We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

First Direct 7% Linked Savings Account

Comments

-

That is how they work.bmcdonagh said:I’ve just opened a First Direct bank account (mainly for the switch bonus) and decided to look at opening the linked savings account which offers a huge 7% interest.

I just wanted to make clear that you cannot make partial withdrawals on this account. It also looks as though the 7% lasts for 12 months only, and you then need to find a new home for your savings (at least, that’s how I read it).

Whilst this is still a great offer for someone saving for a long term goal, I think it’s worth mentioning and perhaps the main article in the website could mention the inability to make partial withdrawals as that may influence some people’s decision?Personally, I have minor savings that I keep as a sort or ‘house fund’ for maintenance that pops up during the year so I would expect to dip into it a few times a year. This savings account wouldn’t work for me. Just thought it worth mentioning.Regular Saver Account

Get into a good savings habit

And the future you will say thanks. Put away between £25 to £300 each month, for a fixed 12 month term, and we'll give you a fixed rate of 7.00% AER/gross p.a.

- 7.00% AER/Gross p.a. fixed for 12 months

- save between £25 and £300 a month, up to £3,600 per year

- change the amount of your standing order at any time

Life in the slow lane0 -

@bmcdonagh, if Regulars Savers without withdrawals before maturity don't work for you, there are Regular Savers which do allow withdrawals and/or closure before maturity without penalty. They don't pay quite as much as 7% but still more than easy access accounts, and the drip feed method can make a substantial difference to the amount of interest you can earn.bmcdonagh said:Personally, I have minor savings that I keep as a sort or ‘house fund’ for maintenance that pops up during the year so I would expect to dip into it a few times a year. This savings account wouldn’t work for me. Just thought it worth mentioning.

A complete list of RSs is maintained by a friendly forumite here: https://forums.moneysavingexpert.com/discussion/6106986/regular-savings-accounts-the-best-currently-available-list/p1

It is mentioned - and more importantly, the Key Product Information which all providers make available for all their products does detail whether and how withdrawals/closures work.bmcdonagh said:

Whilst this is still a great offer for someone saving for a long term goal, I think it’s worth mentioning and perhaps the main article in the website could mention the inability to make partial withdrawals as that may influence some people’s decision?

0 -

I have done a rough calculation on a possible strategy for achieving the best overall interest rate over 12 months taking a view of future interest rates, given that successive monthly deposits have an aer reducing by 1/12th of 7% each month.

If £300 is deposited in each of 12 successive months the interest achieved is £136.50 (FD website) for £3,600 deposited, giving an overall return of 3.8%.

However if £300 is deposited in each of the first 7 months(*) only and £25 in each of the next 5 months the interest achieved is £122.50 for £2,225 deposited, giving an overall return of 5.5%. To me this is more attractive with less committed when returns are diminished.

(*) the 8th deposit has an effective interest rate of 2.91% (below easy access today).

0 -

So in each of the latter five months, instead of depositing the remaining £275 to earn 7%, what would you do instead?dealyboy said:I have done a rough calculation on a possible strategy for achieving the best overall interest rate over 12 months taking a view of future interest rates, given that successive monthly deposits have an aer reducing by 1/12th of 7% each month.

If £300 is deposited in each of 12 successive months the interest achieved is £136.50 (FD website) for £3,600 deposited, giving an overall return of 3.8%.

However if £300 is deposited in each of the first 7 months(*) only and £25 in each of the next 5 months the interest achieved is £122.50 for £2,225 deposited, giving an overall return of 5.5%. To me this is more attractive with less committed when returns are diminished.

(*) the 8th deposit has an effective interest rate of 2.91% (below easy access today).3 -

So, you take out a FD Reguar saver, feeding from a Chase 3% saver. Rough sums:

You're suggesting that you would be better off dropping the FD depostit to £25 from months 7 onwards:

Your money is always going to be better off in a 7.00% account over a 3.00% account. You're £13.75 worse off.Mortgage and debt free. Building up savings...3 -

I am afraid, this s is not how it works. The AER of the FD account is 7% for the duration, not any less.dealyboy said:I have done a rough calculation on a possible strategy for achieving the best overall interest rate over 12 months taking a view of future interest rates, given that successive monthly deposits have an aer reducing by 1/12th of 7% each month.

If £300 is deposited in each of 12 successive months the interest achieved is £136.50 (FD website) for £3,600 deposited, giving an overall return of 3.8%.

However if £300 is deposited in each of the first 7 months(*) only and £25 in each of the next 5 months the interest achieved is £122.50 for £2,225 deposited, giving an overall return of 5.5%. To me this is more attractive with less committed when returns are diminished.

(*) the 8th deposit has an effective interest rate of 2.91% (below easy access today).

Goes without saying that you do not get interest for money that you have not deposited. You therefore cannot compare the return of a lump sum you deposit on day one for 12 months with the return you get on money that you deposit month on month. It's also illogical to suggest depositing less money into a higher paying account would be a better approach.

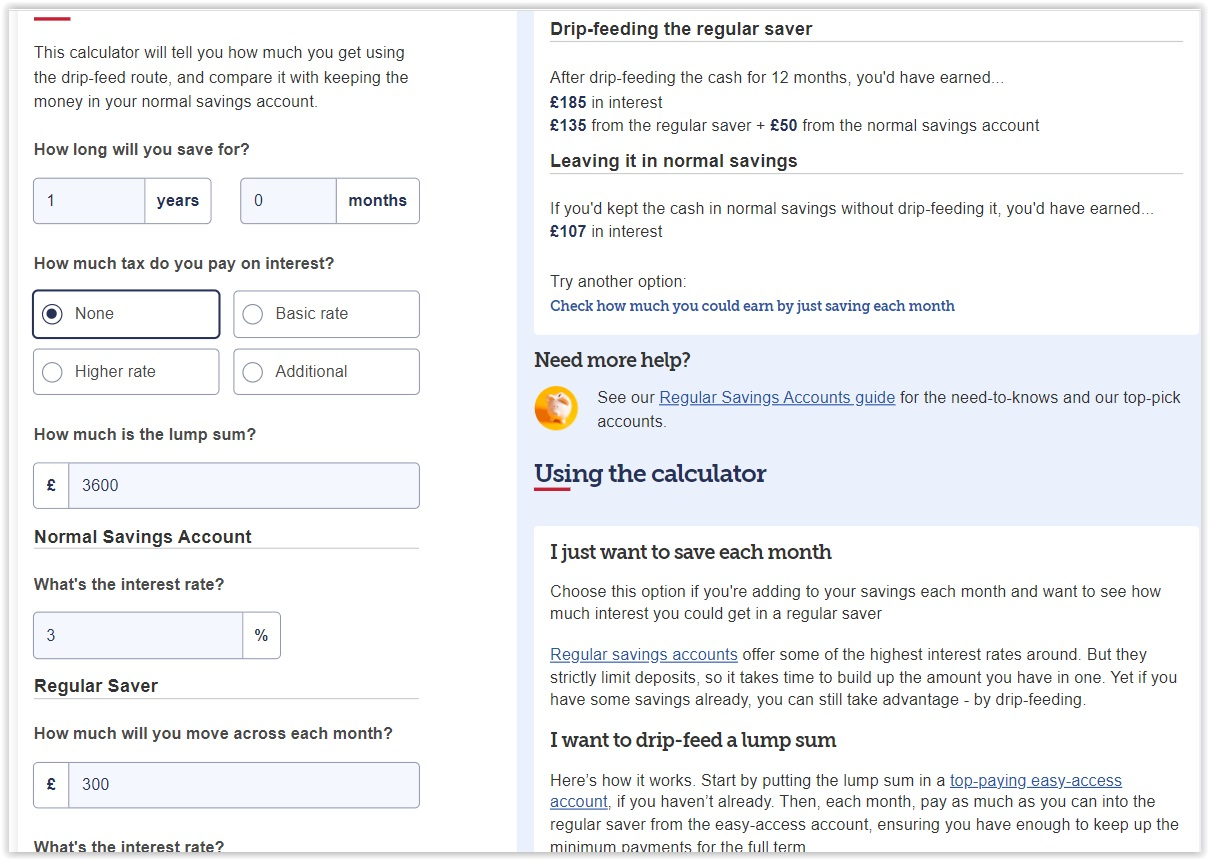

There is, however, the drip feed method that I have mentioned above. This can be deployed on a lump sum to increase the overall return. The MSE Regular saver calculator can be used to work out the approx returns. It assumes the drip feed happens on each first of a month for 12 months. Here is a realistic example, feeding a monthly £300 from a 3% easy access account into the FD RS: 4

4 -

... there is no remaining £275, you just don't deposit the max £300 but instead the min £25 per month.AmityNeon said:

So in each of the latter five months, instead of depositing the remaining £275 to earn 7%, what would you do instead?dealyboy said:I have done a rough calculation on a possible strategy for achieving the best overall interest rate over 12 months taking a view of future interest rates, given that successive monthly deposits have an aer reducing by 1/12th of 7% each month.

If £300 is deposited in each of 12 successive months the interest achieved is £136.50 (FD website) for £3,600 deposited, giving an overall return of 3.8%.

However if £300 is deposited in each of the first 7 months(*) only and £25 in each of the next 5 months the interest achieved is £122.50 for £2,225 deposited, giving an overall return of 5.5%. To me this is more attractive with less committed when returns are diminished.

(*) the 8th deposit has an effective interest rate of 2.91% (below easy access today).

0 -

dealyboy said:AmityNeon said:dealyboy said:I have done a rough calculation on a possible strategy for achieving the best overall interest rate over 12 months taking a view of future interest rates, given that successive monthly deposits have an aer reducing by 1/12th of 7% each month.

If £300 is deposited in each of 12 successive months the interest achieved is £136.50 (FD website) for £3,600 deposited, giving an overall return of 3.8%.

However if £300 is deposited in each of the first 7 months(*) only and £25 in each of the next 5 months the interest achieved is £122.50 for £2,225 deposited, giving an overall return of 5.5%. To me this is more attractive with less committed when returns are diminished.

(*) the 8th deposit has an effective interest rate of 2.91% (below easy access today).

So in each of the latter five months, instead of depositing the remaining £275 to earn 7%, what would you do instead?

... there is no remaining £275, you just don't deposit the max £300 but instead the min £25 per month.

I currently transfer £300 to my First Direct current account so the standing order to the Regular Saver can be paid. What should I do from month 8 onwards? How do I best make use of the £275 that will no longer go to the Regular Saver?

2 -

... Sorry for my wrong thinking and thank you to:

@AmityNeon twice

@financialbliss for straightforward explanation

@Band7 for explanation and guidance

db. 3

3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards