We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

S&S ISA limit fluctuation

PloughmansLunch

Posts: 699 Forumite

Hi all,

I apologise if I come across as a bit of a thickie but I’d like some advice.

I recently sold off some funds from my Vanguard S&S ISA and transferred the cash into my general account - the reason being it was <£1k and at a very tiny loss so no tax benefit wrapped, and I wanted to be able put the maximum into a cash ISA for this financial year and have filled that up to £20k. Both the Vanguard and the Virgin ISAs are flexible so hopefully I can rectify anything if need be before year end.

I apologise if I come across as a bit of a thickie but I’d like some advice.

I recently sold off some funds from my Vanguard S&S ISA and transferred the cash into my general account - the reason being it was <£1k and at a very tiny loss so no tax benefit wrapped, and I wanted to be able put the maximum into a cash ISA for this financial year and have filled that up to £20k. Both the Vanguard and the Virgin ISAs are flexible so hopefully I can rectify anything if need be before year end.

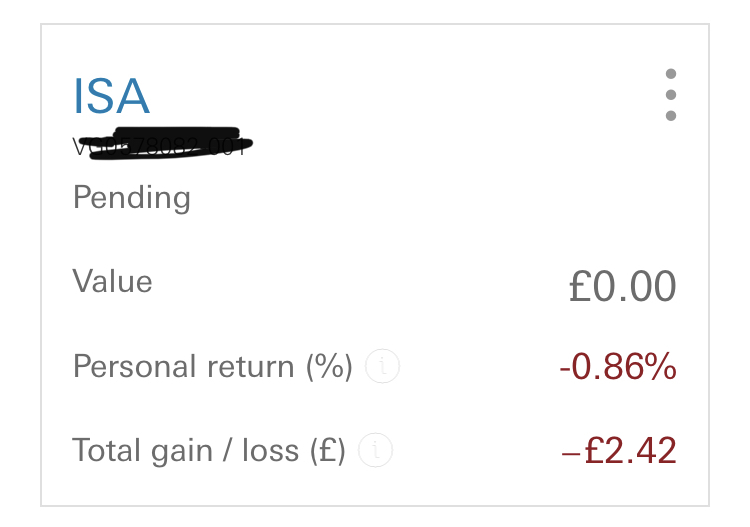

If the S&S ISA has effectively been cleared out shouldn’t it now be at £0 will a full tax allowance that I can use for the cash ISA? As per the screenshots it’s got two different figures anyway so I’m not sure what the actual amount to be reported to HMRC would be.

Any help would be greatly appreciated. Do I need to do anything or is it ok to leave it? It seems silly to use up my HMRC youve been a naughty boy letter over what is basically pennies, but I also like having a nice round figure for my cash ISA balance.

0

Comments

-

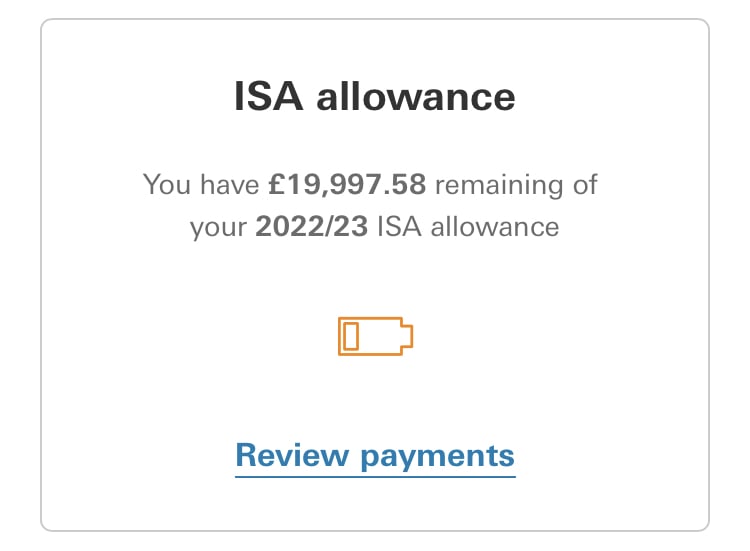

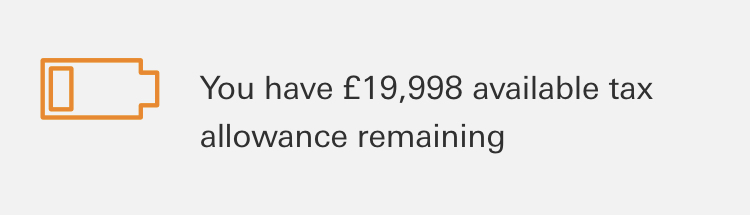

The Vanguard S&S ISA is a flexible one, which allows you to withdraw money and replace it within the same tax year without it counting towards your annual ISA contribution allowance, so the remaining allowance figure is taking account of that. If you've withdrawn everything from your Vanguard ISA and paid £20K into a cash one, with no contributions to any other ISAs during this tax year, then you haven't broken any rules....1

-

If the S&S ISA has effectively been cleared out shouldn’t it now be at £0 will a full tax allowance that I can use for the cash ISA? As per the screenshots it’s got two different figures anyway so I’m not sure what the actual amount to be reported to HMRC would be.Depends on how much you draw out.

£20,000 brought it to zero but if you drew £19,997 then that is what your ISA allowance becomes.

Allowance - minus amount contributed + withdrawals (+ certain charges depending on platform).

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.0 -

That's good news - red numbers always worry me. So the loss discrepancy is presumably just showing the difference in my submitted sell order and when the funds were sold and not actually relevant to HMRC? I haven't paid in to any other ISAs this year and Vanguard is totally empty despite the screenshots, so to all intents and purposes the Vanguard is now a nil value, is that correct?0

-

Yes, HMRC aren't interested in gains or losses within ISAs, and only need to know about contributions (net contributions for flexible ISAs like Vanguard's). If your Vanguard account has a zero balance then that signifies that if anything was paid in during this tax year then it must have been withdrawn, so it'll be reported as zero to HMRC.PloughmansLunch said:That's good news - red numbers always worry me. So the loss discrepancy is presumably just showing the difference in my submitted sell order and when the funds were sold and not actually relevant to HMRC? I haven't paid in to any other ISAs this year and Vanguard is totally empty despite the screenshots, so to all intents and purposes the Vanguard is now a nil value, is that correct?

Edit: as pointed out by @dunstonh, if you withdrew less than you paid in this year then you have used some allowance.1 -

Fantastic, thanks for your help0

-

It will be reported as £2.42 ISA allowance used in this case.eskbanker said:

Yes, HMRC aren't interested in gains or losses within ISAs, and only need to know about contributions (net contributions for flexible ISAs like Vanguard's). If your Vanguard account has a zero balance then that signifies that if anything was paid in during this tax year then it must have been withdrawn, so it'll be reported as zero to HMRC.PloughmansLunch said:That's good news - red numbers always worry me. So the loss discrepancy is presumably just showing the difference in my submitted sell order and when the funds were sold and not actually relevant to HMRC? I haven't paid in to any other ISAs this year and Vanguard is totally empty despite the screenshots, so to all intents and purposes the Vanguard is now a nil value, is that correct?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

Sorry, yes, you're right - OP, do you agree that £2.42 represents the difference between what you paid in during this tax year and what you withdrew?dunstonh said:

It will be reported as £2.42 ISA allowance used in this case.eskbanker said:

Yes, HMRC aren't interested in gains or losses within ISAs, and only need to know about contributions (net contributions for flexible ISAs like Vanguard's). If your Vanguard account has a zero balance then that signifies that if anything was paid in during this tax year then it must have been withdrawn, so it'll be reported as zero to HMRC.PloughmansLunch said:That's good news - red numbers always worry me. So the loss discrepancy is presumably just showing the difference in my submitted sell order and when the funds were sold and not actually relevant to HMRC? I haven't paid in to any other ISAs this year and Vanguard is totally empty despite the screenshots, so to all intents and purposes the Vanguard is now a nil value, is that correct?1 -

Yes, I suppose so as the prices went down so will probs have to withdraw a couple of quid from Virgin to be safe. Virgin do a S&S paper transfer form via post but that seemed like a faff, and if the funds had to be sold beforehand it would be the same outcome I guess.eskbanker said:

Sorry, yes, you're right - OP, do you agree that £2.42 represents the difference between what you paid in during this tax year and what you withdrew?dunstonh said:

It will be reported as £2.42 ISA allowance used in this case.eskbanker said:

Yes, HMRC aren't interested in gains or losses within ISAs, and only need to know about contributions (net contributions for flexible ISAs like Vanguard's). If your Vanguard account has a zero balance then that signifies that if anything was paid in during this tax year then it must have been withdrawn, so it'll be reported as zero to HMRC.PloughmansLunch said:That's good news - red numbers always worry me. So the loss discrepancy is presumably just showing the difference in my submitted sell order and when the funds were sold and not actually relevant to HMRC? I haven't paid in to any other ISAs this year and Vanguard is totally empty despite the screenshots, so to all intents and purposes the Vanguard is now a nil value, is that correct?

I'm sure the answer is no, but out of interest does that mean that it's possible if you have decent gains in S&S then sold in the same tax year to have a negative allowance?0 -

Not sure what you actually mean by a 'negative allowance' here? If you withdraw more than you paid in that would be a negative net contribution but that doesn't actually equate to a negative allowance as such....PloughmansLunch said:I'm sure the answer is no, but out of interest does that mean that it's possible if you have decent gains in S&S then sold in the same tax year to have a negative allowance?0 -

Yes, that was what I was trying to get at. Thanks for clarifyingeskbanker said:

Not sure what you actually mean by a 'negative allowance' here? If you withdraw more than you paid in that would be a negative net contribution but that doesn't actually equate to a negative allowance as such....PloughmansLunch said:I'm sure the answer is no, but out of interest does that mean that it's possible if you have decent gains in S&S then sold in the same tax year to have a negative allowance?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.6K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.5K Spending & Discounts

- 247.5K Work, Benefits & Business

- 604.4K Mortgages, Homes & Bills

- 178.6K Life & Family

- 261.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards