We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

To overpay mortgage or to increase savings?

Comments

-

With regards to property valuation when remortgaging, this might make it clearer

https://hoa.org.uk/services/ask-an-expert-2/ask-an-expert-i-am-managing/how-do-i-value-my-property-before-remortgaging/

1 -

There is no practical difference between a 'workplace' pension and an 'auto-enrolment' pension. The provider is what determines the investment choices.

I don't have a NOW pension so can't log in and see what is there but from what I can see on their website you are invested in their diversified growth fund - no choice in this and as you say can't change, and I agree is very difficult to see what exactly it is invested in (factsheet only gives breakdown of (rather vague) asset classes, no further breakdown), I couldn't find any more details.

https://www.nowpensions.com/app/uploads/2022/05/diversified-growth-fund-factsheet-q1-22.pdf

In members booklet says you can change the age you tell them you want to retire (this will make no difference to when you actually retire). In booklet says you can email them.

https://www.nowpensions.com/app/uploads/2022/04/Member-Booklet-NP-D0065.pdf

One option you could look at if you aren't happy with the investment options is to periodically transfer out from NOW to a different provider (in booklet says is free) - whether your SIPP or a previous workplace pension.

0 -

It leaves me wondering whether we're talking about the same thing to be honest. I'll say where I'm at and you can tell me if we're on the same page:Expotter said:With regards to property valuation when remortgaging, this might make it clearer

https://hoa.org.uk/services/ask-an-expert-2/ask-an-expert-i-am-managing/how-do-i-value-my-property-before-remortgaging/

I bought a house. Took out a mortgage on it at 102k. We fixed for 5 years with Nationwide.

As that 5 years approached, I went to my IFA & said hey we're nearing the end of our 5 years. I want to lock in on another 5 years but don't have a clue what I'm doing, can you assist again (same guy who sorted us with the initial purchase).

Went to his place, he sorted another 5 year fixed, the cheapest being with who the initial 5 year was with - Nationwide, so that side was made easier.

And now we're 12 months from coming to the end of the existing 5 years.

Is that called remortgaging or not? Is it called something else? Again, not being difficult or awkward here. If anything it just shows my lack of understanding.

Because when you talk about remortgaging & when the links talk about remortgaging, pictures are being painted of having to get a valuation done on the house.

When that isn't something we had to do last time.🤐🤐🤐

0 -

Thanks for the detail/snapshots. NOW is the outlier with no choices, as said this is rather unusual, even for a newer provider focused on auto enrolment pensions.B0bbyEwing said:@Albermarle

@Dazed_and_C0nfused

@grumiofoundation

Firstly Albermarle touched on something which may be why you seem to be suggesting I've got it wrong here when I know I haven't - auto enrolment.

Now I don't know what the experience of workplace pensions is you guys have and I'm no expert but I've seen enough to know that they're not all created equal, so I don't assume that mine is a fair representations of the next persons, likewise theirs isn't necessarily going to be the same as the person after them and so on. I personally accept that there's differences between providers.

Now whether this lack of faith in me being correct comes down to you're thinking about a workplace pension that isn't auto-enrolment and maybe auto-enrolment is different, I honestly don't know. I don't knwo whether auto enrolment is or is not different to other workplace pensions.

I'll show you 3 examples:

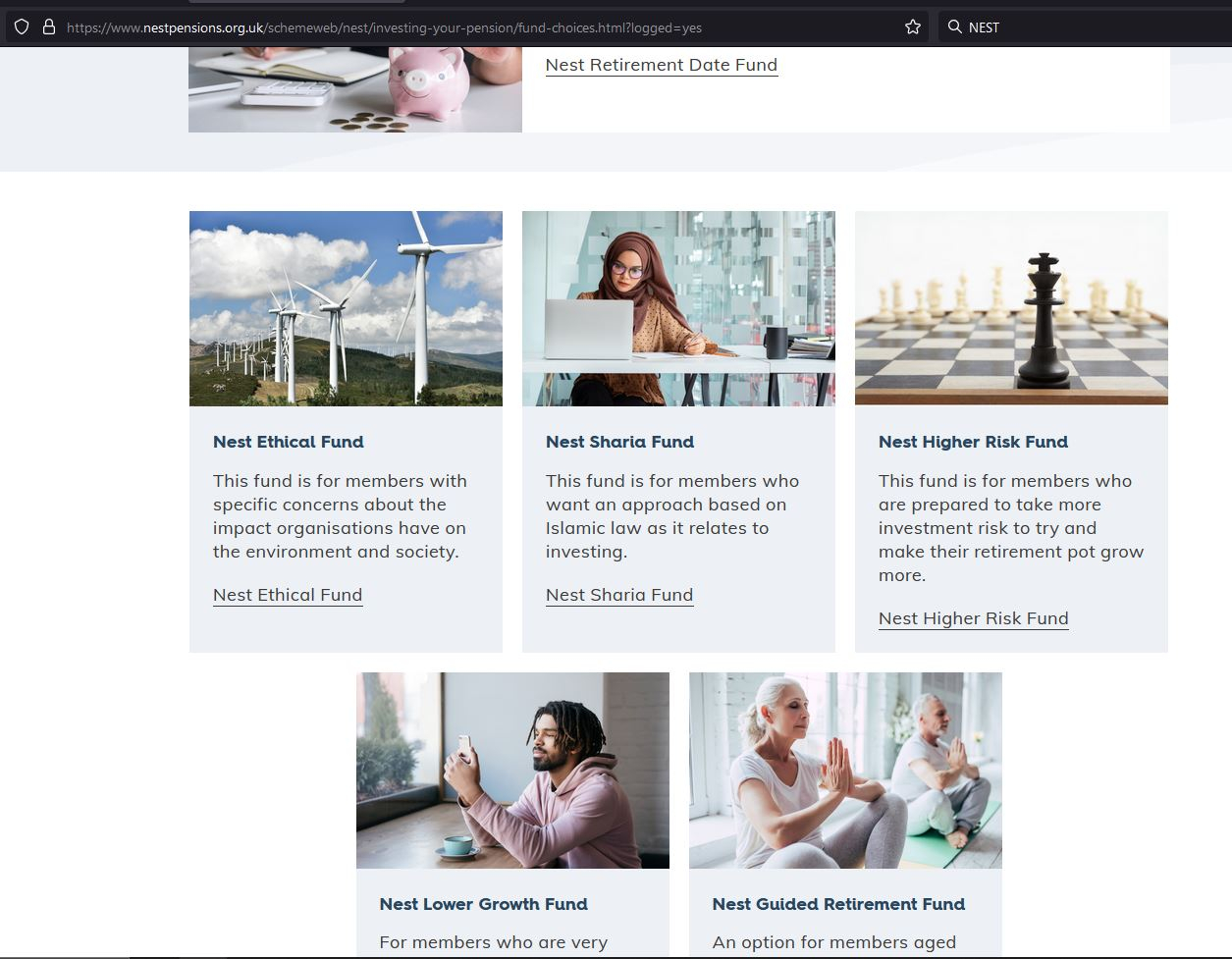

As you can see, this person with nest has selected to be invested in the higher risk fund. There's other options such as ethical, sharia, lower growth etc. If I remember right then once you keep clicking through you can actually see a breakdown of how it's invested. In this example the umbrella could be called higher risk but underneath this it shows how this is broken down.

Something a little similar with the peoples pension. They get options of adventurous, balanced, cautious - so there's choice there. They can do other things like selecting beneficiaries, setting their retirement age, they can easily transfer in from within their online portal.

Then there's now pensions which gives you almost nothing. The only change you can make is an additional contribution in the form of a percentage.

You cannot really do any of the above with the other 2 providers from within your now portal.

If you go on to the now site and dig deep you can find a wishy-washy answer as to how they invest but there is no input from you. Your money goes in, they decide what happens with it and that is final.

It sounds quite similar to Vanguards Target Retirement approach. Speaking of which, I'm not even sure that you can set your retirement age with Now. Maybe you can, but what you can't do which you guys appear to be suggesting must be able to be done, is you can't tell them hey I want to invest more aggressively or more cautiously.

If you want to do that then you need to quit your job & go work for someone who uses a different provider.

Or pay in to a SIPP.

NEST has 6 choices . The retirement date fund ( which is the most used ) and the 5 others shown in your snapshot.

Peoples pension has this on their website.

Unless you tell us otherwise, we’ll automatically invest your money in our ‘balanced’ investment profile. You can choose other investment options through your Online Account if you want to.There’s 3 investment profiles to pick from (‘balanced’, ‘cautious’ or ‘adventurous’). Or, for those who are more confident with investment decisions, you can self-select from our range of nine investment funds.

0 -

Which is what I was saying - in that there really is no option to say I want to invest more aggressively or conservatively. You get what you get.grumiofoundation said:There is no practical difference between a 'workplace' pension and an 'auto-enrolment' pension. The provider is what determines the investment choices.

I don't have a NOW pension so can't log in and see what is there but from what I can see on their website you are invested in their diversified growth fund - no choice in this and as you say can't change, and I agree is very difficult to see what exactly it is invested in (factsheet only gives breakdown of (rather vague) asset classes, no further breakdown), I couldn't find any more details.

https://www.nowpensions.com/app/uploads/2022/05/diversified-growth-fund-factsheet-q1-22.pdf

In members booklet says you can change the age you tell them you want to retire (this will make no difference to when you actually retire). In booklet says you can email them.

https://www.nowpensions.com/app/uploads/2022/04/Member-Booklet-NP-D0065.pdf

One option you could look at if you aren't happy with the investment options is to periodically transfer out from NOW to a different provider (in booklet says is free) - whether your SIPP or a previous workplace pension.

I asked the question (to NOW) years ago, which is why I knew")

I've had it about 7 years now. I should tot it up again as I did it after about the 4-5 year mark & totalled just my contributions, not my employers, just mine & the balance of my pot was actually barely any different to the sum of all my contributions. Pretty poor I thought.

For comparison, my SIPP is with Fidelity. The total percentage it's up as of last month end was 27.52%. The annual percentage it was up was 6.84%.🤐🤐🤐

0 -

Yes, that's exactly what remortgaging is, getting a new deal of any kind instead of going directly into the variable rate of your current lender when your deal ends. You can borrow more (to release some equity), less (if you contribute some extra) or just the outstanding value. The lender will always carry out a valuation of some kind, perhaps you weren't aware of it and it was just what the article called a desktop valuation. In any case they need to assess the value of your property somehow in order to make you the offer.B0bbyEwing said:

It leaves me wondering whether we're talking about the same thing to be honest. I'll say where I'm at and you can tell me if we're on the same page:Expotter said:With regards to property valuation when remortgaging, this might make it clearer

https://hoa.org.uk/services/ask-an-expert-2/ask-an-expert-i-am-managing/how-do-i-value-my-property-before-remortgaging/

I bought a house. Took out a mortgage on it at 102k. We fixed for 5 years with Nationwide.

As that 5 years approached, I went to my IFA & said hey we're nearing the end of our 5 years. I want to lock in on another 5 years but don't have a clue what I'm doing, can you assist again (same guy who sorted us with the initial purchase).

Went to his place, he sorted another 5 year fixed, the cheapest being with who the initial 5 year was with - Nationwide, so that side was made easier.

And now we're 12 months from coming to the end of the existing 5 years.

Is that called remortgaging or not? Is it called something else? Again, not being difficult or awkward here. If anything it just shows my lack of understanding.

Because when you talk about remortgaging & when the links talk about remortgaging, pictures are being painted of having to get a valuation done on the house.

When that isn't something we had to do last time.

More helpful info

https://www.hsbc.co.uk/mortgages/what-is-remortgaging/

1 -

The annual percentage it was up was 6.84%.

It is doing well, most pension pots were down on a 12 months basis at the start of July, but the uptick in the markets in July has probably pushed most back into the positive , but probably not by as much as 7%.

0 -

Now you mention it, I vaguely remember being asked by the IFA the value of the property & saying not a clue. I think they just added on a bit to what we paid because oh well it wont be far wrong will it kind of thing.Expotter said:Yes, that's exactly what remortgaging is, getting a new deal of any kind instead of going directly into the variable rate of your current lender when your deal ends. You can borrow more (to release some equity), less (if you contribute some extra) or just the outstanding value. The lender will always carry out a valuation of some kind, perhaps you weren't aware of it and it was just what the article called a desktop valuation. In any case they need to assess the value of your property somehow in order to make you the offer.

So to paint another extreme again just i order to check I've got this - in theory, you could sign up on a deal like we did & your LTV is say 41%, but you could come next time round in 5 years time to renew again & (in theory) despite having made 5 years of payments, your LTV may actually be more than it was last time round? Depending on whether your house/area has had a massive swing one way or another?

Of course, that is just a very small snapshot & was the status at month end July. For a further breakdown the funds were:Albermarle said:The annual percentage it was up was 6.84%.It is doing well, most pension pots were down on a 12 months basis at the start of July, but the uptick in the markets in July has probably pushed most back into the positive , but probably not by as much as 7%.

Emerging Markets: +8.70%

ESG: +7.18%

VLS100: +37.88%

Now when I go back to month end June it was a little different:

total: 20.96%

Annual: 5.83%

Emerging: +9.33%

ESG: -0.76%

VLS100: 29.79%

Month end May:

total: 27.14%

Annual: 6.89%

Emerging: 11.22%

ESG: 4.68%

VLS100: 37.05%

So I understand the ups & downs. I tend to just invest & forget and not flap when it starts going down. Long road ahead.

I will make a tweak at some point. When I started out I bought in to an emerging markets fund as you can see. I'm not overly happy with it being there to be honest and no longer put any money in to it. One day I'll get round to removing it & moving that money sideways.🤐🤐🤐

0 -

LTV is determined by the value of the mortgage divided by the value of the property (x100 in %). That's it, regardless of what it was in the past. So in theory, yes it could be higher if your property had a big decrease in value, even it the mortgage value is actually less than previously. That's how some people with a high LTV can end up in negative equity sometimes if their mortgage is more than the current value of their house.0

-

If you are above 70% LTV, overpay the mortgage. So that you can get the most competitive interest rates when your fixed term expires.

Once you get below 70% LTV, put the rest into a stocks & shares ISA. Ideally through a stock market index fund. The stock markets return on average 7-8% per year so over the long term that is a complete no brainer.

As an alternative to a stocks & shares ISA, you could invest more into your pension. This has the disadvantage of locking money away from retirement, but the advantage of saving income tax and national insurance.1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 604.9K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.6K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards