We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Vanguard LifeStrategy Funds

Comments

-

Ask again in 6 months time, because without a crystal ball nobody knows.jim8888 said:Given the situation in the bond market at the moment, is investing into a Vanguard 60% Equity, 40% Bond fund more risky, or less risky, than a 60% Bond, 40% equity fund?0 -

Exactly. Makes you wonder why they're allowed to market them as one type being less risky than another? I suppose admitting "We have not the first clue how any of our funds will perform in the near or long term future" is covered with the catch-all "Value of funds can go up and down" that they all employ.Albermarle said:

Ask again in 6 months time, because without a crystal ball nobody knows.jim8888 said:Given the situation in the bond market at the moment, is investing into a Vanguard 60% Equity, 40% Bond fund more risky, or less risky, than a 60% Bond, 40% equity fund?0 -

Is Vanguard 60/40 worth investing in at all. All the markets have taking a hammering, first it was Covid, then the SMO in Ukraine and now the debacle of the current government..0

-

Makes you wonder why they're allowed to market them as one type being less risky than another?You could check how they define risk, but commonly it’s how much variation there is in the gains and losses of the funds or assets in the funds over long periods of time. We know that those bonds vary less than those equities from history, and painful experience. And ignore 6 months of what’s happened if you’re assessing risk. If one fund changed value more than the other over a two day period would you conclude it to be more risky for your purposes? No, because one doesn’t invest in such a fund for 2 days.

0 -

The important question is “what is risky to you”? What is your investment horizon?

The expected growth for 40/60 is less than for 60/40, so the former is more risky for people with many years of investing before them, unless they already have too much money. Bonds can lose value for years on end, something stock indices rarely do.Stocks are more volatile though so if you need to start withdrawing soon then sequence of returns is an issue and you may want more bonds. Keep in mind that VLS uses a mix of British and foreign bonds, so British government alone can’t destroy the bond portion of the portfolio.1 -

In general its better to invest just after the markets take a hammering rather than just before.Skinnydad said:Is Vanguard 60/40 worth investing in at all. All the markets have taking a hammering, first it was Covid, then the SMO in Ukraine and now the debacle of the current government..3 -

Bonds can lose value for years on end, something stock indices rarely do.

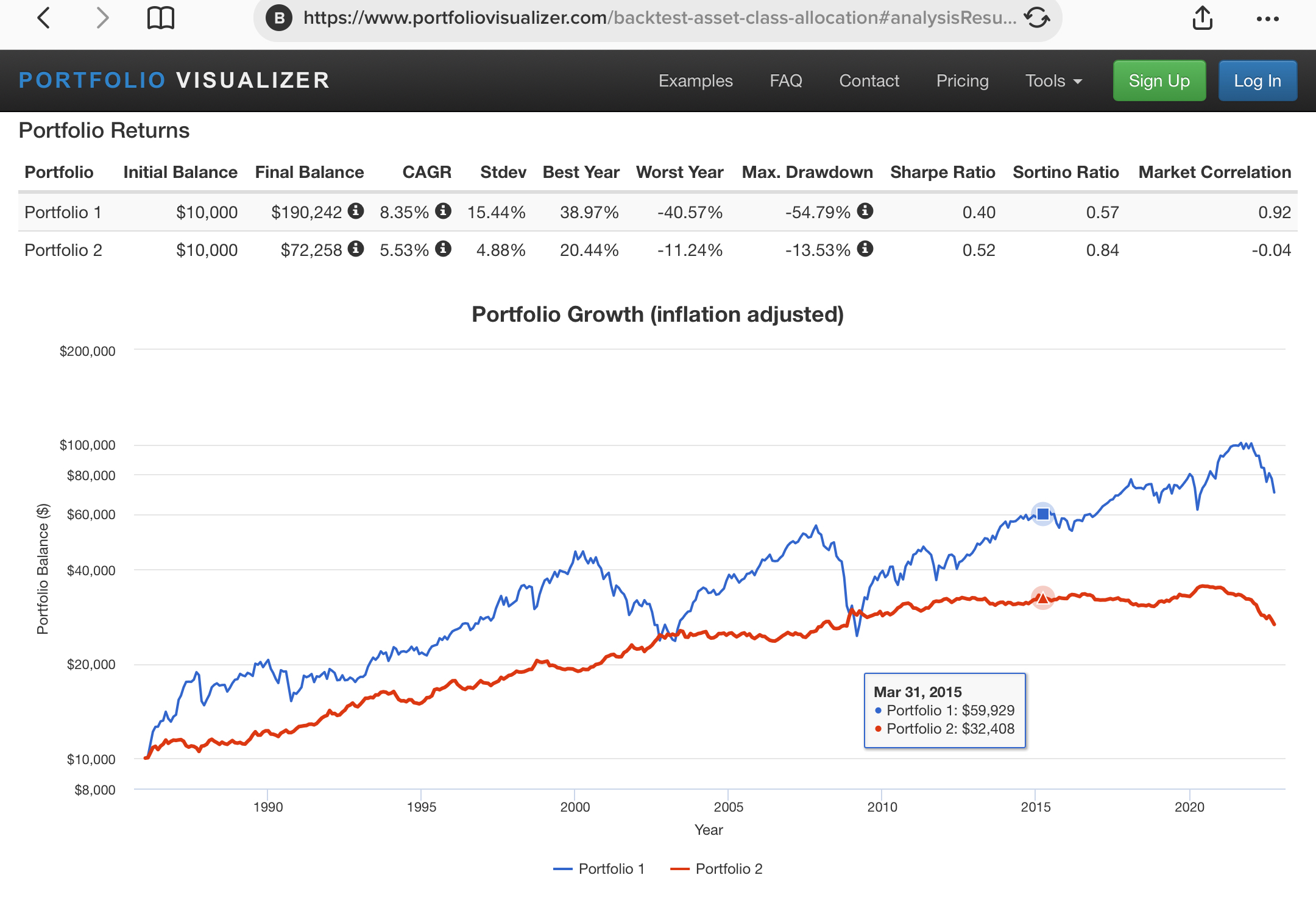

It may be hard for some readers, including me, to get a clear picture of what that means since ‘can lose value’ says nothing about how often or for how many years whereas ‘rarely do’ says how often. What to do? Compare the inflation adjusted value of global stocks with intermediate government bonds over a 35 year period:

0

0 -

We can’t look at the period of secular fall in interest rates (since around 1980) and claim that its in any way representative of all conditions. Bond holders suffered disastrous returns for most of the 20th century.JohnWinder said:Bonds can lose value for years on end, something stock indices rarely do.It may be hard for some readers, including me, to get a clear picture of what that means since ‘can lose value’ says nothing about how often or for how many years whereas ‘rarely do’ says how often. What to do? Compare the inflation adjusted value of global stocks with intermediate government bonds over a 35 year period:

In the words of Bernstein (Four Pillars):

” What you are looking at is a picture of the financial devastation of British bondholders. Between 1900 and 1974, the average consol yield rose from 2.54% to 14.95%, or a fall in price of 83%. But there was even worse news. Between those two dates, inflation had decreased the value of the pound by approximately 87%, so the real principal value of the consol had fallen 98% during the period, although that loss was partially mitigated by the dividends paid out. The twentieth century history of bonds in the U.S. was almost as unhappy.“

I am not saying the twentieth century is going to be repeated but bond holders had negative returns in real terms over whole decades (and longer). Its a high risk asset if you have a long investment career in front of you and plonk most of your portfolio into bonds. Unexpected inflation is particularly bad for bonds. Its also bad for stocks, but they recover much faster.1 -

Thanks. The more history, and quantitative, we have the better informed we can be. I didn’t choose my period to make a point; it was the longest period offered by portfoliovisualzer for those asset classes, and they were US bonds not UK bonds. Any better sites with useful information, please step forward.0

-

Well my VLS 80 has lost less in percentage terms than DH’s VR 2025 , which is around 50/50 equity v bonds. Thankfully he only has 15% of his sipp in this.I’m sticking with higher equities at the moment.I wonder if advisers are still advocating 60/40 as the ideal in retirement?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.3K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.3K Work, Benefits & Business

- 604K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.5K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards