We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Annuities

Comments

-

A shame you can’t buy an annuity from your own savings cash reserves.

In my youth i didn’t really understand pensions and investing in general, but for some reason I keep a eye on the annuity rates at that time. This figure always has stuck in my mind - for a 65 year old, £100,000 fund on a single life level, and no guaranteed period was £10,000 per annum. For some reason i thought this was a good deal.

I can’t find a link for historic annuity rates so can’t arcuately date this period.

0 -

A shame you can’t buy an annuity from your own savings cash reserves.You can....

I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

A shame you can’t buy an annuity from your own savings cash reserves

Purchased life annuity (PLA) | Hargreaves Lansdown (hl.co.uk)

1 -

Today you'd be lucky to get 4%.Thumbs_Up said:...

In my youth i didn’t really understand pensions and investing in general, but for some reason I keep a eye on the annuity rates at that time. This figure always has stuck in my mind - for a 65 year old, £100,000 fund on a single life level, and no guaranteed period was £10,000 per annum. For some reason i thought this was a good deal.

In 1990 the rate peaked at about 15%. We still see some people on this forum who have a 10% guaranteed annuity when they convert their pot into a pension. Lucky them. With life expectancy rising I doubt we will ever see those numbers again, though I'm sure we will see better than 4%0 -

According to HL's website the current best 65 single life level annuity is 5.584%0

-

I think you're talking about two different kinds of 'level'. I could be wrong though. I think the OP was using the word in a general way, and not referring to a level annuity. I don't think level annuities were common 25 years ago. I think some of them had fixed annual % increases, but it wasn't normally zero. More like 3% or 5% because inflation couldn't be trusted to sit at 2% for extended periods. Would love to hear more on this from someone with better historical knowledge.

0 -

Extremely common. Life expectancy was shorter a few decades ago. Annuities were also far more restricted in terms of choice of product. Few providers offered uncapped inflation protection. The experience of the 70's was still fresh in peoples minds.Secret2ndAccount said:. I don't think level annuities were common 25 years ago.1 -

Try Cannon and Tonks, UK annuity price series, 1957–2002, (Figures 1 and 2, and Table 3 are particularly interesting), there's a full text version at http://people.exeter.ac.uk/ipt201/research/Cannon and Tonks FHR Final Version.pdf and yes, there are lengthy periods (1950s to mid 1990s) when a male aged 65, level annuity could be purchased to provide an income of over 10% of premium (it peaked at 16% in 1975).Thumbs_Up said:A shame you can’t buy an annuity from your own savings cash reserves.

In my youth i didn’t really understand pensions and investing in general, but for some reason I keep a eye on the annuity rates at that time. This figure always has stuck in my mind - for a 65 year old, £100,000 fund on a single life level, and no guaranteed period was £10,000 per annum. For some reason i thought this was a good deal.

I can’t find a link for historic annuity rates so can’t arcuately date this period.

As others have said, increases in longevity means that those annuity rates are unlikely to return (even if interest rates do go up). I suspect (but may be wrong) that the temporarily reduced longevity in the over 60s caused by the pandemic will be ignored by the insurance company actuaries (although it will come out in the ONS data).

2 -

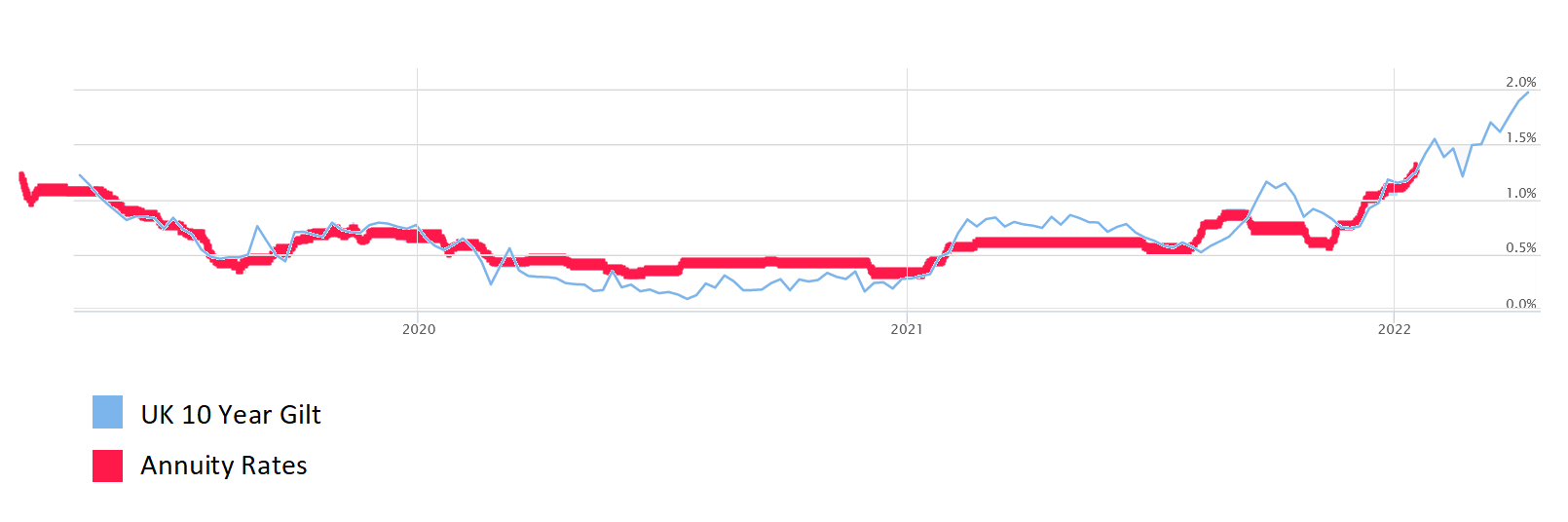

You are in favour of market timing?Secret2ndAccount said:westv said:... where do we see rates being at in 12 months time...I believe that annuity offers are strongly linked to gilt rates (UK treasuries). Here is a graph of annuity rates overlaid with gilt rates. I have moved the annuities to the left about 3 mths as they take time to catch up.

Gilt rates will rise substantially in the next year (already have, so there is already an inbuilt rise in annuities to come). Annuity rates will rise substantially in the next year.

If you can afford to wait before buying an annuity you should do so.

0 -

If you are going to buy an annuity you either buy it now or later. Which option would you go for if you were?najan49 said:

You are in favour of market timing?Secret2ndAccount said:westv said:... where do we see rates being at in 12 months time...I believe that annuity offers are strongly linked to gilt rates (UK treasuries). Here is a graph of annuity rates overlaid with gilt rates. I have moved the annuities to the left about 3 mths as they take time to catch up.

Gilt rates will rise substantially in the next year (already have, so there is already an inbuilt rise in annuities to come). Annuity rates will rise substantially in the next year.

If you can afford to wait before buying an annuity you should do so.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards