We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Buying an Annuity young?

MrE1

Posts: 43 Forumite

I've read online one can buy an annuity at any age (ie swap a lump sum for an annual salary for life).

Does any one have their own experience of this and know where to buy one? I'm 37

Does any one have their own experience of this and know where to buy one? I'm 37

0

Comments

-

You can but people complain about the rates on annuities bought at retirement and buying earlier will result in worse rates and crippled by 50 years + of admin fees which inflate each year.

I assume you want the payments to start straight away and not have it in deferment2 -

Does any one have their own experience of this and know where to buy one?Theoretically possible, but commercially, a total no go. No sensible website would even hint that it is a good idea.

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.3 -

Are you talking about an immediate annuity or a deferred annuity? Would it be linked to some other insurance component. Be very careful as these products can be complicated and potentially expensive, but they might be complimentary to other pension and investing provisions like SIPPs and ISA.

FYI when I was young I bought a deferred annuity that credited at an annual rate linked to prevailing interest rates (I'm in the US so such products might not be available in the UK) . I can turn it into a lifetime annuity at any time to provide lifetime income. It is a conservative investment that provides diversity to my portfolio and a foundation to my other stock market investments. So think of an annuity as just one component of your total finances. Right now an annuity will be expensive because interest rates are still low, but as they go up you will get more income for your lump sum.

“So we beat on, boats against the current, borne back ceaselessly into the past.”1 -

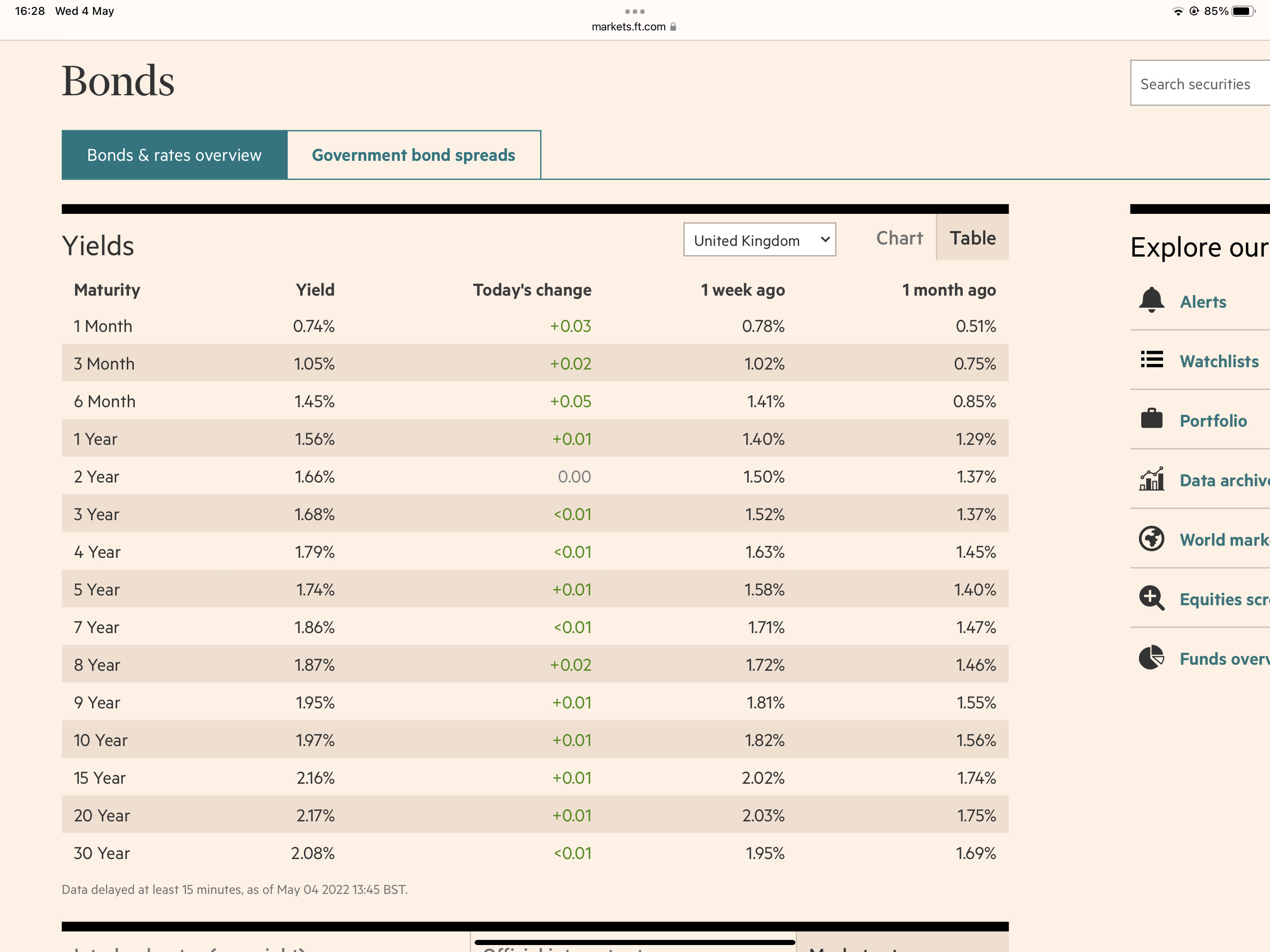

You can guarantee that the rate would be awful. You could sort-of do it yourself by buying long dated gilts e.g., the current annual yield to maturity on the benchmark 30 year gilt is 2.08%. The insurer would probably use these rates as a starting point as well. Anything inflation linked would no doubt be exceptionally low to begin with.MrE1 said:I've read online one can buy an annuity at any age (ie swap a lump sum for an annual salary for life).

Does any one have their own experience of this and know where to buy one? I'm 37

1 -

On the assumption that the annuity route is a non-starter, what are you trying to achieve? Your other threads about using a modest lump sum to invest standalone or via a pension seem like much better ideas - what's your thinking behind dismissing those more mainstream options?MrE1 said:I've read online one can buy an annuity at any age (ie swap a lump sum for an annual salary for life).

Does any one have their own experience of this and know where to buy one? I'm 372 -

BMWs are nothing special in terms of cost. Especially at the fleet or budget model end. And actuaries for insurers are not the most well-paid jobs. Annuities don't have explicit charges anyway. You get the annuity terms at the outset. The margin on annuities for an insurer are less than a savings account for a bank.Thumbs_Up said:

Didn't know that, thought it was a one off payment ref admin fees. No wonder they have BMW's on the drive.Sandtree said:worse rates and crippled by 50 years + of admin fees which inflate each year.I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

I won’t push you to an annuity but we don’t want a fully one sided discussion.Yes, but if you’re still alive in 31 years the bonds are no longer paying but the annuity is/should be.

You could sort-of do it yourself by buying long dated gilts e.g., the current annual yield to maturity on the benchmark 30 year gilt is 2.08%.

And yes, but the bonds don’t have the benefit of mortality credits ie some of the annuitants will die early leaving money to pay those who live loooong.

And yes, it won’t pay as much each year compared with buying it at age 57 years, but you’d have 20 years of income the later annuitant never got.

But you give up a lot of opportunity by handing over your money at age 37.1 -

So when it matures you buy another gilt or an annuity or whatever. Obviously you could be looking at a capital loss but you can also change your mind and sell them at any point. If you croak someone can inherit them. There's no changing your mind with an annuity.JohnWinder said:I won’t push you to an annuity but we don’t want a fully one sided discussion.Yes, but if you’re still alive in 31 years the bonds are no longer paying but the annuity is/should be.

You could sort-of do it yourself by buying long dated gilts e.g., the current annual yield to maturity on the benchmark 30 year gilt is 2.08%.

And yes, but the bonds don’t have the benefit of mortality credits ie some of the annuitants will die early leaving money to pay those who live loooong.

And yes, it won’t pay as much each year compared with buying it at age 57 years, but you’d have 20 years of income the later annuitant never got.

But you give up a lot of opportunity by handing over your money at age 37.2 -

Thank you everyone

0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards