We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Lloyds/Bank of Scotland/Halifax regular/monthly saver limits

Comments

-

As an alternative to @AmityNeons excellent work on the spreadsheets, and as a more general solution* to should I cancel (or renew in this case) my existing RS to instead take the new one (when you can only have one issue):It is only worth doing so if:(The increase in interest from the old to the new RS) / (the reduction in interest in moving funds from the old RS to an EA or feeder)is more than 2* (months into the RS / months left)e.g.If 6 months into RS, existing 5.25%, new 6.25%, with an EA at 3.25% to move the balance to1%/2% is not more than 2* (6/6)So if 6 months in, it's only worth moving if the increase in interest rate is more than 2* the loss of moving to the EA.Or in this case, would need to be a new RS @9.25%At 4 months in, break even is when increase in rate = decrease.

At 8 months the increase needs to be 4* the decrease.So, it's only worth moving if:Only just started the RSInterest increase old to new is largeInterest drop to EA is small, or you can use a higher interest notice account.You want to lock in the new interest for the next 12 months* this is a simplified solution, and will vary slightly depending when money is paid in, chance of 13th payment, days in each month etc, and what unknown options are available in the future.7 -

hi @ConsistentlyLost - are you suggesting it's possible to have a monthly saver with BOS without having a BOS current account, and to operate it via the Halifax app? How exactly is this done, curious to see if I can do this too! Thanks in advanceConsistentlyLost said:I've got the monthly saver with Bos and the regular saver with Halifax but I only have a bank account with Halifax so I've been operating them through my Halifax login. I've looked at how to transfer money from both into another savings account (I guess the everyday saver that halifax opened in conjunction with my reg saver) but ironically it only gives me the option to empty my Bos saver and not the Halifax. Would I have to wait for the Halifax reg saver to mature or is there a way to close it?TiA

0 -

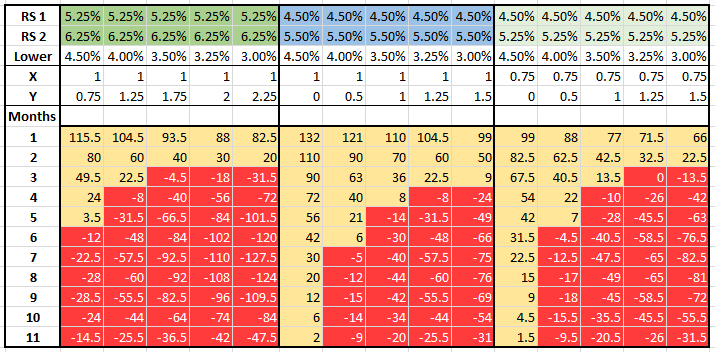

Good idea @k_man for something easily and generically applicable. Here's a much easier spreadsheet to interpret, for the three LBG Regular Savers (RS). It assumes deposits on the first of the month over 12 equal periods.

Check your interest rates, then look for the row representing how many months/deposits your current RS has. If the result is greater than 0 (yellow), it's mathematically beneficial to close/renew. If it's less than or equal to 0 (red), then it's not.

The chart uses the following formula:

(n − 12) * [(n − 13) * x + (2 * n * y)] > 0

X = higher RS interest rate minus current RS interest rate

Y = current RS interest rate minus lower (or easy access) interest rate

N = number of months/deposits of current RSIt essentially compares the average interest of keeping your RS for the full 12 months, versus the blended average interest of:

- Keeping your RS for a variable number of months (less than 12)

- Starting a new RS and contributing for the remaining months (up to and including month 12)

- The balance from the first RS being transferred to a lower interest account for the remaining months (up to and including month 12)

18 -

@AmityNeon got to applaud a fellow spreadsheet geek that uses conditional formatting and some decent formulae. Someone after my own heart lol.0

-

Only opened a Club reg saver and normal reg saver on 1st March for the OH and I, funded same day in full. Thinking of filling up again on 1st April and close them all down on 5th April to get the interest into this tax year (even if it's only a very little amount) and reopen and fund on the 6th April. Plenty of allowance left for this tax year, will both be easily over next year so that way it gives me full 12 months to fund and interest is credited to account against tax year 24/25

Does that make sense and does the process as mentioned earlier work and can be done the same day or do things need an overnight run?0 -

Although unlikely, Lloyds could attempt to patch the loophole if they notice that customers have had more than one of the same type opened in 12 months. The only other thing would be the small chance that they have some kind of outage on the 5th April - so maybe a couple of days before would be the way to go, if you want to wait still.pecunianonolet said:Only opened a Club reg saver and normal reg saver on 1st March for me and the OH and funded same day in full. Thinking of filling up again on 1st April. Close them all down on 5th April to get the interest into this tax year (even if it's only a very little amount) and reopen and fund on the 6th April. Plenty of allowance left for this tax year, will both be easily over next year.

Does that make sense?If you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.2 -

Could anyone tell me please, whether these accounts have to be funded via standing order, or at least the first payment has to be via S.O? Or can they be funded via internal transfer from the start?0

-

I've funded all mine (and previous versions of the regular savers) by internal transfer from the start for a couple of years without issues.Expotter said:Could anyone tell me please, whether these accounts have to be funded via standing order, or at least the first payment has to be via S.O? Or can they be funded via internal transfer from the start?2 -

My first RSs in October with LBG, I did an external payment in. My second LBG RSs opened a couple of days ago, I did an internal transfer in. Both worked fine for meExpotter said:Could anyone tell me please, whether these accounts have to be funded via standing order, or at least the first payment has to be via S.O? Or can they be funded via internal transfer from the start?If you want me to definitely see your reply, please tag me @forumuser7 Thank you.

N.B. (Amended from Forum Rules): You must investigate, and check several times, before you make any decisions or take any action based on any information you glean from any of my content, as nothing I post is advice, rather it is personal opinion and is solely for discussion purposes. I research before my posts, and I never intend to share anything that is misleading, misinforming, or out of date, but don't rely on everything you read. Some of the information changes quickly, is my own opinion or may be incorrect. Verify anything you read before acting on it to protect yourself because you are responsible for any action you consequently make... DYOR, YMMV etc.1 -

I'm a little wary of breaking the funding "rules" in case they decide to wriggle out of paying the interest due, so I have SO for the minimum amounts, topped up by manual faster payment.

I'm probably over thinking it, but...How's it going, AKA, Nutwatch? - 12 month spends to date = 3.24% of current retirement "pot" (as at end December 2025)1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards