We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Changing how I Budget

Comments

-

Yes it went a bit crazy didn't it. It is perfectly fine for you to quote if responding to a post but it looks like several posts have been quoted in one response so make sure you only click quote once. I will try and edit for you or get it deleted.Peterxxxxxx said:Dear enthusiastic saver

Thank you for your feedback. Also my apology about the crazy post.

In what context would it be appropriate to use the quote function?

Can I respond to individual post?

🙂🙏I’m a Forum Ambassador and I support the Forum Team on the Debt free Wannabe, Budgeting and Banking and Savings and Investment boards. If you need any help on these boards, do let me know. Please note that Ambassadors are not moderators. Any posts you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own and not the official line of MoneySavingExpert.

Save £12k in 2026 Challenge £12000/£9500

365 day 1p Challenge 2026 £667.95/£374.01

Click on this link for a Statement of Accounts that can be posted on the DebtFree Wannabe board: https://lemonfool.co.uk/financecalculators/soa.php1 -

Peterxxxxxx said:

I want to change how I budget. I am single and will be 73 next month. I use an app to manage my finances. My belief is that I need to rewrite my my budget.

Perhaps something has been lost in the above editing, but surely, unless any of these factors have changed significantly recently, they'll all have been present when you set up your existing budget? You haven't yet given any clues about why you feel the need to rewrite your budget, i.e. in what specific ways is it deficient, or how isn't it adequately supported by whichever tool(s) you use? For example, is the issue that you're not sticking to your budget perhaps, or maybe that it's not reflecting all of your spend?Peterxxxxxx said:There a number of factors contributing to my situation. Single, retired, low income, spiriting costs, prioritising essential payments and age 72.

Paying for essential items. Calculating what is the total. What money is leftover for nonessential items.

Keeping accurate records of income and expenditure. This would be to have an account financial picture. Also, supporting my personal health.2 -

I have a spreadsheet of all my bills including a savings payment and an allowance per week. When I get paid I split it all into pots in the Monzo app, the bills come directly out of the bills poit and each week (7 or 8 days) I withdraw from one of the weekly pots and make that last the week. I find it easier to let the app do it all as I never forget anything and all it takes is a fingerprint to see how much I have left that week,

1 -

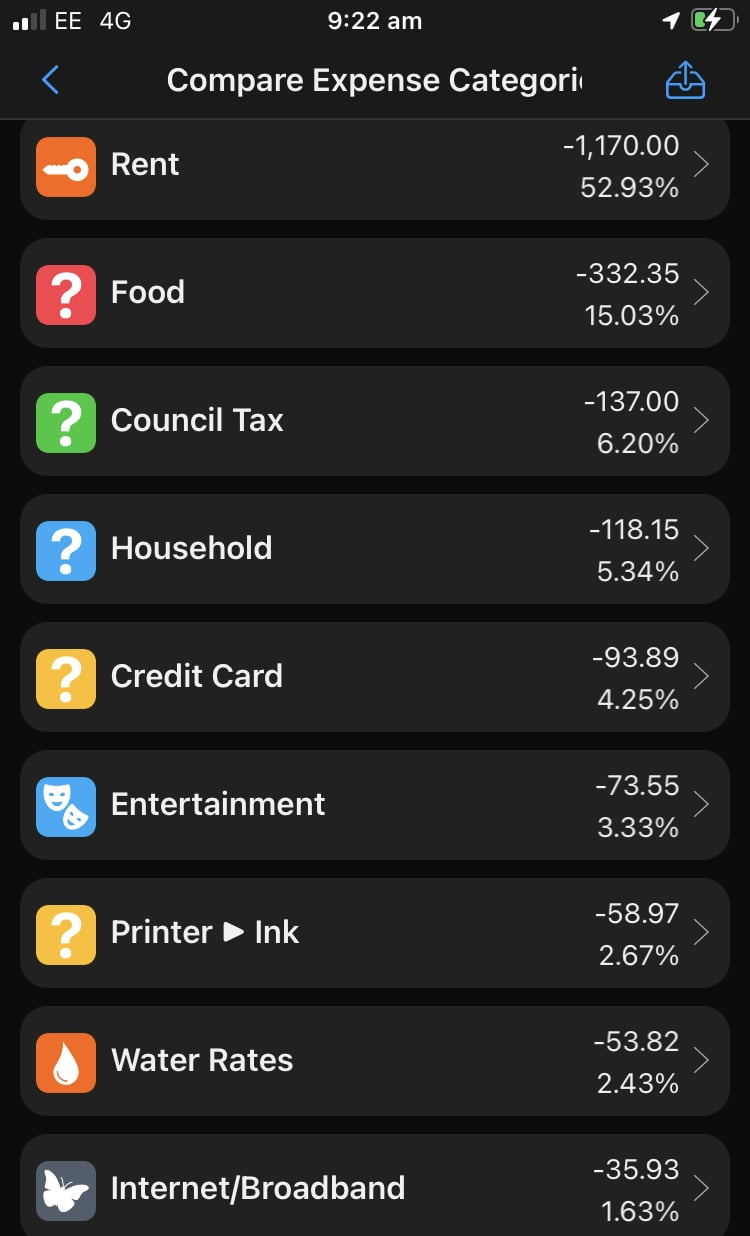

This is a screenshot of part of my spending in November. I’m new to posting to this forum. I finding out what I can do.

This is a screenshot of part of my spending in November. I’m new to posting to this forum. I finding out what I can do.

Rob thank you for your comments.

🙂🙏0 -

What type of files can I upload? I’m able to produce PDF files. But I don’t appear to be able to upload them to the board. Is it image files that I can upload?

0 -

You can post images but not files.

Once you have been a member for a bit longer, you can also post links. So if your PDF etc is online somewhere, e.g. on Google Drive, you can post a link.

But before posting lots of data, you should clarify what your objective is. Are you trying to reduce your spending? Are you having discrepancies between your plan and your actual? Are you looking for an easier/better tool than the one you are using currently - and what is wrong with your current tool? Etc etc0 -

I have 3 bank accounts which may not work for everyone, but works for me. My main salary goes into one bank account and I work out what my bills/DDs are for month, and leave myself a £50 buffer. I check it regularly. I transfer any excess to another account that pays interest. My other income also goes into that account.

I then have Monzo for day to day spending and transfer a weekly allowance there. Anything I haven't spent goes into pots. I also have my penny challenge and my 52 week challenge in there as well.

Debts :Paypal £1981.32

Monzo Loan £4278.16

Virgin CC £2137 0% until Dec 23

HSBC £5471.01 0% until Feb 2025

Emergency pot £404.47/2500

1p Savings Challenge £1.45/660

52 week Savings: £22.00/14000 -

Are your current account paying you interest? Wouldn't you do better if your bills/DD money was in a Chase Savings account, which uniquely allows DDs, and pays one of the top interest rates now? Also, wouldn't you be able to make use of the Chase cashback, or of the Kroo current account (2% interest) for your day to day spending. These account are likely to pay you more than a penny challenge.Arwen said:I have 3 bank accounts which may not work for everyone, but works for me. My main salary goes into one bank account and I work out what my bills/DDs are for month, and leave myself a £50 buffer. I check it regularly. I transfer any excess to another account that pays interest. My other income also goes into that account.

I then have Monzo for day to day spending and transfer a weekly allowance there. Anything I haven't spent goes into pots. I also have my penny challenge and my 52 week challenge in there as well.0 -

I don't understand budgets, for me the idea is to spend as little money as necessary. If I set a budget, then I would find myself spending more money to use up the budget. What happens when you have blown your food budget, do you stop eating?

You can't budget for emergencies either, will I need a new boiler this year or next? How much should I put by for that?2 -

This is my understanding of a budget.How much money I’m going to spend on a particular type of purchase. An example would be how much I spend on water rates. Knowing how much I’ve spent in previous years, allows me to forecast the future cost.Another example would be how much electricity and how much it cost me monthly. I have a record of the amount of electricity I use monthly. I can then forecast my usage. This then allows me to calculate what the increase in cost would be given price rises1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards