a beating to provide a reasonably good entry point so with my equities recovered and after holding minimal bonds for a couple of years I have moved to 75% equities / 25% corporate bonds (similar to the above duration, and higher yeild now via a low cost workplace pension fund). We might not have reached the very bottom of the bond market but it's probably good enough and takes a little bit of risk off the table. Any further interest rate hikes would probably start affecting equities just as badly. Let's hope past performance is no indicator of future returns as the past 2 years of negative performance have wiped out such bond funds' previous 3 years of returns.GeoffTF said:https://www.vanguard.co.uk/professional/product/fund/bond/9125/uk-investment-grade-bond-index-fund-gbp-acc

Yield to maturity 5.3%. Average duration 6.0 years. A 5% p.a. return from UK bonds over the next ten years looks reasonable if interest rates do not change. Both the central banks and the market think that interest rates will fall, but they both have a bad record of predicting future interest rates. If interest rates do fall, the return from UK bonds will be more than 5%, and could outpace equity returns.

1

https://youtu.be/2dz_tgTQedQ

https://youtu.be/2dz_tgTQedQ

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards