We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Holding cash in a personal pension

Comments

-

Alistair31 said:

For the life of me, I still cannot figure out how to do this (iweb)masonic said:pdiddy64 said:Are you aware that it is very difficult to invest in individual bonds within low cost SIPPS? Account holders are shepherded into buying bond funds. If you look through all of the investment literature all it talks about is bond funds. I don't think I have ever read an article about an individual company bond. The same applies to gilts. The point is identical to the issue with cash. Individual investors in low cost SIPPs cannot access the good deals. This will change with time as investors become more astute and providers are forced to offer individual bonds - almost the opposite of what happened with mutual equity funds many years ago. Please can we leave bonds totally out of this as it just distracts from the point about cash held in SIPPs.There are low cost SIPP providers who allow you to buy individual bonds, for example Hargreaves Lansdown and iWeb. As you mention later in your post that you hold a SIPP at iWeb, you can already access bonds paying a return of 4+%, so problem solved..If you go to the trading page for shares and enter the ticker for the gilt you're interested in (e.g. TG26) then it should recognise it. (this is based on my experience with a trading account and S&S ISA at iWeb, as I don't hold a SIPP there) When I last tried, it told me that online trading wasn't available and I'd need to call them. Markets are closed now, but it seemed to be attempting to get a quote just now before throwing an error, so perhaps online trading was just suspended when I last tried.2

When I last tried, it told me that online trading wasn't available and I'd need to call them. Markets are closed now, but it seemed to be attempting to get a quote just now before throwing an error, so perhaps online trading was just suspended when I last tried.2 -

aroominyork said:

Where does the data come from please? Morningstar shows YTM of IGLT as 2% https://www.morningstar.co.uk/uk/etf/snapshot/snapshot.aspx?id=0P00007013&tab=3&InvestmentType=FEm_c_s said:IGLT iShares Core UK Gilts UCITS ETF 10yr avg bond ytm=4.29% IGLS iShares UK Gilts 0-5yr UCITS ETF very low risk ytm=4.13% ERNS iShares £ Ultrashort Bond UCITS ETF mainly corporate bonds of less than 1yr duration ytm=3.57%

There will be some volatility in the fund price for the top two ETFs but 4+% return virtually guaranteed is something we have not had for many years.Here you go

1 -

Thank you, Masonic. Using my below example, can you tell me what guaranteed return would be, and would it just appear as cash in account after 22/07/23?masonic said:Alistair31 said:

For the life of me, I still cannot figure out how to do this (iweb)masonic said:pdiddy64 said:Are you aware that it is very difficult to invest in individual bonds within low cost SIPPS? Account holders are shepherded into buying bond funds. If you look through all of the investment literature all it talks about is bond funds. I don't think I have ever read an article about an individual company bond. The same applies to gilts. The point is identical to the issue with cash. Individual investors in low cost SIPPs cannot access the good deals. This will change with time as investors become more astute and providers are forced to offer individual bonds - almost the opposite of what happened with mutual equity funds many years ago. Please can we leave bonds totally out of this as it just distracts from the point about cash held in SIPPs.There are low cost SIPP providers who allow you to buy individual bonds, for example Hargreaves Lansdown and iWeb. As you mention later in your post that you hold a SIPP at iWeb, you can already access bonds paying a return of 4+%, so problem solved..If you go to the trading page for shares and enter the ticker for the gilt you're interested in (e.g. TG26) then it should recognise it. (this is based on my experience with a trading account and S&S ISA at iWeb, as I don't hold a SIPP there)When I last tried, it told me that online trading wasn't available and I'd need to call them. Markets are closed now, but it seemed to be attempting to get a quote just now before throwing an error, so perhaps online trading was just suspended when I last tried.

My logic is to earn something on cash (in S&S ISA) that is earmarked to cover mortgage on renewal next October.0 -

If gilts are supposed to give an almost guaranteed rate of return how can an etf like IGLT that only holds gilts performed so badly over the last year0

-

Short term Gilts have a mathematic certainty if held to maturity. So if you buy a gilt today for about £100 it will bring in about 4% pa and you get your £100 back

Or other gilts will cost £96 and yield .125% and after a year you get minimal interest but you get £100 back

In both cases you make around 4%. Depending on the gilt you can essentially select whether the profit is income or capital gain. More interesting if gilt not held in tax shelter.

So you can simply pick a gilt based on when you want it to mature.

Make sure you don't buy an index linked gilt unless you mean to!

A bond fund never matures so will fluctuate depending on market conditions. So unlike individual gilts contain no certainty so maybe not ideal for cash substitute.

You can't compare holding individual shares and a share fund to holding individual bonds and a bond fund...

Diversification for Gilts which have built in certainly is not relevant and does not reduce risk

2 -

The gilt rate of return is as a % of £100, the nominal value of a bond, and at maturity you get £100 back. So a 4% bond gioves you £4/year. SO it is guaranteed if you hold to maturity.Stargunner said:If gilts are supposed to give an almost guaranteed rate of return how can an etf like IGLT that only holds gilts performed so badly over the last year

The gilt fund calculations are based on the current price of the constituent bonds which can, in the case of long dated bonds, be quite volatile.2 -

Alistair31 said:

Thank you, Masonic. Using my below example, can you tell me what guaranteed return would be, and would it just appear as cash in account after 22/07/23?masonic said:Alistair31 said:

For the life of me, I still cannot figure out how to do this (iweb)masonic said:pdiddy64 said:Are you aware that it is very difficult to invest in individual bonds within low cost SIPPS? Account holders are shepherded into buying bond funds. If you look through all of the investment literature all it talks about is bond funds. I don't think I have ever read an article about an individual company bond. The same applies to gilts. The point is identical to the issue with cash. Individual investors in low cost SIPPs cannot access the good deals. This will change with time as investors become more astute and providers are forced to offer individual bonds - almost the opposite of what happened with mutual equity funds many years ago. Please can we leave bonds totally out of this as it just distracts from the point about cash held in SIPPs.There are low cost SIPP providers who allow you to buy individual bonds, for example Hargreaves Lansdown and iWeb. As you mention later in your post that you hold a SIPP at iWeb, you can already access bonds paying a return of 4+%, so problem solved..If you go to the trading page for shares and enter the ticker for the gilt you're interested in (e.g. TG26) then it should recognise it. (this is based on my experience with a trading account and S&S ISA at iWeb, as I don't hold a SIPP there)When I last tried, it told me that online trading wasn't available and I'd need to call them. Markets are closed now, but it seemed to be attempting to get a quote just now before throwing an error, so perhaps online trading was just suspended when I last tried.

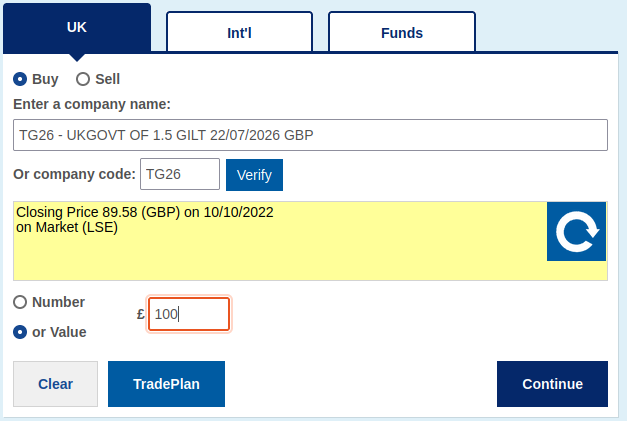

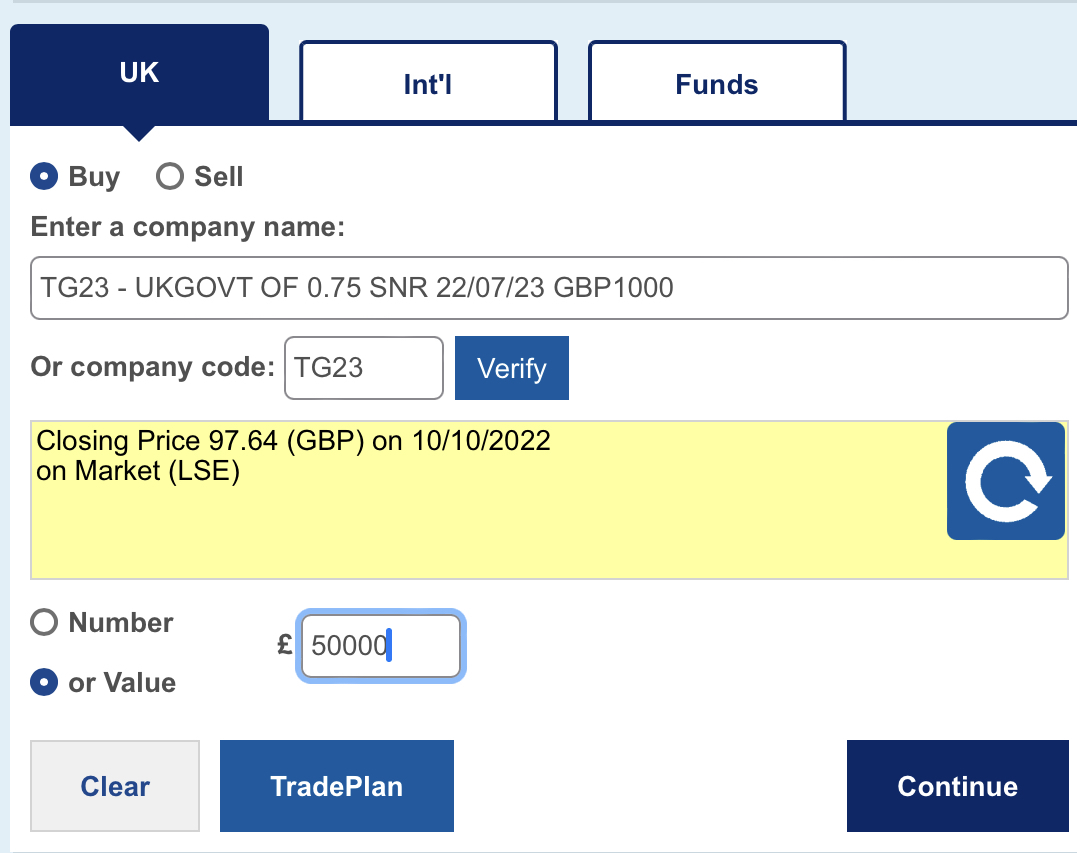

My logic is to earn something on cash (in S&S ISA) that is earmarked to cover mortgage on renewal next October.You'd get interest payments at 0.75% AER based on the face value (in Jan and July), so a total of £50,000/97.64*0.75 = £384 minus accrued interest between July 2022 and when you buy (I guess about -£90), which is added to your acquisition price.At maturity you'd get the principal repaid at £100 face value, so £50,000/97.64*100 = £51,208.1 -

Neversurrender said:I have approx £50,000 in cash in my Sipp portfolio.

My intention is to take £16,666 out each financial year for the coming 3 years starting April 2023

It hurts me that the interest offered is pitiful

I am holding it in cash as I will be needing it over the next 3 years and don't want it to go down then crystallise a loss.

So reading this thread would anything similar suffice for my situation?

if you move your SIPP to Hargreaves Landown you can buy gilts maturing in 2023, 2024 and 2025 - interest on these is currently 4%+ less HL's fees.

0 -

Any chance you could give the details of what I have highlighted in bold? I am sure many would be interested to know which pension provider offers a guaranteed 7% return on an investment.pdiddy64 said:Masonic

Most of your arguments are contradictory and obviously made to distract the argument.

Your final point about bonds being a good deal really gives the game away! Most people would agree that bonds are one of the most risky investments of all at the moment (especially those with indexation or long duration).

SIPP providers generate a great deal of profit from ripping clients off with poor returns on cash, that is just a fact. Changing this would remove the distortion in the SIPP industry, not create a distortion elsewhere.

The point about company pension schemes and the wider pension industry doing the same thing has some validity but it is not quite as bad there at all. For example, my workplace pension offers a guaranteed 7% equity based scheme. There are also many other schemes that are actually quite generous. Also, why should the fact that this is an industry wide con prevent us from reining in this poor behaviour in the SIPP area? We have to start somewhere.

Maybe many of us will not stand to gain much from any change - but at least we could be helping those who follow in years to come.

Please tell me if you think I am being naive or just wrong.2 -

Masonic's explicit calculation is very useful, but there is also a yield to maturity calculator at https://dqydj.com/bond-yield-to-maturity-calculator/ (just ignore the $ signs and pretend they are £!) which for your example gives a ytm of just over 3.1% (in agreement with Masonic's calculation).masonic said:Alistair31 said:

Thank you, Masonic. Using my below example, can you tell me what guaranteed return would be, and would it just appear as cash in account after 22/07/23?masonic said:Alistair31 said:

For the life of me, I still cannot figure out how to do this (iweb)masonic said:pdiddy64 said:Are you aware that it is very difficult to invest in individual bonds within low cost SIPPS? Account holders are shepherded into buying bond funds. If you look through all of the investment literature all it talks about is bond funds. I don't think I have ever read an article about an individual company bond. The same applies to gilts. The point is identical to the issue with cash. Individual investors in low cost SIPPs cannot access the good deals. This will change with time as investors become more astute and providers are forced to offer individual bonds - almost the opposite of what happened with mutual equity funds many years ago. Please can we leave bonds totally out of this as it just distracts from the point about cash held in SIPPs.There are low cost SIPP providers who allow you to buy individual bonds, for example Hargreaves Lansdown and iWeb. As you mention later in your post that you hold a SIPP at iWeb, you can already access bonds paying a return of 4+%, so problem solved..If you go to the trading page for shares and enter the ticker for the gilt you're interested in (e.g. TG26) then it should recognise it. (this is based on my experience with a trading account and S&S ISA at iWeb, as I don't hold a SIPP there)When I last tried, it told me that online trading wasn't available and I'd need to call them. Markets are closed now, but it seemed to be attempting to get a quote just now before throwing an error, so perhaps online trading was just suspended when I last tried.

My logic is to earn something on cash (in S&S ISA) that is earmarked to cover mortgage on renewal next October.You'd get interest payments at 0.75% AER based on the face value (in Jan and July), so a total of £50,000/97.64*0.75 = £384 minus accrued interest between July 2022 and when you buy (I guess about -£90), which is added to your acquisition price.At maturity you'd get the principal repaid at £100 face value, so £50,000/97.64*100 = £51,208.

I've checked with iweb support, they will indeed only take orders for individual bonds by telephone and have no intention of offering an online service in this area.

2

Here you go

Here you go

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.5K Banking & Borrowing

- 254.4K Reduce Debt & Boost Income

- 455.4K Spending & Discounts

- 247.4K Work, Benefits & Business

- 604.2K Mortgages, Homes & Bills

- 178.5K Life & Family

- 261.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards