We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Vanguard LifeStrategy Funds

Comments

-

I wonder if advisers are still advocating 60/40 as the ideal in retirement?No adviser advocates 60/40 as the ideal in retirement. Advice is personalised. However, there probably hasn't been a better time in the last 20 years to invest new money into a fund of that type.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

The recent bond events were an unprecedented one-off unwinding of the unprecedented interest rate fall in the 2008 crash in a few months. So a repeat on the same scale is not likely. If rates again fall to near zero hopefully people will now understand the possible consequences.NannaH said:Well my VLS 80 has lost less in percentage terms than DH’s VR 2025 , which is around 50/50 equity v bonds. Thankfully he only has 15% of his sipp in this.I’m sticking with higher equities at the moment.I wonder if advisers are still advocating 60/40 as the ideal in retirement?

Sadly there are limited alternatives to bonds as a source of non-equity and now interest rates have risen theren use alongside equity I think is still appropriate. Equities are capable of larger falls.0 -

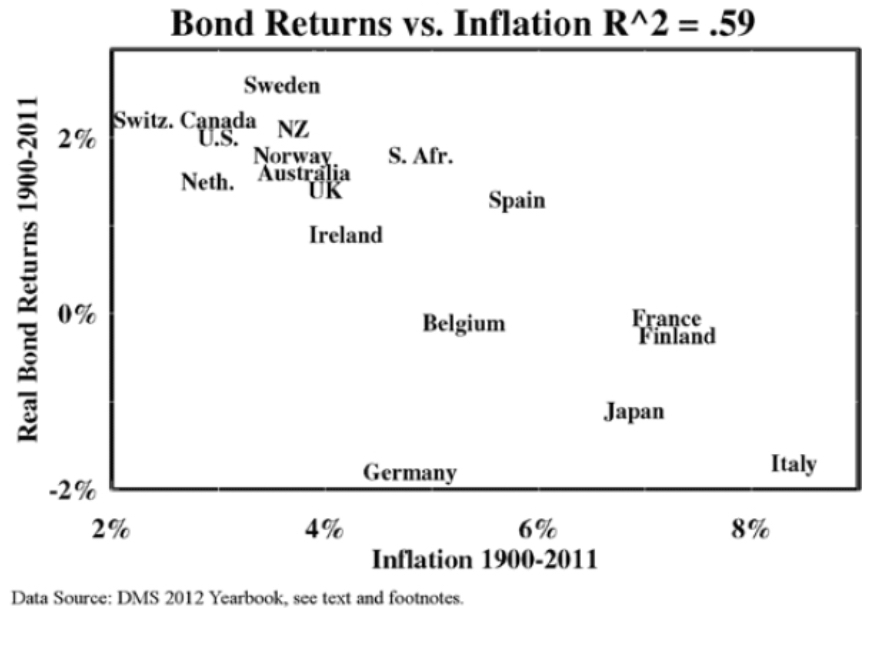

A little bit more history and quantitative info is provided below. One can see strong negative correlation between bond returns and inflation. As expected. In the 20th century we’ve had several decades when bonds permanently destroyed value in the US and Britain as a result of inflation; in several countries negative returns were observed over the whole period.JohnWinder said:Thanks. The more history, and quantitative, we have the better informed we can be. I didn’t choose my period to make a point; it was the longest period offered by portfoliovisualzer for those asset classes, and they were US bonds not UK bonds. Any better sites with useful information, please step forward.

Which is why routine claims that bonds are “low risk” are misleading. They are only “low risk” if your time horizon is short because of lower volatility. Otherwise stocks are lower risk. That’s not to say that bonds shouldn’t be part of the portfolio (I have them) but 40/60 is rarely optimal. 0

0 -

No adviser advocates 60/40 as the ideal in retirement. Advice is personalised. However, there probably hasn't been a better time in the last 20 years to invest new money into a fund of that type.

What is the ideal mix in retirement. I know it all depends on circumstances, but are there any funds out there that'll just keep ticking along and keeping your investments head above the water?

0 -

Sadly, no. I define “above water” as “beating inflation”. Nothing will keep”ticking along”. Shares are volatile. Treasuries and gilds are still paying negative interest (in real terms). There is no guarantee or silver bullet.Skinnydad said:No adviser advocates 60/40 as the ideal in retirement. Advice is personalised. However, there probably hasn't been a better time in the last 20 years to invest new money into a fund of that type.

What is the ideal mix in retirement. I know it all depends on circumstances, but are there any funds out there that'll just keep ticking along and keeping your investments head above the water?One has to look at annuities to get any degree of certainty. Its a good idea fora portion of your portfolio unless you have DB pensions. Outside that, Graham’s 60/40 balanced portfolio has stood the test of time amazingly well (VLS 60 is an example).Basic principles are:

- stay invested and diversified

- reduce expenditure during major bears

- keep your investment costs and “layers” between you and your money under control

- stay liquid (avoid property and private equity funds)

- invest in things with positive expected return (avoid gold, etc)

- all will be well.2 -

Nice historical overview in the graphic, and ‘bankable’ principles. Just to note that for most of that 110 year period and in most of those countries inflation linked bonds were not offered. Nominal bonds can be damaged by unexpected inflation which I suppose high inflation usually is, but linkers can’t be.

Secondly, the real yields on linkers maturing in under 35 years are all positive, not negative as of Tuesday, according to the Bank of England. That’s an asset that will tick along and ‘beat inflation’ and carries a high quality guarantee. That allows you to call bonds ‘low risk’ I think, and it introduces the concept a ‘funding ratio’, below.

I don’t think an ‘appeal to authority’ is a good basis for advice, but if we’re talking about Benjamin Graham I think his advice was to hold between 25% and 75% as stocks, ‘“The sound reason for increasing the percentage in common stocks [beyond 50%] would be the appearance of ‘bargain price’ levels created in a protracted bear market. Conversely, sound procedure would call for reducing the common-stock component below 50% when in the judgment of the investor the market level has become dangerously high.”.

We know it’s hard to agree on what ‘risk’ is. If it’s volatility, then high quality bonds have been and will likely remain lower risk than stocks. But if risk is having or not having the spending money you need at the time you need it, then an all stock portfolio can be more risky if it collapses the day you retire, while a bond portfolio can be more risky if it doesn’t increase in value enough to cover your spending needs. The ‘funding ratio’ is an alternative, ‘better’ way to assess the risk of a portfolio made for retirement, because it doesn’t focus on volatility which is irrelevant if you give proper consideration to what really matters which is ‘will enough money be there, when I need it in retirement?’.

The funding ratio is how much the portfolio is worth divided by how much it needs to be. If it’s worth £400k, but needs to be £600k, the ratio is 0.67 and so needs to be lifted to 1.0 by more contributions or better returns. When you get to a ratio of 1.0 you need have no risk anymore. The bit you won’t like about this idea is that when you get to 1.0, you have to spend that money on buying a lifetime indexed annuity or a bond ladder of linkers; essentially, certain (or as certain as you can get) sources of lifetime inflation protected income. Those latter are investments with no volatility, or at least none that matters. Even if linkers yields are negative, you can do this as the yield simply needs to be factored into the funding ratio.

1 -

Secondly, the real yields on linkers maturing in under 35 years are all positive, not negative as of Tuesday, according to the Bank of England.

Are you certain about this? I am seeing yields on 30-year gilts at around 4.5%. Linkers will yield less. UK CPI sits at about 9%. Real yields appear to be negative.

0 -

No, I could be wrong. Have a look at https://www.bankofengland.co.uk/statistics/yield-curves

UK instantaneous implied real forward curve (gilts) chart.

These are ‘forward’ yields which I think can (usually) be different (a lot or a little) from what we want to know. So, I don’t know which linkers have positive yields now, if any. Seeking light.0 -

https://www.londonstockexchange.com/stock/TR40/united-kingdom/company-page

Does this information mean I could have bought a linker maturing in 2040 for £86 this week, and receive a coupon of 0.625%/year, and expect to get £100 back in 2040? The £100 back assumes no inflation from now on; if there is any then I get more than £100. Indeed its inflation adjusted face value is probably well over £100 already, which I get back with no further inflation. And the 0.625% is on its current inflation adjusted value, not on £100. Have I go that right? If so, the yield seems positive.0 -

Thanks, I understand. Maybe a bad choice of words ticking over. From a personal perspective I'm 64..2 years away from state pension age. My sipp has taken a pounding. No doubt like a lot of others. If I could get it back to where it was then I'd sit in cash. To hell with inflation and erosion. Because it's couldn't be worse than the markets at present. Plus TBH you're getting a better return in some bonds at present. And no doubt as we go forward in some interest baring accounts. Just my tuppence worth. Sorry for the rantDeleted_User said:

Sadly, no. I define “above water” as “beating inflation”. Nothing will keep”ticking along”. Shares are volatile. Treasuries and gilds are still paying negative interest (in real terms). There is no guarantee or silver bullet.Skinnydad said:No adviser advocates 60/40 as the ideal in retirement. Advice is personalised. However, there probably hasn't been a better time in the last 20 years to invest new money into a fund of that type.

What is the ideal mix in retirement. I know it all depends on circumstances, but are there any funds out there that'll just keep ticking along and keeping your investments head above the water?One has to look at annuities to get any degree of certainty. Its a good idea fora portion of your portfolio unless you have DB pensions. Outside that, Graham’s 60/40 balanced portfolio has stood the test of time amazingly well (VLS 60 is an example).Basic principles are:

- stay invested and diversified

- reduce expenditure during major bears

- keep your investment costs and “layers” between you and your money under control

- stay liquid (avoid property and private equity funds)

- invest in things with positive expected return (avoid gold, etc)

- all will be well.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards