We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

1y ISA fix now or wait for next BOE raise?

pecunianonolet

Posts: 2,027 Forumite

Hi all,

Debating with myself if I should keep 20k in easy access for now, currently spread over various accounts (Al Ryan 2.81%, YBS 3% level from 9th Dec (maxed out), HSBC 3% (maxed out), Santander 2.75%) or move to a 1y or 1.5y fixed ISA. Need access to the cash in Summer/Autumn 2024. Will break the higher rate threshold with my end of March salary, potentially earlier with anticipated salary increase/bonus and would start to pay tax on savings. Currently putting between 1 and 1.5k aside monthly and have a 15k stoozing pot going too. Was thinking of 1y fix bond as well with higher rate but that would instantly put me into a tax liability situation.

Would you keep everything flexible for now or start fixing? Not much movement since last BOE increase and anticipating another interest rate increase but unsure if it will filter through into fixes and ISA's or if it just means banks take a higher cut but market remains at current level.

What would you do or have you done?

Debating with myself if I should keep 20k in easy access for now, currently spread over various accounts (Al Ryan 2.81%, YBS 3% level from 9th Dec (maxed out), HSBC 3% (maxed out), Santander 2.75%) or move to a 1y or 1.5y fixed ISA. Need access to the cash in Summer/Autumn 2024. Will break the higher rate threshold with my end of March salary, potentially earlier with anticipated salary increase/bonus and would start to pay tax on savings. Currently putting between 1 and 1.5k aside monthly and have a 15k stoozing pot going too. Was thinking of 1y fix bond as well with higher rate but that would instantly put me into a tax liability situation.

Would you keep everything flexible for now or start fixing? Not much movement since last BOE increase and anticipating another interest rate increase but unsure if it will filter through into fixes and ISA's or if it just means banks take a higher cut but market remains at current level.

What would you do or have you done?

0

Comments

-

-

@Albermarle thanks and very interesting read.

However, let me make it a bit more clear.

I can put 20k in an ISA now and fix for 1 year and get 3.8% and I am protected from tax. That would be ca. 760 interest tax free.

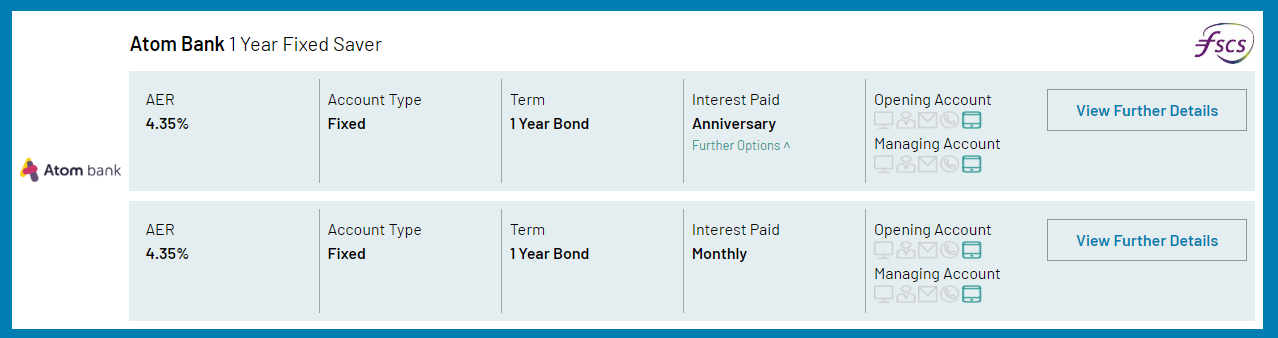

Could also put the 20k into Atom 1 year fixed for 4.35% (4.27% gross) and generate ca. 870 in interest over 12 months. Would need to go monthly interest so I can bank Dec, Jan, Feb and March into this tax year and would be sitting at around 580 interest from Atom alone next year and a tax liability.

This does not take into account additional savings accumulated over time and that I am building up a slow stoozing pot through a purchase card just now needing repayment or a future balance transfer in June next year (max 5k) and another 15k fast stoozing pot partly repayable in 15 months and 20 months.

I have plenty room left for this tax years PSA so the question really is:

- Keep all in easy access for now and gamble for a higher ISA 1y fix of at least 4% to come in December.

- Fix 20k now to current levels for a 1y bond and pay tax on interest next year and keep some cash in easy access to accumulate with future monthly savings to potentially repay full stooze if I can't balance transfer again.

Decisions, decisions.....0 -

0

-

Yes, but again more focussing on long term bonds and not so much on ISA, still a good read.Albermarle said:

On another note, we track rates, have our top 10 tables etc. and I read all the time about trends or things "seem" to go into one or the other direction. Would be great to have a visual representation of this with a trend line. E.g. daily the top easy access interest rate is written down and over time a comprehensive data set is available. Moneyfacts is great to compare on a daily basis wat the currently best rate is but if I want to know historical data I have no chance. Like in the threads you mention there is chat about long term fixes declining. is that really so and is this a confirmed trend or are they more moving sideways, etc.

Don't think something like that exists?0 -

The MSE weekly tips email always contains the best savings rates available on the release date (limited to certain account types). A complete archive is available, so you can tabulate them on a weekly basis going back years if you so desire. It can be a useful exercise.pecunianonolet said:On another note, we track rates, have our top 10 tables etc. and I read all the time about trends or things "seem" to go into one or the other direction. Would be great to have a visual representation of this with a trend line. E.g. daily the top easy access interest rate is written down and over time a comprehensive data set is available. Moneyfacts is great to compare on a daily basis wat the currently best rate is but if I want to know historical data I have no chance. Like in the threads you mention there is chat about long term fixes declining. is that really so and is this a confirmed trend or are they more moving sideways, etc.

Don't think something like that exists?

0 -

Although still probable due to the current 11.1% CPI inflation rate, it is not an absolute certainty that there will be a Bank of England base rate rise on December 15; furthermore, if there is any base rate rise coming from the February Monetary Policy Committee meeting it is likely to be 0.25% at most, followed by few if any further base rate rises from later MPC meetings. I would be very surprised tbh if the peak level of the base rate is much higher than 4% during the next few months seeing as the current prediction is for inflation to start falling back from spring 2023 onwards.

The general consensus at the moment seems to be that the base rate rise on December 15 will most probably be a 0.5% one, with a slightly lesser possibility of only a 0.25% rise. There is actually one MPC member who is very likely to vote to maintain the base rate at 3% on December 15, and it only needs four more MPC members to agree that interest rates are now high enough to bring inflation back down to its target level of 2% for the base rate to be held rather than raised at all!

What will be interesting to see is what happens once a majority on the MPC do decide to hold the base rate at what they see as the highest appropriate level for the time being. Will the base rate be held for several months, thus providing at least a modicum of certainty and stability, or will it start to be regularly lowered after a couple of months or so as part of a general easing of monetary policy due to the fact we’re already in a recession?0 -

I am very certain it will rise again in December, the real question is by how many bpt. The rate lags behind as the BoE has been reacting far too slow, although faster than the ECB and only the Fed saw the sign to raise early but arguably also not early enough. However, for now inflation has gone down in the US, if this is only a snapshot or the beginning of a trend remains to be seen. Fed and ECB movements highly influence BoE decissions as well.

Gilt interest rates came down again, while inflation is high and even rose further. The spread between these two rates is great for the gov as it brings debt down. For us savers it's a painful process of damage control managing meticusly where we put our cash.

So the BoE could and I think should be more aggressive with their rate increases but that would imply huge counter effects on the labour market and with higher unemployment rates even greater effects to the property market with very high mortgate rates as a concequence. The cynic in me would say, a normalisation of property prices to a healthy and justifiable level, as they have been inflated like an ever growing balloon. A side effect is that unproductive and inefficient martet player disapear, too.

On the other hand such a drastic procedure is poison for the already millions suffering living from hand to mouth not knowing how to pay for essentials. The gov would need to step in with drastic fiscal policy (not fundable) to support or the current gov in power risk a record breaking defeat at the next election and possibly loss of power for decades. Landlisde defeat is surely not top of current gov agenda.

So if the BoE is serious about reaching their 2% inflation target they need to act more boldly until we enter a trend by when they can start to keep rates flat.

If the rate only goes 0.5 bpt up in December and 0.25bpt in Feb this is to me a sign that they are not bold enough, even scared of even more political instability, weak currency and having to step in with more quantitave easing in the worst case. Ultimately, that would mean that the BoE is accepting, and would never openly admit, that the 2% goal is not desirable in these times and it is better, longer term, to let people deal with a 4-5% stagflation making them just a little less poorer compared to now with 10-11% inflation rates. In return market players can deal somehow with the situation, there is a semi working gov in place, trust into the UK remains more or less in place and the labour market is not too damaged as we have a labour shortage anyway.

Fast forward 6 months, we survived the winter, maybe the war has even ended, labour market naturally picked up simply because it's summer again. Litterally everyone has been on strike, got some sort of increase and we have adapted to stagflation and hopefully made use of the summer months to prepare for, oh surprise, the next winter.

The verdict, further significant interest rates increases would be a sign for me that the BoE is trully fully independent and leads the way and everyone else has to adapt. Anything else leaves room for doubt, don't hurt me so I don't hurt you scenario.

Interesting read here: https://webcache.googleusercontent.com/search?q=cache:SbNPMlYD2ncJ:https://www.bloomberg.com/news/articles/2022-11-09/boe-s-forecasts-under-fire-from-five-former-uk-rate-setters&cd=19&hl=en&ct=clnk&gl=uk2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards