We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Bond Volatility

Comments

-

I would love to have caught the recent 25% increase in the UK gilts index fund I am eying up but not yet committed any money to buying, would have been a great start to a long term bond fund investmentdunstonh said:but i know that many wont touch bonds with a barge pole!Which is daft now as they have gone back to 1990s levels and are looking much more attractive.0 -

That seems a lot ! I was thinking rises around 10% were more typical.GazzaBloom said:

I would love to have caught the recent 25% increase in the UK gilts index fund I am eying up but not yet committed any money to buying, would have been a great start to a long term bond fund investmentdunstonh said:but i know that many wont touch bonds with a barge pole!Which is daft now as they have gone back to 1990s levels and are looking much more attractive.0 -

See below, Over 5 Year Index Linked Gilt Index Tracker up 24.66%, Corporate Bond Index Tracker, up 21.31%, in last month:Albermarle said:

That seems a lot ! I was thinking rises around 10% were more typical.GazzaBloom said:

I would love to have caught the recent 25% increase in the UK gilts index fund I am eying up but not yet committed any money to buying, would have been a great start to a long term bond fund investmentdunstonh said:but i know that many wont touch bonds with a barge pole!Which is daft now as they have gone back to 1990s levels and are looking much more attractive.

0 -

From Santander managed funds -eskbanker said:

Changing them from what, and with what objectives in mind?Redlander said:Thanks for those replies. Should the current situation affect the proportion of bonds I have in my portfolio? Specifically I 'v been thinking of changing a lot of my investments to Vanguard Life Strategy 60 (i.e. 60% equities, 40% bonds). Ought I to re-think that?

Santander Max 50% Shares Pfl SA

Santander Max 70% Shares Pfl SA

Santander Atlas Portfolio 4 IA

With the aim of preserving my investements against inflation as much as possible over, say, five years.0 -

and is it possible to predict how quickly the value of bonds might recover?A bond is a contract to pay you, who bought it, £100 on an agreed date as well as agreed interest payments regularly until that date. As interest rates have risen recently, such a bond is less attractive (because of its agreed lower interest rate payments) than a new bond paying the current higher interest rate payments. Thus the value of your £100 bond falls until the interest payments become the same percentage of its price as the new bond’s interest payments are.

So now, your £100 bond is only worth, say, £90; but the contract says you must be repaid £100 when it matures. Now you tell me, will the value of the bond recover? Of course it will, it has to as it’s in the contract. So when someone says bond values probably won’t recover, you better ask them what they mean. Not only will the value recover, but we know the precise trajectory of that recovery back to £100 over the remaining life of the bond.

Funds of bonds are a bit more complicated, but their value recovers too; it must if the fund holds the bonds to maturity, although funds commonly don’t but it’s only because they think they can make more money by not doing so. And if you keep reinvesting the interest from the bond fund back into the fund you will speed up the recovery in value. As a rule of thumb: it takes, in years, the duration of the fund (find it in the fund specs) multiplied by the % rise in interest rates for the value of the fund to recover a rise in interest rates so that you’re getting the return you would have had without the rate rise. It takes less time to get back to the value the fund was at when the drop started. So a fund with 10 year duration will take 20 years to get up to the value it would have been without the rate rise, from a 2% interest rate rise. And each interest rate rise resets the clock. Lesson: if you’re investing for a short period with bonds, be very careful of owning bond funds with a long duration.

Second rule of thumb: if interest rates rise continuously, non-stop, it takes 2.5 durations to get ahead of where you would have been without the interest rate rises. But interest rates don’t rise forever, so this rule has limited practical value but it gives you a sense of the time scales.

If you’re a bond investor you’d like interest rates to be as high as possible (and then falling gently) because that’s how you make your money with bonds if you’re in it for the long term.

0 -

Don't many people hold bonds for the negative correlation with stocks to counter stock volatility?

You can find correlation measures. Over the last 50 years the correlation of US bonds with the US stock market has been 0.12. That’s positive, not negative. It’s not very positive, since 1 is the most and -1 is the least correlation. So it’s close to zero, meaning stocks and bonds have moved without regard for each other, independently in fact.

Correlation figures can be highly sensitive to start/end dates, and will be different over shorter and longer periods. Be careful of relying on correlation to do anything for you, or against you.

0 -

Any asset that is less volatile than stocks, as bonds have been, will reduce the volatility of a stock portfolio even if they were perfectly correlated, and more so if they are less correlated I would think.0

-

Judging by your posts on your church friend advisor, should I go active and Morningstar, I’d say you’re engaged enough to accept doing a bit of reading to become an informed participant in the management of your investments. It doesn’t need much brain power, just enough interest. Bogle’s book is good, and free; Hale’s very good and likely in a library near you. Edwards’ book is well spoken of. Asking for portfolio advice without doing that reading only risks you being tossed around by the most convincing posts on different websites, and even if you land on something sensible you risk floundering into up-ending it all again at the next interest rate/covid/brexit induced market crisis.

With the aim of preserving my investements against inflation as much as possible over, say, five years.Do you have a particular purpose for this £400k you are referring to here, for use in about 5 years? We don’t need to know the purpose, just that you need it to be cash? So really specific advice might be possible.

0 -

Err what if you had bought your bond for more than £100 which would probably be the case if you had bought one in the past 13 if not 40 years? The person you bought the bond from would have made excess profit paid for by your loss.JohnWinder said:and is it possible to predict how quickly the value of bonds might recover?A bond is a contract to pay you, who bought it, £100 on an agreed date as well as agreed interest payments regularly until that date. As interest rates have risen recently, such a bond is less attractive (because of its agreed lower interest rate payments) than a new bond paying the current higher interest rate payments. Thus the value of your £100 bond falls until the interest payments become the same percentage of its price as the new bond’s interest payments are.So now, your £100 bond is only worth, say, £90; but the contract says you must be repaid £100 when it matures. Now you tell me, will the value of the bond recover? Of course it will, it has to as it’s in the contract. So when someone says bond values probably won’t recover, you better ask them what they mean. Not only will the value recover, but we know the precise trajectory of that recovery back to £100 over the remaining life …….

0 -

For anyone that doesn't hold bonds yet, but is thinking about buying some bonds funds, would you suggest it may be prudent to wait for the interest rates pivot by governments once inflation gets under control before buying in? Further interest rate hikes are going be more pain for the existing bonds held in funds aren't they?coastline said:Just weeks ago you could have bought VGOV for around £15.50 now £18.60 so 20% up. Volatility will be here for a long time I would have thought as yields are still historically low. In recent years 10% or more volatility has been normal. Moves in base rates can get shallow eg, 0.1% but 0.25% will be pretty common. On 3% that's a fair move and a bit different from 10% to 9% years ago. Set these both to10 years to see the yearly moves .

Vanguard U.K. Gilt UCITS ETF summary price and performance data – Investors Chronicle

United Kingdom Government Bond 10Y - 2022 Data - 1980-2021 Historical - 2023 Forecast (tradingeconomics.com)

Low returns in the 1960's a similar period to today with low base rates.

FgL02RvXoAEgCUh (779×502) (twimg.com)

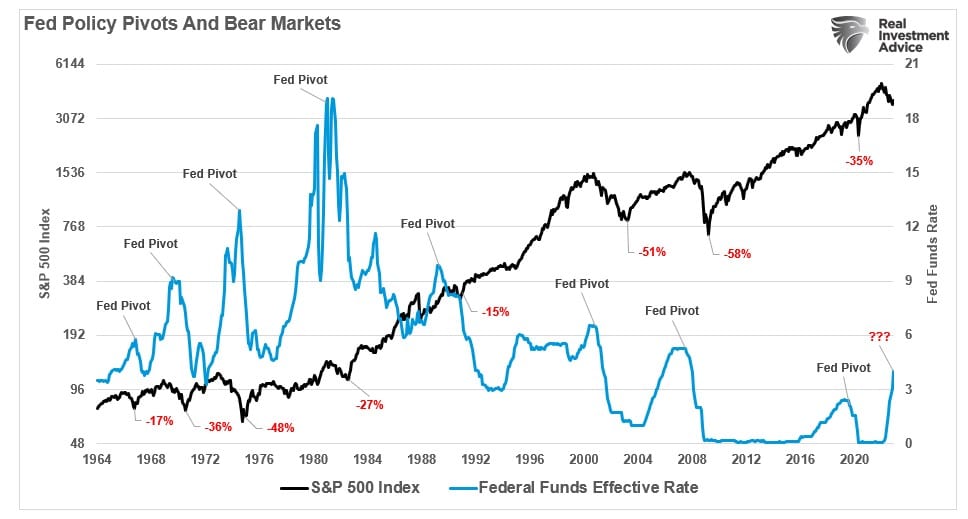

When the FED pivots it usually means there's trouble ahead. Speculators are guessing this will come when unemployment figures go higher. What does that mean? Who knows but if it's a recession then you'd imagine markets will fall. Bonds markets will have repositioned by then and I'd guess prices will be higher so in the case of VGOV could be over £20.?

Fhm-y4rX0AAG8et (900×506) (twimg.com)

Fed-Funds-and-Bear-Markets.jpg (968×519) (realinvestmentadvice.com)0

{kind=link}

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.5K Banking & Borrowing

- 254.1K Reduce Debt & Boost Income

- 455K Spending & Discounts

- 246.6K Work, Benefits & Business

- 602.9K Mortgages, Homes & Bills

- 178K Life & Family

- 260.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards