We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

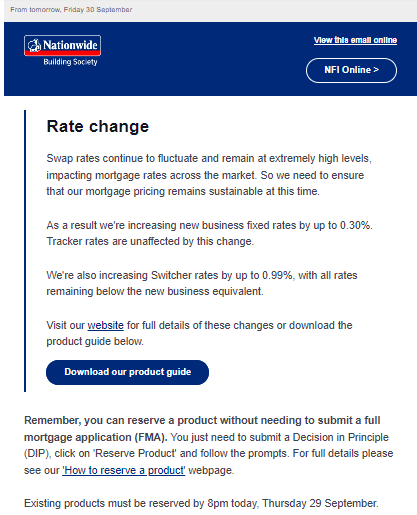

Nationwide announce revised Interest rates

Comments

-

You can't if there is an ERC payable - otherwise yes, a simple mortgage can be switched online (did mine a week ago - saved 4.29% instead of 5.19% today, happy days).themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

Know what you don't0 -

You can apply yourself online for a no advice switch of products (as I have done previously) but you can't do that when there is an early repayment charge, like I said. You have to make an appointment with a mortgage advisor as is mentioned on the screen and lets you go no further. The helpline confirmed that an ERC could not be settled online.themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

0 -

Exactly the same boat as me - stuck in ERC payable range will 31st October and it would cost me £1000 to change before then. I'm going to sit it out till then though as even with a substantial rates rise I probably will be still better off (or only slightly worse off) if I wait and don't pay the £1000.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.I am insane and have 4 mortgages - total mortgage debt £200k. Target to zero = 10 years! (2030)0 -

I think it also states this on the online mortgage manager when you try to switch.Dabrudders said:

You can apply yourself online for a no advice switch of products (as I have done previously) but you can't do that when there is an early repayment charge, like I said. You have to make an appointment with a mortgage advisor as is mentioned on the screen and lets you go no further. The helpline confirmed that an ERC could not be settled online.themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

Are you able to reserve the rate through a DIP or something? I'd be going absolutely crazy if not and you had to wait until October, in which another government master play could see interest rates in the double digits...Know what you don't0 -

Sadly and frustratingly, you can't reserve the rate until the appointment takes place. We tried that ourselves recently when the advisor called us for a quick chat to introduce herself a couple of days before the appointment - I could see from the Nationwide intermediaries website that the rates were due to go up the next day so asked if we could 'pencil in' the current rate in advance of the appointment, but it wasn't possible!Exodi said:

I think it also states this on the online mortgage manager when you try to switch.Dabrudders said:

You can apply yourself online for a no advice switch of products (as I have done previously) but you can't do that when there is an early repayment charge, like I said. You have to make an appointment with a mortgage advisor as is mentioned on the screen and lets you go no further. The helpline confirmed that an ERC could not be settled online.themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

Are you able to reserve the rate through a DIP or something? I'd be going absolutely crazy if not and you had to wait until October, in which another government master play could see interest rates in the double digits...0 -

Unfortunately we just have to wait until 7th or try to line up a 6 month offer from this coming Saturday with another lender. Which has the risk of that being pulled if things get worse which by the look of these clowns on an hourly basis seems baked in.Exodi said:

I think it also states this on the online mortgage manager when you try to switch.Dabrudders said:

You can apply yourself online for a no advice switch of products (as I have done previously) but you can't do that when there is an early repayment charge, like I said. You have to make an appointment with a mortgage advisor as is mentioned on the screen and lets you go no further. The helpline confirmed that an ERC could not be settled online.themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

Are you able to reserve the rate through a DIP or something? I'd be going absolutely crazy if not and you had to wait until October, in which another government master play could see interest rates in the double digits...0 -

catclaires said:

Sadly and frustratingly, you can't reserve the rate until the appointment takes place. We tried that ourselves recently when the advisor called us for a quick chat to introduce herself a couple of days before the appointment - I could see from the Nationwide intermediaries website that the rates were due to go up the next day so asked if we could 'pencil in' the current rate in advance of the appointment, but it wasn't possible!Exodi said:

I think it also states this on the online mortgage manager when you try to switch.Dabrudders said:

You can apply yourself online for a no advice switch of products (as I have done previously) but you can't do that when there is an early repayment charge, like I said. You have to make an appointment with a mortgage advisor as is mentioned on the screen and lets you go no further. The helpline confirmed that an ERC could not be settled online.themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

Are you able to reserve the rate through a DIP or something? I'd be going absolutely crazy if not and you had to wait until October, in which another government master play could see interest rates in the double digits...

My full sympathies to you both - that is absolutely shocking...Dabrudders said:

Unfortunately we just have to wait until 7th or try to line up a 6 month offer from this coming Saturday with another lender. Which has the risk of that being pulled if things get worse which by the look of these clowns on an hourly basis seems baked in.Exodi said:

I think it also states this on the online mortgage manager when you try to switch.Dabrudders said:

You can apply yourself online for a no advice switch of products (as I have done previously) but you can't do that when there is an early repayment charge, like I said. You have to make an appointment with a mortgage advisor as is mentioned on the screen and lets you go no further. The helpline confirmed that an ERC could not be settled online.themoomins said:

You can just apply online yourself, taking a 'no advice' mortgage if you know what you are doing. I did it in 2020 with no problems.Dabrudders said:

I would suggest getting your appointment sorted in advance as there is a wait now due to the rush brought on by this mess.IvyFlood said:

You are the exact same as me! We were looking at the same deal and we must have the same amount left as our ERC is £1400 at 1% - though we need to wait till Saturday for it to fall in the 1% bracket.Adsta said:

I'm in similar boat. My 2.09 fix ends Oct next year (2023) I'm considering if I try switch deal next month, ERC is 1.4k to get a 5 year fix at 4.49%.DPicard said:I got a 2 year fixed term on 2020 thinking that the Covid storm would pass and now im finding myself on a rush to remortgage and potentially paying 2K£ of ERC.

Any advice on what could be the safest thing looking ahead? would it be wise to go for a 5 year deal i.e. will things go back to normal in the mid term or is this the new "normality"

That or ride it out until Oct and hope they don't go up to high. I could manage if they get to extreme of say 8% by next year after this years payments and some overpayments. But it would start getting rough if they do go any higher or no sign of coming down.

4.49% would be a dent but obviously more manageable. But then risk is being locked to that for next 5 years in which they might come down again. I need to sit on it for another couple of weeks anyway for my ERC to fall into the 1.4k territory anyways.

Such awful timing.

My fixed runs out March 31st So ERC payable until 31 October. Decided it was worth it to guarantee a 5 year fixed at todays rate. 45 minutes wait time while calling Nationwide Mortgage helpline and after 20 mins of not much I was told I need to make an appointment with Mortgage Advisor to discuss options. Expected 1 and a half hour appointment with both my wife and myself and earliest appointment was 7 October. I know what I want and I want it today but now just have to hope it doesn't get worse by next week which it no doubt will. Appointment necessary due to ERC element.

Are you able to reserve the rate through a DIP or something? I'd be going absolutely crazy if not and you had to wait until October, in which another government master play could see interest rates in the double digits...Know what you don't0 -

@Dabrudders, if it helps at all, we are changing from Nationwide to Lloyds - we did an unsupported application online, and it was unbelievably easy/quick. Our circumstances are quite straightforward, but even so, it only took about 15 minutes if that to put through the full application, and we received the offer in a couple of days! I'm not sure what the Lloyds rates are like now, but at the time they were slightly better than Nationwide anyway - plus we can wait for longer before we start the new mortgage, which will save a bit of interest and a tiny bit of ERC too (with Nationwide, we had to start the new product pretty much immediately).1

-

Thanks for that. We will take a look this evening.catclaires said:@Dabrudders, if it helps at all, we are changing from Nationwide to Lloyds - we did an unsupported application online, and it was unbelievably easy/quick. Our circumstances are quite straightforward, but even so, it only took about 15 minutes if that to put through the full application, and we received the offer in a couple of days! I'm not sure what the Lloyds rates are like now, but at the time they were slightly better than Nationwide anyway - plus we can wait for longer before we start the new mortgage, which will save a bit of interest and a tiny bit of ERC too (with Nationwide, we had to start the new product pretty much immediately).0 -

Nationwide is upping rates again from tomorrow. This is an intermediary notification, not sure if it's the same direct or not.

Barclays is again increasing rates from tomorrow, Halifax from Monday.

I am a Mortgage Adviser - You should note that this site doesn't check my status as a mortgage adviser, so you need to take my word for it. This signature is here as I follow MSE's Mortgage Adviser Code of Conduct. Any posts on here are for information and discussion purposes only and shouldn't be seen as financial advice.

PLEASE DO NOT SEND PMs asking for one-to-one-advice, or representation.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards