We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Annuities

Comments

-

You could take your 25% tax free and use that to buy your wife an annuity. That's still converting tax free money to taxable money though, if her income then exceeds 12,570.NedS said:

...The main issue for us is when one partner dies, so maybe waiting until that happens with the surviving partner converting remaining SIPP to an annuity rather than each buying joint life annuities now, especially as our SIPP assets are not evenly balanced so OH does not have assets that can be used to directly purchase an annuity and I would presumably have to pay tax to withdraw from my SIPP for OH to purchase a joint life annuity.

You would still retain the option of moving your crystallised 75% to an annuity of your own without getting a tax bill. Of course, your annuity income would be taxable, whereas the SIPP could pass tax free if you die before age 75.

Made up example:

You wait 1 year.

Annuity rate offered is now 3.2%

Your wife's State Pension is 10,000. Personal allowance 12,570

You buy her an annuity with 85,000. This pays 2,720 per year.

So her income is now roughly equal to her personal allowance. Can't make any more without paying tax.

No rush to do this though. Annuity rates get more attractive as you get older.1 -

Secret2ndAccount said:

I am not a believer in the 4% rule. For a 30 year, properly invested SWR, I think 3% is probably OK, but if you want to get closer to the nailed-on safety of an annuity, I would start at 2.5% and review every few years - maybe you can increase to 3% if the first few years weren't a disaster. At age 65, a 30 year time horizon would be fairly safe. Maybe you could start at 3% SWR, though having to cut back would not be out of the question. Therefore, if annuity rate was 3% you might opt for it. Depends on your risk averseness, and your inheritance wishes. With SWR, you keep some risk, but you keep potentially a lot of inheritance.NedS said:All else being equal, at what rate would a single life, aged 65, RPI annuity become attractive?HL are currently quoting 2.92% on their best buy tables and from the above discussions, we are all assuming that figure will rise so 3% looks a given. We already have a good chunk of DB/SP to come, but if rates get anywhere near 5% by the time I hit 65 I think I'll be seriously considering adding some annuity.The main issue for us is when one partner dies, so maybe waiting until that happens with the surviving partner converting remaining SIPP to an annuity rather than each buying joint life annuities now, especially as our SIPP assets are not evenly balanced so OH does not have assets that can be used to directly purchase an annuity and I would presumably have to pay tax to withdraw from my SIPP for OH to purchase a joint life annuity.

So, if you just want to forget about it and sleep at night, 3%. If you have children, and would like to pass on a small fortune in the event you go early, higher than 3%. So, in your case - wanting to protect your spouse, maybe a bit higher than 3%.

Reasons why I don't like the 4% rule:- 4% worked for an optimally invested portfolio - chose the right market and didn't suffer any unfortunate events. We can't all count on being that lucky.

- 4% doesn't account for costs. Even with a great portfolio, the 4% wouldn't actually be achieved because there are always costs.

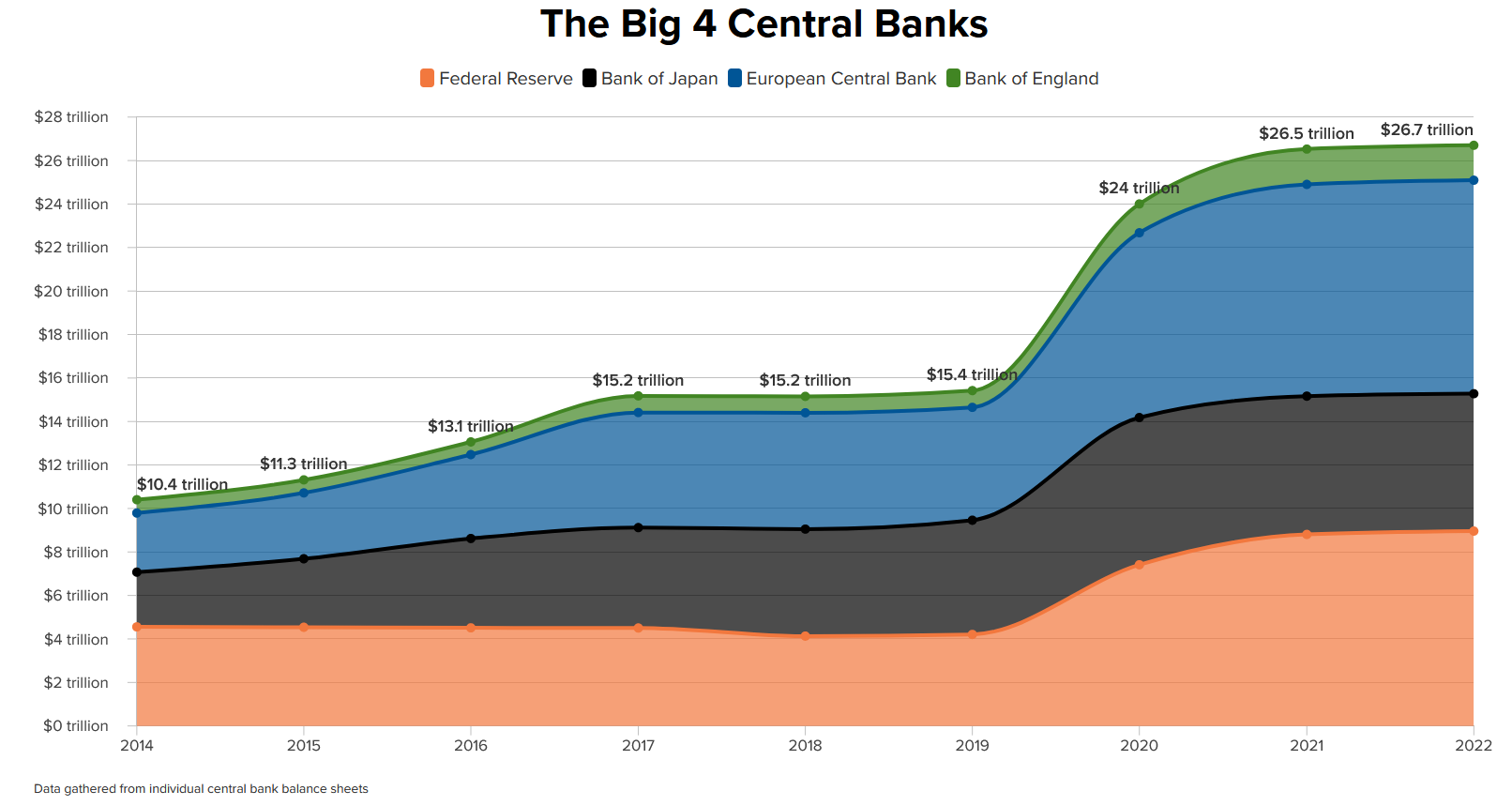

- Only in recent times have central banks started major QE programs. This really messes with bond prices. Therefore I don't believe that even 100 years of historical data is suitable to back-test the SWR method. This time really is different. Bonds have historically been somewhat uncorrelated with stocks so that the two provide protection for each other. Today, bond returns simply suck, and don't protect against equity downturn. SWR can't be relied upon until QE is over. (Which might only be a year or two...)

- Even though the SWR is successful in 99% of cases, (or 95% or 100%...) there were cases where the pot was grievously diminished during its lifetime, but turned out OK. The retiree would have cut their income in order to protect the pot, even though it turned out to be unnecessary. That case should be regarded as a fail, not a pass.

- Constant SWR is too blunt an instrument for a long retirement. It serves a purpose for planning and estimating, but there must be some willingness to re-evaluate.

- Many people don't have constant income in retirement. They start multiple pensions at different ages. They downsize, or inherit, or do equity release. Therefore a personalised model is needed, as the withdrawal rate will change.

"SWR can't be relied upon until QE is over. (Which might only be a year or two...)"

Have a look at historical events

https://www.timelineapp.co/blog/no-qe-didnt-break-the-4-rule/

"4% doesn't account for costs. Even with a great portfolio, the 4% wouldn't actually be achieved because there are always costs.

Longevity and investor misbehaviour also needs to be taken into account. 4% has historically been achievable with certain portfolios (tilting towards EM and small-cap value).

"and don't protect against equity downturn."

They worked in 2000, 2008 and 2020. What period were you referring to?

" Bonds have historically been somewhat uncorrelated with stocks"

Depends what time period you are looking at

https://occaminvesting.co.uk/is-the-stock-bond-correlation-about-to-turn-positive/

0 -

I don't get that bit. No unfortunate events?Secret2ndAccount said:- chose the right market and didn't suffer any unfortunate events. We can't all count on being that lucky.

0 -

westv said:

I suppose I was just trying to compare to an "average" final salary pension.michaels said:

And it is easy to argue that even 50% partner benefit is worse than SWR where the partner effectively gets 100%.westv said:I wonder if RPI, 50% survivor, age 60 rates will get to 3.5%/4%? Unlikely I assume.An effective 75% partner benefit rate could be achieved by splitting a pot equally and each purchasing a joint life annuity with 50% partner benefit. So instead of purchasing a single annuity paying £10k with a £200k pot with 50% partner benefits, each purchase a £5k annuity using half the pot (£100k each) and each benefit from £5k self and £2.5k partner benefits should the other die first.I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.1 -

I don't understand that. Surely if you want to leave more to your children you would need to reduce your sending not increase it? And the same for protecting your spouse.Secret2ndAccount saidNedS said:So, if you just want to forget about it and sleep at night, 3%. If you have children, and would like to pass on a small fortune in the event you go early, higher than 3%. So, in your case - wanting to protect your spouse, maybe a bit higher than 3%.

0 -

That article plots bond yields minus inflation. The chart has some pretty scary lows during periods of hyperinflation. Nonetheless, it shows a prolonged and increasingly negative trend in the last 27 years. It ends with a real yield of zero. The current number, I would say, is about -4 or -5%, so we have no way of knowing how that works out for today’s SWR.

I’m not saying that SWR can’t work with negative real yields. I’m saying that 4% SWR can’t work with yields artificially held down by massive QE. It’s been fine for the last decade because equities have been on fire, and inflation dormant. Now we have high inflation, and faltering equities. This is the point where bonds come to the rescue. Except the yields are depressed by the QE actions of central banks. This time is different because bond yields are not the result of a free market.

I don’t think all is lost because QE won’t go on forever. The US Fed has already announced plans to end QE. However, the ECB has no such intentions, so we will have to see where this goes.

The article you quote above, and the article it references both state that 4% is not achievable in the real world.... 4% has historically been achievable with certain portfolios (tilting towards EM and small-cap value)."and don't protect against equity downturn."

They worked in 2000, 2008 and 2020. What period were you referring to?Current QE is enormous, and dwarfs the earlier programs. We had previous equity dips during QE, but not with such high inflation, and such huge QE. I think we are in uncharted waters right now.

The requirement is for stocks and bonds to be uncorrelated, which, according to your reference appears to have been the case since 1870. Whether R² is +0.2 or -0.2 isn't the point. It's not .8, and that's what matters.BritishInvestor said:" Bonds have historically been somewhat uncorrelated with stocks"

Depends what time period you are looking at

https://occaminvesting.co.uk/is-the-stock-bond-correlation-about-to-turn-positive/

1 -

westv said:

I don't get that bit. No unfortunate events?Sorry, I was trying (unsuccessfully) to keep my post brief. I should have been more explicit.

I’m not talking about World Wars or pandemics. We all have those. When Bengen did his math, he had access to a good USA data set, and used US stocks and bonds. He came up with 4.1% as his result. Suppose a Japanese investor had read this paper and decided to invest in the Nikkei. From 1990-2020 the Nikkei returned -9%. In the same time, the US S&P returned about 2000%. This is what I mean by an unfortunate event: a 30 year retirement where stocks never made any money. Not an obviously stupid investment policy - just things not working out at all.

Unfortunately a globally diversified index portfolio is designed to lessen risk, and therefore reward, and drops the 4% achievable SWR down to about 3%

About 15 years ago, before FANG, the acronym du jour was BRIC. Brazil, Russia, India, China. That was where you were supposed to put your money. Brazil had some fantastic years, but also some very bad ones. So you might have done okay, save for the fact that the Brazillian Real has halved in value. If you invested in Russia you would be wondering if you will ever see any of your money again. The Indian tiger has failed to roar. China offered great returns for a number of years. Then they remembered they were communists, and took a knife to many of their own best international companies. You can’t buy Chinese stocks – only a ‘Variable Interest Entity’ which is supposed to trade alongside the stock. Except that the Chinese government can decide at any time that the VIE no longer applies, and your investment is worth zero. That would be an unhappy event.

2 -

I was answering the question: "All else being equal, at what rate would a single life, aged 65, RPI annuity become attractive?"Terron said:

I don't understand that. Surely if you want to leave more to your children you would need to reduce your sending not increase it? And the same for protecting your spouse.Secret2ndAccount saidNedS said:So, if you just want to forget about it and sleep at night, 3%. If you have children, and would like to pass on a small fortune in the event you go early, higher than 3%. So, in your case - wanting to protect your spouse, maybe a bit higher than 3%.

I wasn't suggesting SWR's. I did quote the question before answering it")

0 -

I think it's important to make the distinction between what has happened and what might happen.Secret2ndAccount said:That article plots bond yields minus inflation. The chart has some pretty scary lows during periods of hyperinflation. Nonetheless, it shows a prolonged and increasingly negative trend in the last 27 years. It ends with a real yield of zero. The current number, I would say, is about -4 or -5%, so we have no way of knowing how that works out for today’s SWR.

I’m not saying that SWR can’t work with negative real yields. I’m saying that 4% SWR can’t work with yields artificially held down by massive QE. It’s been fine for the last decade because equities have been on fire, and inflation dormant. Now we have high inflation, and faltering equities. This is the point where bonds come to the rescue. Except the yields are depressed by the QE actions of central banks. This time is different because bond yields are not the result of a free market.

I don’t think all is lost because QE won’t go on forever. The US Fed has already announced plans to end QE. However, the ECB has no such intentions, so we will have to see where this goes.

The article you quote above, and the article it references both state that 4% is not achievable in the real world.... 4% has historically been achievable with certain portfolios (tilting towards EM and small-cap value)."and don't protect against equity downturn."

They worked in 2000, 2008 and 2020. What period were you referring to?Current QE is enormous, and dwarfs the earlier programs. We had previous equity dips during QE, but not with such high inflation, and such huge QE. I think we are in uncharted waters right now.

The requirement is for stocks and bonds to be uncorrelated, which, according to your reference appears to have been the case since 1870. Whether R² is +0.2 or -0.2 isn't the point. It's not .8, and that's what matters.BritishInvestor said:" Bonds have historically been somewhat uncorrelated with stocks"

Depends what time period you are looking at

https://occaminvesting.co.uk/is-the-stock-bond-correlation-about-to-turn-positive/

"I’m saying that 4% SWR can’t work with yields artificially held down by massive QE."

Putting aside the relevance of a given "rule" to a given investor, it really depends what a future scenario gives us. For example, this may or may not happen (or worse)

"According to Professor Elroy Dimson, UK bond investors lost half their wealth in real terms in the inflationary period from 1972 to 1974! In the period between 1914 and 1920, UK bonds lost over 60% in real terms over seven consecutive years. But the SWR framework would have held its own during this period"

SWR comes under pressure when we have both bonds and equities getting hit, high inflation, and all for a sustained period.

"Now we have high inflation, "

If you look at the historical worst time to retire, the late 60s features strongly, partly due to the lumpy inflation in the 70s. We are nowhere near that (yet!)

"and faltering equities"

Global equities are down single digits YTD (with small-cap value far less - more on that below). Is this anything more than noise?

"The article you quote above, and the article it references both state that 4% is not achievable in the real world."

The article is for a 50/50 portfolio. The "global" equity part is most likely developed only. Abraham himself offers a portfolio service (Betafolio) and a tool (Timeline) where you can evaluate "tilts" that have historically improved portfolio sustainability.

Nudge the equity content up, and >4% has been achievable for a tilted portfolio over a 30-year horizon, assuming fees have been kept low. This may or may not be the case going forward. And to be fair, few people would be prepared to invest this way, preferring to chase recent winners, even though history shows us this is suboptimal.

"Whether R² is +0.2 or -0.2 isn't the point. It's not .8, and that's what matters."

I must admit I'm not really clear on your correlation point. For me, correlation matters during times of stress, not benign markets. The worry is if we have a 1970s scenario again when both bonds and stocks both suffer - see the step up in the 1970s correlation on the graph.0 -

"Unfortunately a globally diversified index portfolio is designed to lessen risk, and therefore reward, and drops the 4% achievable SWR down to about 3%"Secret2ndAccount said:westv said:

I don't get that bit. No unfortunate events?Sorry, I was trying (unsuccessfully) to keep my post brief. I should have been more explicit.

I’m not talking about World Wars or pandemics. We all have those. When Bengen did his math, he had access to a good USA data set, and used US stocks and bonds. He came up with 4.1% as his result. Suppose a Japanese investor had read this paper and decided to invest in the Nikkei. From 1990-2020 the Nikkei returned -9%. In the same time, the US S&P returned about 2000%. This is what I mean by an unfortunate event: a 30 year retirement where stocks never made any money. Not an obviously stupid investment policy - just things not working out at all.

Unfortunately a globally diversified index portfolio is designed to lessen risk, and therefore reward, and drops the 4% achievable SWR down to about 3%

About 15 years ago, before FANG, the acronym du jour was BRIC. Brazil, Russia, India, China. That was where you were supposed to put your money. Brazil had some fantastic years, but also some very bad ones. So you might have done okay, save for the fact that the Brazillian Real has halved in value. If you invested in Russia you would be wondering if you will ever see any of your money again. The Indian tiger has failed to roar. China offered great returns for a number of years. Then they remembered they were communists, and took a knife to many of their own best international companies. You can’t buy Chinese stocks – only a ‘Variable Interest Entity’ which is supposed to trade alongside the stock. Except that the Chinese government can decide at any time that the VIE no longer applies, and your investment is worth zero. That would be an unhappy event.

Do you have the dataset for this? I'm seeing a higher number.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.2K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards