We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

How to beat inflation?

sevenhills

Posts: 5,938 Forumite

I don't have the answer to the above, but most savings accounts have been losing value for over a decade.

Buying shares is quite complex for the risk averse, but savings rates instead of being just one or two percent short of inflation, savings accounts are now 5% or more below inflation.

I would guess most people on here have many thousands in savings that are losing value.

Does everyone just accept a loss in the value of their money, what would Martin Lewis say?

If you have £10,000 in a savings account, you are likely to lose £500 in value.

On average, Brits have £7,509 in savings. The average UK savings account has effectively lost £1,012 (13.5%) in value since 2017. Inflation as of July 2022 is 15 times higher than the average saving account rate. The inflation rate is currently 9.1%, which is the highest recorded figure since 1981. The Bank of England has projected that inflation will hit 11% in 2022, making savings accounts 10.41% less valuable within the year. In 2021, interest rates hit a record low of 0.35%, this is 97% less than the highest

Source: https://www.finder.com/uk/inflation-vs-savings

Buying shares is quite complex for the risk averse, but savings rates instead of being just one or two percent short of inflation, savings accounts are now 5% or more below inflation.

I would guess most people on here have many thousands in savings that are losing value.

Does everyone just accept a loss in the value of their money, what would Martin Lewis say?

If you have £10,000 in a savings account, you are likely to lose £500 in value.

On average, Brits have £7,509 in savings. The average UK savings account has effectively lost £1,012 (13.5%) in value since 2017. Inflation as of July 2022 is 15 times higher than the average saving account rate. The inflation rate is currently 9.1%, which is the highest recorded figure since 1981. The Bank of England has projected that inflation will hit 11% in 2022, making savings accounts 10.41% less valuable within the year. In 2021, interest rates hit a record low of 0.35%, this is 97% less than the highest

Source: https://www.finder.com/uk/inflation-vs-savings

1

Comments

-

He'd say that it's unfortunate but that options are limited - inflation risk is undoubtedly a significant issue just now (albeit 2023 isn't necessarily going to repeat 2022) as covered elsewhere, so the only ways to achieve returns anywhere near inflation entail other risks, but whether they're more or less acceptable depends on individual circumstances.sevenhills said:Does everyone just accept a loss in the value of their money, what would Martin Lewis say?

Edit: not ML's personal words as such but MSE echoes the above at https://www.moneysavingexpert.com/savings/investment-beginners/Although rates on savings accounts have seen some recent upward momentum, inflation is still soaring well above them. Understandably, the incentive to look elsewhere for decent returns remains strong.

Of course, everyone would prefer to make 5% on their cash but only if you take the right level of risk to suit you. We've said it above but there's no harm in repeating this till we're blue in the face...

Warning: Investing is risky and any money you put in could fall in value. Put bluntly, you could lose it all. There's a reason you'll see the phrase 'Past performance is no indicator of future success' – you've no guarantee your investment is going to do well.

2 -

If you are a cash only saver, there is no way to beat inflation, so yes you can only do your best to minimise the devaluation of your cash. The only way to beat inflation is to expose a fair proportion of your total wealth to the risks of the markets I’m afraid. The cash element of my pf (c10%) will return me 4-5% this year, but the investment element will hopefully do better, getting my average much nearer to inflation…but probably not beat it unless I increase my risk considerably which I’m unlikely to do.1

-

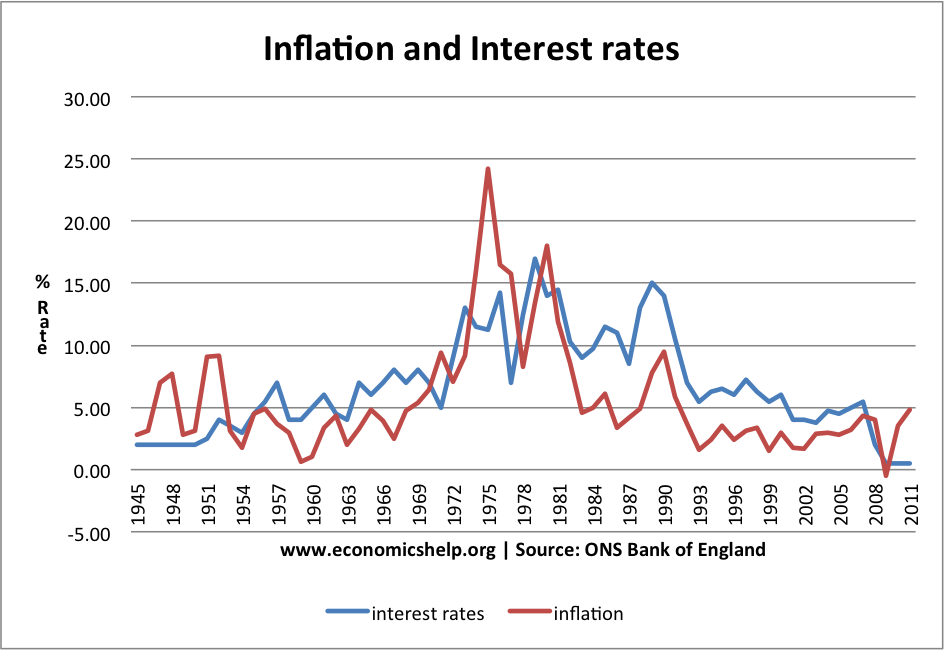

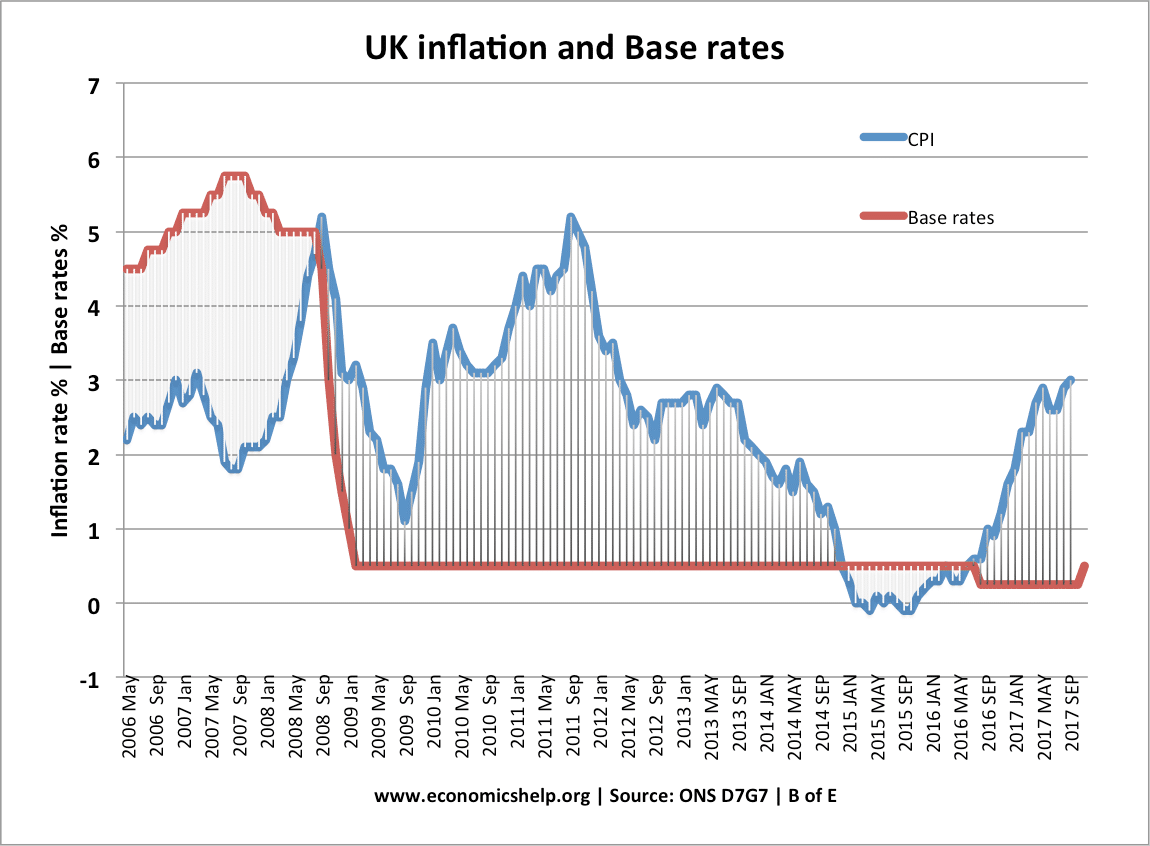

Blue (rates) above red (inflation) has been the case for many years but 2008 GFC ruined that for cash savers.

inflation-interest-rates-1945-2011.png (944×650) (economicshelp.org)

uk-base-rates-inflation.png (1150×846) (economicshelp.org)

Looking like Equities over a long period . Chart is UK for once as usually US.

FpZfVTWWcAEU7d4 (900×617) (twimg.com)

Nice little read.

The UK's biggest bond market crash - Monevator

EDIT..US history broken in periods.

200+ Years of Asset Class Returns (awealthofcommonsense.com)

2 -

Most people on this forum with large pension pots will hold most of their wealth in share based investments. The loss of real value from inflation of any cash will be accepted as the cost of having the money easily available and not subject to the volatility of the stock markets. In any case the returns from the investments should, over time, more than compensate one for the loss in real value of the cash.

The only way of guaranteeing inflation linking is through index linked government bonds with a maturity date set to when you need the money. However doing this could well be more complex than buying shares/funds and would not be as flexible as holding cash.1 -

If you can wait until 2036 for your money, you can beat inflation:

https://www.londonstockexchange.com/stock/TG36/united-kingdom/company-page

https://www.advfn.com/stock-market/london/TG36/stock-price

The price here is the "clean" price before indexation. You pay the "dirty" price after indexation. The clean price at maturity will be 100. You are paid at the dirty price after indexation. You can sell before maturity, but you will likely lose money if real interest rates have risen. Equities could do better, but at much higher risk. Fixed interest could do better too if interest rates fall.1 -

It has been argued that those who don't own property, don't have savings and claim benefits are the real winners. Generally their standard of housing & living has improved over the last 100 years irrespective of inflation & cost of living. We no longer have Victorian (or Edwardian) levels of real poverty and slum housing.1

-

sevenhills said:I don't have the answer to the above, but most savings accounts have been losing value for over a decade.

Buying shares is quite complex for the risk averse, but savings rates instead of being just one or two percent short of inflation, savings accounts are now 5% or more below inflation.

I would guess most people on here have many thousands in savings that are losing value.

Does everyone just accept a loss in the value of their money, what would Martin Lewis say?

If you have £10,000 in a savings account, you are likely to lose £500 in value.

On average, Brits have £7,509 in savings. The average UK savings account has effectively lost £1,012 (13.5%) in value since 2017. Inflation as of July 2022 is 15 times higher than the average saving account rate. The inflation rate is currently 9.1%, which is the highest recorded figure since 1981. The Bank of England has projected that inflation will hit 11% in 2022, making savings accounts 10.41% less valuable within the year. In 2021, interest rates hit a record low of 0.35%, this is 97% less than the highest

Source: https://www.finder.com/uk/inflation-vs-savingsMartin Lewis has mentioned it multiple times, he is not an investment guru. Also it is suggested from the forum he founded "Money Saving Expert",I personally listen to the views of many people but I make up my own mind. I listen more focus to the people who have track records of making money, not random people from the internet.There is already general truth that investing in equity will beat inflation in the long run. Also equity outperform bond and saving in the long run and beats inflation. So increasing equity holdings and reducing the bond/saving people will help more chance to beat inflation. Also many of multi billionaires proven investors dislike bonds and if they do invest in Bonds it is only for a small percentage and for a short term.So no need to search for the holy grail as there is already a proven method to beat inflation in the long run. A few people could beat inflation by a large degree such as investing in properties, trading, open business etc although a few fail as well. So certainly imo this consideration will depend of people personal circumstances, time horizon, risk tolerance, etc1 -

These charts of inflation versus savings rates make extremely depressing reading for those who thought their bank deposits were 'safe'. And this ignores the losses in savings value since July 2022.

Really Bank/BS interest rates should be advertised relative to inflation, then it might shake people up to demand more from the financial institutions.

I wish I'd kept all my NS&I Index linked bonds!

3 -

Personally I would not be surprised if fixed term savings taken out in the last 4 months or so, start to beat/equal inflation by the end of this year, as inflation is predicted to start dropping quickly. It could even be that those with long term fixes at 4 to 5% may well find themselves ahead of inflation for a significant period.CheekyMikey said:If you are a cash only saver, there is no way to beat inflation, at the moment so yes you can only do your best to minimise the devaluation of your cash. The only way to beat inflation is to expose a fair proportion of your total wealth to the risks of the markets I’m afraid. The cash element of my pf (c10%) will return me 4-5% this year, but the investment element will hopefully do better, getting my average much nearer to inflation…but probably not beat it unless I increase my risk considerably which I’m unlikely to do.

Nobody knows for sure of course, as is the same with the outlook for investments, which may or may not quickly make up the double losses endured in 2022 ( inflation and markets down at the same time)3 -

That loss in value of cash savings has been more than compensated for in property values.sevenhills said:I don't have the answer to the above, but most savings accounts have been losing value for over a decade.

Buying shares is quite complex for the risk averse, but savings rates instead of being just one or two percent short of inflation, savings accounts are now 5% or more below inflation.

I would guess most people on here have many thousands in savings that are losing value.

Does everyone just accept a loss in the value of their money, what would Martin Lewis say?

If you have £10,000 in a savings account, you are likely to lose £500 in value.

On average, Brits have £7,509 in savings. The average UK savings account has effectively lost £1,012 (13.5%) in value since 2017. Inflation as of July 2022 is 15 times higher than the average saving account rate. The inflation rate is currently 9.1%, which is the highest recorded figure since 1981. The Bank of England has projected that inflation will hit 11% in 2022, making savings accounts 10.41% less valuable within the year. In 2021, interest rates hit a record low of 0.35%, this is 97% less than the highest

Source: https://www.finder.com/uk/inflation-vs-savings0

{kind=link}

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.4K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604.1K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards