We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Guide discussion: Voluntary national insurance contributions

Comments

-

None at allmolerat said:wiley353 said:

Full year N.I. 80-17/18, short fall years 17/18,(237 to top up) 19/20,(126 top up) 21/22 (200 top up). COPE £160 as of April "22 . SRA 17/09/31. unlikely to have full year N.I. to 2031 due to health issuesmolerat said:Sounds about right for a long public sector employment.If those part filled years are post 2016 then in all likelihood they will add to your pension, pre 2016 years are unlikely to add value.Post up your current amount up to April 2022 (or possibly still showing 2021), your number of pre 2016 years, number of post 2016 years, your COPE amount, your gap years and the tax year in which you reach SRA and people here will be able to work it all out for you.At those prices it would be rude not to take advantage It will take you 22 weeks at today's rates to recoup the capital outlayAre you currently receiving any benefits ?0

It will take you 22 weeks at today's rates to recoup the capital outlayAre you currently receiving any benefits ?0 -

None at allmolerat said:wiley353 said:

Full year N.I. 80-17/18, short fall years 17/18,(237 to top up) 19/20,(126 top up) 21/22 (200 top up). COPE £160 as of April "22 . SRA 17/09/31. unlikely to have full year N.I. to 2031 due to health issuesmolerat said:Sounds about right for a long public sector employment.If those part filled years are post 2016 then in all likelihood they will add to your pension, pre 2016 years are unlikely to add value.Post up your current amount up to April 2022 (or possibly still showing 2021), your number of pre 2016 years, number of post 2016 years, your COPE amount, your gap years and the tax year in which you reach SRA and people here will be able to work it all out for you.At those prices it would be rude not to take advantage It will take you 22 weeks at today's rates to recoup the capital outlayAre you currently receiving any benefits ?0 -

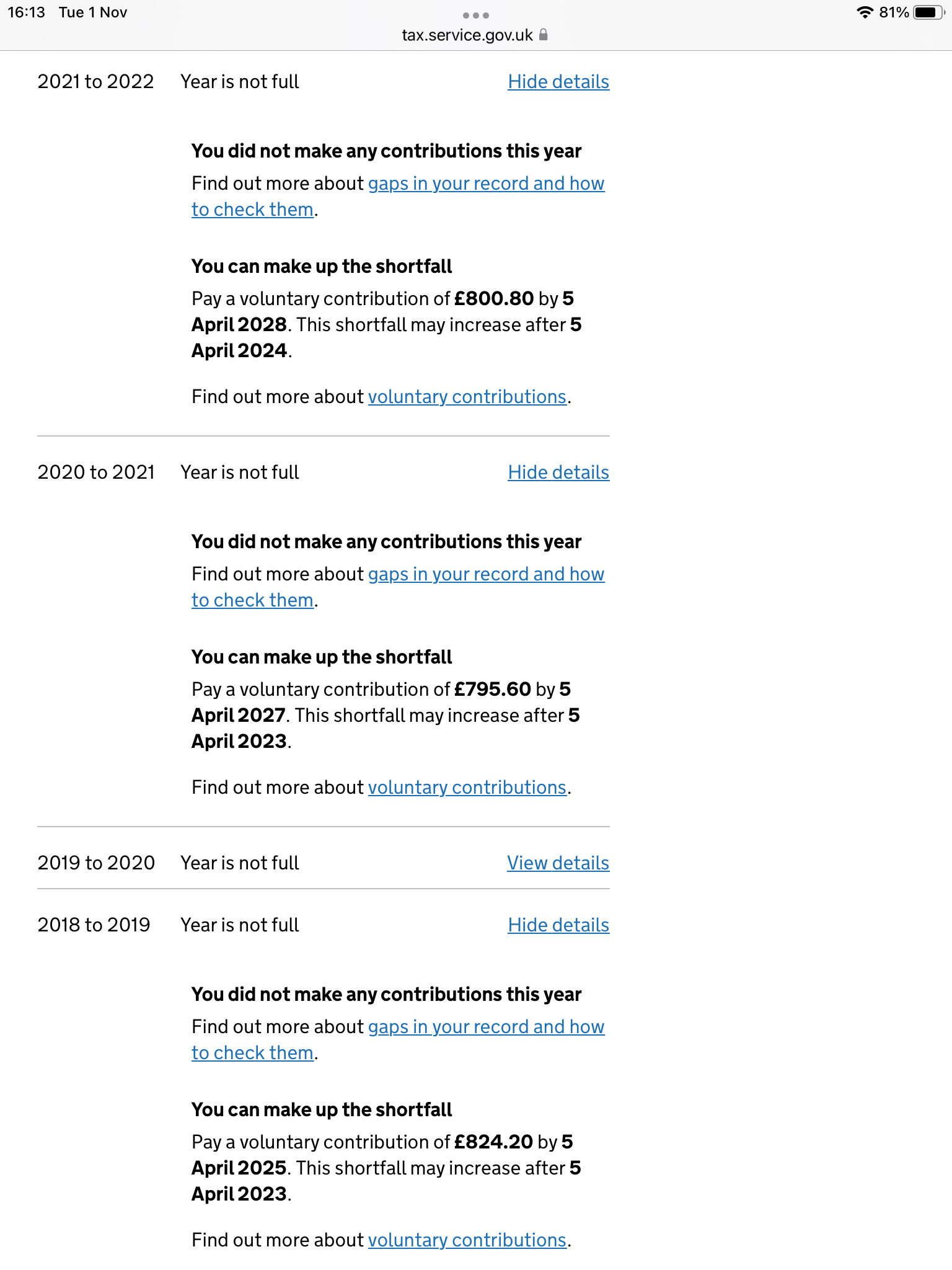

Been reading with interest all the comments on this post. Screenshots of my forecast and shortfalls are attached. I presume it is a no-brainer that I should pay all the shortfalls from 2017 onwards (c£2k) plus another £800 for Y/E 2023 to achieve my maximum forecast of £183.67? Am I also correct in reading that if I make no further NI contributions my forecast will fall to £162.51?

I reach SP age in 2023.

0 -

Yes, £162.51 is what you currently have, do nothing and that is what you will get. Each year you purchase will give you £5.29 per week extra pension so is really a no brainer, a full price year pays back in about 3 years. 20-21 is even better ! The prices of the 2 earliest years will increase after April to likely to around £907.50 & £453.70.

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

0 -

Many thanks. It's taken me a long time to get my head around all of this so your clear explanation is very welcome. Just one other question, will I also have to pay c£800 for Y/E 2023 to achieve £183.67?0

-

I've recently paid two years of voluntary NICs (2019-2020 and 2020-2021, both via Class 2), which takes me from 22 full years to 24 full years (which is confirmed in my NIC record).

Oddly, my state pension forecast has only increased by £5.29 per week. Can anyone think of a reason why this would have happened? Is it possible that the one part of the system has only caught up with one of those voluntary payments, while the other part has caught up with both?

I made the payment for both years via a single BACs payment BACs on 25th October, and I checked my NICs record was updated by 2 years today, and also checked my new state pension forecast today.(Nearly) dunroving0 -

Hi All

Like many of us I've been following this thread.

I think I have a handle on it and like Circusdancer I'm of the belief that making additional contributions is a no-brainer, but I'd really appreciate your thoughts:

I've got my forecast on line and have spoken to the Future Pension helpline, who, once I got through, were incredibly helpful.

My state pension date is 2023 and I have not worked since 2015/16 tax year and I'm not eligible for, nor have applied for any benefits.

The person at the helpline said that if I made payments for 5 (of the 6) years I would be eligible for the full £185.15. He was adamant that I only need to pay the 5 years and said that by paying 4 years I would add £5.29 per week, whereas the final 5th year would add a further £3.57.

This equates to £4,069 and my calculations are that my breakeven is just over 3 years.

I attach screenshots of my shortfall and forecasts:

Any assistance would be very much welcome.

0 -

Yes you need all 4 years, £824.20 is this year's price.Circusdancer said:Many thanks. It's taken me a long time to get my head around all of this so your clear explanation is very welcome. Just one other question, will I also have to pay c£800 for Y/E 2023 to achieve £183.67?

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

1 -

Lou117 said:

The person at the helpline said that if I made payments for 5 (of the 6) years I would be eligible for the full £185.15. He was adamant that I only need to pay the 5 years and said that by paying 4 years I would add £5.29 per week, whereas the final 5th year would add a further £3.57.

This equates to £4,069 and my calculations are that my breakeven is just over 3 years.The full £185.15 less your currently held £160.42 = £24.73. Divide that by the £5.29 you get for each year purchased = 4.67 years. .67 x £5.29 = £3.57 for the final year.Any looking after grandchildren whilst the parent works ?Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards