We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Guide discussion: Voluntary national insurance contributions

Comments

-

You need to post info from her record for anyone to check whether it’s worth paying all or some of those 7 years.pritchah said:

Thanks. I just put down all I thought was relevantDazed_and_C0nfused said:

Could you explain why you think buying 11 years is appropriate?pritchah said:Hello - my wife has 11 payable gaps which we calculate as needing £8.6k to fill

She has just passed her 69th birthday and is receiving £708.16 state pension every four weeks

I think her full pension entitlement would be £805.32 (same as I'm getting) - so she'd be better of by £97 every four weeks, or £1164 a year

So according to the MSE ready-reckoner if we paid the £8.6k she would break even in three years

But, as she asked me yesterday £8.6 divided by £1164 looks more like it would take around 7 years to pay off

I'm sure my maths or logic is letting me down somewhere, or is it all to to with pre- and post-tax amounts?

Help please

And why is your pension amount relevant to her?

If she is getting £177.04/week now then wouldn't 7 years take her to £221.20/week?

However she may not have 7 years which can benefit her, you would need to provide more details for anyone to help you with that aspect.

What I really wanted was for my wife to be able to fill her NI gaps so she got the full pension

Last thing I want to do is overpay the govtFashion on the Ration

2024 - 43/66 coupons used, carry forward 23

2025 - 62/890 -

pritchah said:What I really wanted was for my wife to be able to fill her NI gaps so she got the full pensionThe short answer is she'll definitely benefit by buying up to 7 years after 2016, so 2016/17 or later. She might (or might not) benefit from pre-2016 years.If you post the full details - her current forecast, the green box and the text that follows, and including which years are available, and at what price - someone will be able to suggest the best ones to buy.

N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 37 MWh generated, long-term average 2.6 Os.0 -

Here is the list of payable gapsQrizB said:pritchah said:What I really wanted was for my wife to be able to fill her NI gaps so she got the full pensionThe short answer is she'll definitely benefit by buying up to 7 years after 2016, so 2016/17 or later. She might (or might not) benefit from pre-2016 years.If you post the full details - her current forecast, the green box and the text that follows, and including which years are available, and at what price - someone will be able to suggest the best ones to buy.You have 11 payable gaps

The cost of filling each gap depends on the amount of National Insurance already paid in that tax year.

Gaps Cost of filling gaps 2020 to 2021 £795.60 2019 to 2020 £824.20 2018 to 2019 £824.20 2017 to 2018 £824.20 2016 to 2017 £824.20 2015 to 2016 £824.20 2014 to 2015 £824.20 2013 to 2014 £824.20 2012 to 2013 £824.20 2011 to 2012 £824.20 2010 to 2011 £412.10 0 -

How many full years does she have in total ? Was she in a contracted out pension scheme ? Does she receive a work pension ?The only years that are guaranteed to add to the pension are the 5 from 2016-17 to 2020-21 which would take her to £208.64. Any others are down to personal circumstances and dependent on the above points.

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

1 -

Thanks all for your comments on my original query about my wife's state pension. I've done some digging around and now found her pension forecast dated 1/11/2001

At that time her forecast was £150.23 a week (£653.23 a month, £7838.79 a year)

As I previously posted -You have 11 payable gaps

The cost of filling each gap depends on the amount of National Insurance already paid in that tax year.

And here is her complete recordGaps Cost of filling gaps 2020 to 2021 £795.60 2019 to 2020 £824.20 2018 to 2019 £824.20 2017 to 2018 £824.20 2016 to 2017 £824.20 2015 to 2016 £824.20 2014 to 2015 £824.20 2013 to 2014 £824.20 2012 to 2013 £824.20 2011 to 2012 £824.20 2010 to 2011 £412.10 View payable gaps2020 to 2021Year is not full2019 to 2020Year is not full2018 to 2019Year is not full2017 to 2018Year is not full2016 to 2017Year is not full2015 to 2016Year is not full2014 to 2015Year is not full2013 to 2014Year is not full2012 to 2013Year is not full2011 to 2012Year is not full2010 to 2011Year is not full2009 to 2010Full year2008 to 2009Full year2007 to 2008Full year2006 to 2007Full yearYour National Insurance record before April 2006

It’s too late to pay for gaps in your National Insurance record before April 2006.

2005 to 2006Full year2004 to 2005Full year2003 to 2004Full year2002 to 2003Full year2001 to 2002Full year2000 to 2001Full year1999 to 2000Full year1998 to 1999Full year1997 to 1998Full year1996 to 1997Full year1995 to 1996Full year1994 to 1995Full year1993 to 1994Full year1992 to 1993Full year1991 to 1992Full year1990 to 1991Full year1989 to 1990Full year1988 to 1989Full year1987 to 1988Full year1986 to 1987Full year1985 to 1986Full year1984 to 1985Full year1983 to 1984Full year1982 to 1983Full year1981 to 1982Full year1980 to 1981Full year1979 to 1980Full year1978 to 1979Full year1977 to 1978Full year1976 to 1977Full year1975 to 1976Full yearUp to 1975Our records show you have 4 full years up to 5 April 1975

Hope this all helps0 -

As she has in excess of 35 full years prior to 2016 only those 5 post 2016 can be purchased. That £4092.40 will give £31.60 per week.So you need to get that call back booked Request a call back to pay voluntary National Insurance contributions - GOV.UK and get those years paid. It could be up to a year before the increased pension comes into payment but it will be backdated to receipt of the contributions.

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

3 -

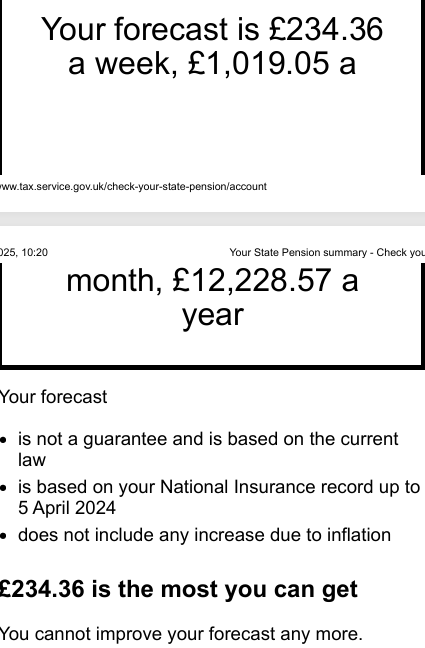

I think I have asked before and I really can't believe it, but checking our state pension forecast, neither Mrs G-C or I need to make any further NI contributions to ensure the maximum available state pension.

I have attached the checks we did online this morning. Mrs G-C had a period of contracted out pension (NHS) which is why I think her forecast is lower than mine. We both have missing years but there seems to be no benefit in us topping up those years.

Have I understood this correctly?

Mrs G-C forecast:

Mr G-C forecast:

0 -

Have I understood this correctly?

Yep, you are both home and dry.

For yourself nothing you have done / paid since April 2016 has added to your pension apart from the annual inflationary increases. You were already there at the inception of the new pension. You are one of the likely losers as you would have continued to build up S2P if you continued working. Only the basic £221.20 will increase with the triple lock, the remaining protected payment will only increase with CPI.

Never associate with idiots on their own level, because, being an intelligent man, you'll try to deal with them on their level - and on their level they'll beat you every time.

Being hated by idiots is the price you pay for not being one of them.

Jean Cocteau 1889-1963

1 -

Thank youmolerat said:Have I understood this correctly?Yep, you are both home and dry.

For yourself nothing you have done / paid since April 2016 has added to your pension apart from the annual inflationary increases. You were already there at the inception of the new pension. You are one of the likely losers as you would have continued to build up S2P if you continued working. Only the basic £221.20 will increase with the triple lock, the remaining protected payment will only increase with CPI.

0

0 -

Please forgive me for being particularly cautious on this, but the statements are that we have both accrued the full state pension (plus a bit in my case). This is not with an assumption that we will both accrued further contributions / credits each year until we reach state pension age?

I am still working and accruing NI years, but Mrs G-C is not currently working or securing credits via any other means.

I kind of find it remarkable given we are both early 50's and need to wait until at least 67 before receiving state pension.

I assume that the "S2P" referred to a couple of post up is what I paid in at the time as SERPS?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards