We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Energy how do they justify your DD increase

Comments

-

Energy suppliers don't force you to set up a direct debit, nor do they refuse to supply you if you don't have a direct debit, so the alleged comparison doesn't hold.

And several food businesses do offer a comparable voluntary arrangement, look at the christmas savings stamp schemes.3 -

They do indeed. And it's pretty fascinating that Tesco do a far better job with their Christmas saver scheme than energy companies do.

The money is held in a trust separate from Tesco itself, and you can get it back at any time until October (just before the "bonus" is paid in) as a pre-paid cash card.

https://www.tesco.com/help/sections/10865630418841-Clubcard-Christmas-Savers

Like you, I'd be all for energy companies adopting this model!0 -

I'm not sure who you are referring to, in my case it was either accept the DD and they chose how much it would be OR standing order with ridiculously inflated rates. Or i guess move so not a great deal of choice, as far as I'm concerned it's forcing a direct debit on you via the back door.[Deleted User] said:Energy suppliers don't force you to set up a direct debit, nor do they refuse to supply you if you don't have a direct debit, so the alleged comparison doesn't hold.

And several food businesses do offer a comparable voluntary arrangement, look at the christmas savings stamp schemes.

0 -

Ofgem has just rejected this model because it would have required energy suppliers to put consumer credits into escrow. If suppliers are unable to use customer credits to run their businesses (cashflow) then this would just increase prices to consumers as suppliers would have to borrow. The other reason for not going ahead with escrow is that it would discourage new entrants from entering the market.deano2099 said:They do indeed. And it's pretty fascinating that Tesco do a far better job with their Christmas saver scheme than energy companies do.

The money is held in a trust separate from Tesco itself, and you can get it back at any time until October (just before the "bonus" is paid in) as a pre-paid cash card.

https://www.tesco.com/help/sections/10865630418841-Clubcard-Christmas-Savers

Like you, I'd be all for energy companies adopting this model!

What many consumers fail to appreciate is that suppliers pay their wholesalers in advance of supply. Perhaps what is needed here is a simple change to the credit balance scheme: perhaps all consumers should hold sufficient credit in the account to cover in full the cost of the following month’s supply. That said, this forum would be full of complaints about variable DDs each month.

The present DD scheme isn’t perfect but it works for millions of consumers. Given that credit balances are 100% protected, the consumer will not lose out should a supplier fail.0 -

Well, being in a separate trust is not beneficial given the already existing consumer protection (and could actually be detrimental by making hedging more expensive), and getting credit back in cash just before winter doesn't seem like a sensible idea.

Not something I'd advocate for energy supply.0 -

“Food, etc…” - there are many essentials people have to pay for - for many these days a cheap sim only contract and some form of home broadband for example, water rates, travel and transport, insurances….had I named all the essentials it might have been a rather long list - hence the entirely correct use of “etc”, which I’m sure was clearly understood by pretty much everyone. My point was that generally speaking it’s those who are able to “save for a rainy day” that regard those who aren’t as in some way profligate - with suggestions that they just need to try harder, have more self control”.pseudodox said:rent, council tax, food etc have to paid for first, and then there is no money left.

So what do you pay the energy FDD from?

So far as I know nobody is likely to have a contract with Tesco where they are tied to that store as their sole provider of food and drink? If they did, then there very likely would be a DD set up for it.deano2099 said:

But Tesco don't look at your Clubcard and say "you spend £300 on food every month, so you need to set up a direct debit for that amount and we'll give you £300 of vouchers you can spend on food every month in return" and then refuse to sell you food if you say that you don't want to spend that much next month and are going to cut back.EssexHebridean said:

Being able to save for a rainy day is wonderful - but you need a degree of financial privilege, ie surplus income beyond your essential expenditure, to be able to do so. With bills increasing rapidly in the last year, even many of those who might have been able to do that a short while ago would struggle to do so now. Sometimes it’s not a “lack of self discipline” at all - it’s that rent, council tax, food etc have to paid for first, and then there is no money left.pseudodox said:So as a tenant you do have the choice to move, with of course a polite notification to the landlord. OVO will not offer whole bill payments. Though in view of increasing numbers being unhappy with FDD it might one day become an option companies have to legally offer.

I just don't get why people prefer to hand money over rather than keep it in their own account - in perhaps a dedicated savings pot, especially in view of the BoE rise again in interest rates. Are people now so lacking in self-discipline that they cannot avoid the tempation to spend every last penny rather than save some for a rainy (or cold) day? I have a money box that was my grandmothers - six slotted compartments into which she distributed her then (cash) pension each week. Rent, Electric, Coal, Water, Food, Other. There was always the money to pay any bill that arrived. Only "Other" could be dipped into for non-essentials. If it was empty she had to wait to purchase a new frock, or have her hair done.

The point of fixed direct debits is to help the customer spread their payments evenly over 12 months. They're not there to force customers to prioritise electric/gas over food. It happens to have that effect, and there's an argument to say that's a positive design accident (there are more food banks than warm banks, after all) but it certainly wasn't the intent of the system.There are currently more Foodbanks than warm banks because there has been a requirement for Foodbanks for longer, for various reasons.If the OP’s billing period begins/ends in January by the way, then he can be reasonably certain to be in debt by the end of it if as he seems to think his current level of DD pretty much covers his average use. If it had begun/ended in September, as might behave been assumed, then he very probably wouldn’t have been.🎉 MORTGAGE FREE (First time!) 30/09/2016 🎉 And now we go again…New mortgage taken 01/09/23 🏡

Balance as at 01/09/23 = £115,000.00 Balance as at 31/12/23 = £112,000.00

Balance as at 31/08/24 = £105,400.00 Balance as at 31/12/24 = £102,500.00

£100k barrier broken 1/4/25

Balance as at 31/08/25 = £ 95,450.00. Balance as at 31/12/25 = £ 91,100.00

SOA CALCULATOR (for DFW newbies): SOA Calculatorshe/her0 -

Well, I was most likely referring to the post that talked about refusing to supply, and about a food business, otherwise my post would have been a little odd, but anyway..MikeJXE said:

I'm not sure who you are referring to, in my case it was either accept the DD and they chose how much it would be OR standing order with ridiculously inflated rates. Or i guess move so not a great deal of choice, as far as I'm concerned it's forcing a direct debit on you via the back door.Deleted_User said:Energy suppliers don't force you to set up a direct debit, nor do they refuse to supply you if you don't have a direct debit, so the alleged comparison doesn't hold.

And several food businesses do offer a comparable voluntary arrangement, look at the christmas savings stamp schemes.

Saying "you can pay the direct debit prices if you have a direct debit, or you can have a standing order and pay the standing order prices, or you can move to another supplier" is pretty much the opposite of "forcing a direct debit on you". It's giving you free choice between several options!

Saying "I demand to pay the way I want, at the price I want, with the credit balance I want, especially for me no matter what the rules or whatever you do with other customers" on the other hand....1 -

Dolor said:

The present DD scheme isn’t perfect but it works for millions of consumers. Given that credit balances are 100% protected, the consumer will not lose out should a supplier fail.deano2099 said:They do indeed. And it's pretty fascinating that Tesco do a far better job with their Christmas saver scheme than energy companies do.

The money is held in a trust separate from Tesco itself, and you can get it back at any time until October (just before the "bonus" is paid in) as a pre-paid cash card.

https://www.tesco.com/help/sections/10865630418841-Clubcard-Christmas-Savers

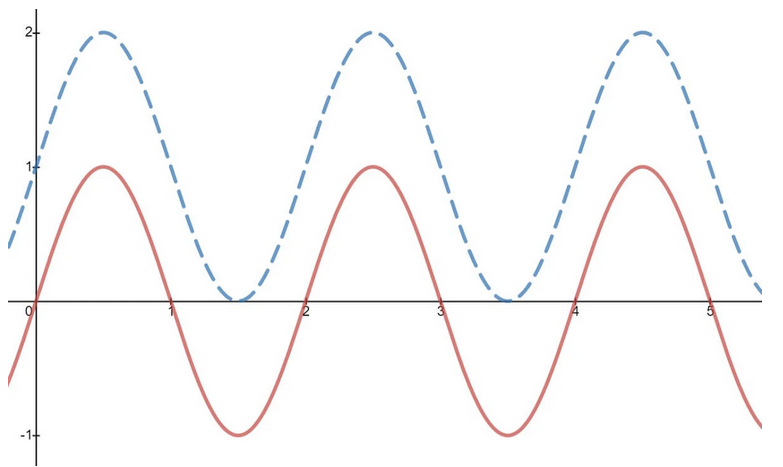

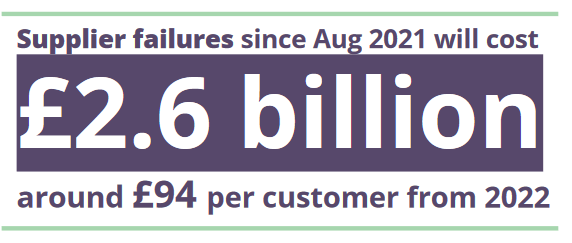

Like you, I'd be all for energy companies adopting this model!That's debatable.There's been a subtle change in DDs, not one that benefits the consumer. Originally a fixed DD meant that you were in credit during the summer and in debit during the winter. It worked reasonably well provided that it was set correctly and your energy usage was as expected, as shown by the red line. Above all, it was fair to both parties. However, when dozy Ofgem let almost anyone set up an energy company run from their front room, some fixed DDs were operated more like Ponzi schemes. The DDs were quietly adjusted upwards so that you were always in credit, often by a significant amount (dotted blue line).When around 30 companies went bust, all the lost credit balances that had to be refunded totalled £2.6 billion, an amount that had to be reclaimed from all customers having to pay an extra £94 for Ofgem's incompetence... plus another £1.7 billion for Bulb !

However, when dozy Ofgem let almost anyone set up an energy company run from their front room, some fixed DDs were operated more like Ponzi schemes. The DDs were quietly adjusted upwards so that you were always in credit, often by a significant amount (dotted blue line).When around 30 companies went bust, all the lost credit balances that had to be refunded totalled £2.6 billion, an amount that had to be reclaimed from all customers having to pay an extra £94 for Ofgem's incompetence... plus another £1.7 billion for Bulb !

Source: Citizens Advice1 -

Good point Gerry1.

It's really more that "the individual customer doesn't lose all of their balance, and isn't any more worse off than any other customer" - a socialised protection - not so much "the customer doesn't lose anything".

Although moving from your red to blue curves was also, in part, a suggestion from the regulator - to address people who were worried that they had a debt (and to avoid issues of people who switched supplier at the bottom of the curve getting a big final bill).1 -

If only it were that low https://www.reuters.com/world/uk/uk-government-expects-recoup-bulb-energy-bailout-cost-2022-12-12/Gerry1 said:Dolor said:

The present DD scheme isn’t perfect but it works for millions of consumers. Given that credit balances are 100% protected, the consumer will not lose out should a supplier fail.deano2099 said:They do indeed. And it's pretty fascinating that Tesco do a far better job with their Christmas saver scheme than energy companies do.

The money is held in a trust separate from Tesco itself, and you can get it back at any time until October (just before the "bonus" is paid in) as a pre-paid cash card.

https://www.tesco.com/help/sections/10865630418841-Clubcard-Christmas-Savers

Like you, I'd be all for energy companies adopting this model!When around 30 companies went bust, all the lost credit balances that had to be refunded totalled £2.6 billion, an amount that had to be reclaimed from all customers having to pay an extra £94 for Ofgem's incompetence... plus another £1.7 billion for Bulb !

Source: Citizens Advice1

![[Deleted User]](https://us-noi.v-cdn.net/6031891/uploads/defaultavatar/nFA7H6UNOO0N5.jpg)

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.3K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards