We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Annuities

Comments

-

Unlike the QE which supported the global financial system from total collapse. The most recent tranche of QE has ended up in peoples pockets driving demand (and asset prices). QT is akin to going cold turkey. The patient needs to be weaned off the bunch bowl of cheap money that's been sloshing around. Interesting times do lie ahead. With a fickle global economy and external geopoltical events compounding the uncertainty as powerfull forces collide. .michaels said:

Depends to what extent near term inflation impacts on the 50 year expectation, I can see the curve becoming inverted as the current commodity driven price spike feeds through into a 'real' recession.Thrugelmir said:

I'd hazard a guess at a minimum BOE base rate of 2.25% - 2.75% in 12 months time. With 50 year gilts yielding in excess of 3%. Nor will major Central Banks have achieved their objective of bringing inflation back to 2% levels within 2 years. The genie is out of the bottle.westv said:

I'll put that in the "I have no idea" pile.Thrugelmir said:

Six months ago maturity yield on 50 year UK Government bonds was 1.12%. Today it's 1.75%. Shows how quickly the weather can change in the markets.westv said:Getting back to annuities for the moment, where do we see rates being at in 12 months time. Yes, I know nobody can know for certain.1 -

Do section 32 pension have to be taken as an annuity?

0 -

westv said:... where do we see rates being at in 12 months time...

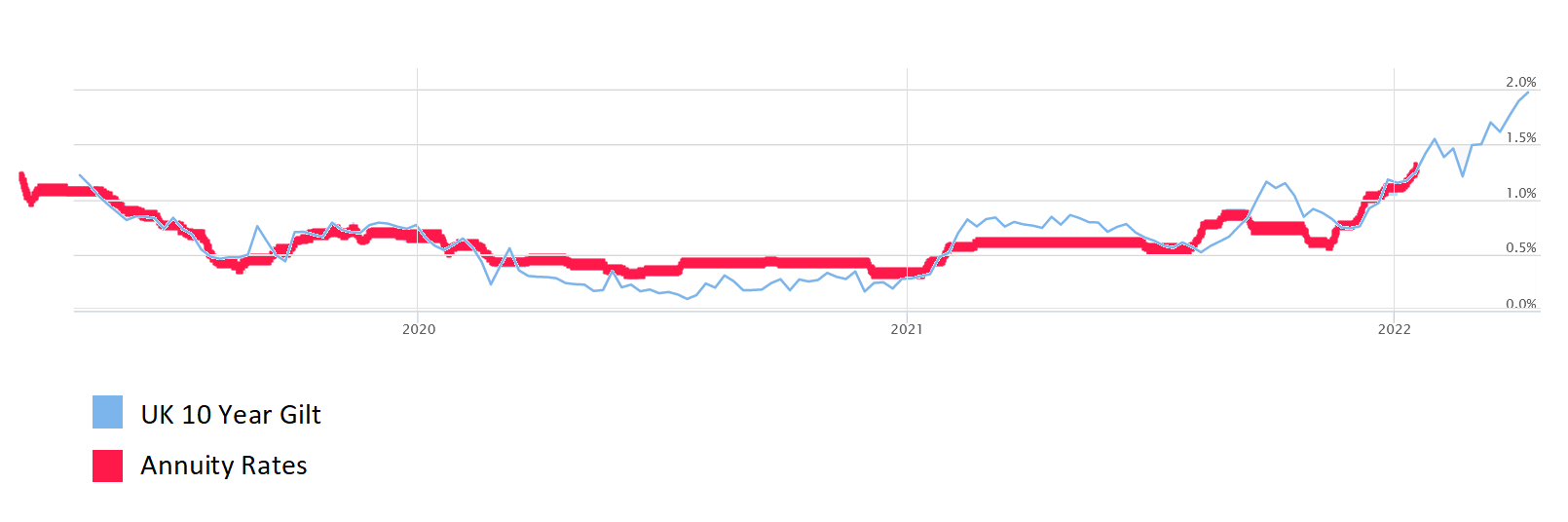

I believe that annuity offers are strongly linked to gilt rates (UK treasuries). Here is a graph of annuity rates overlaid with gilt rates. I have moved the annuities to the left about 3 mths as they take time to catch up.

Gilt rates will rise substantially in the next year (already have, so there is already an inbuilt rise in annuities to come). Annuity rates will rise substantially in the next year.

If you can afford to wait before buying an annuity you should do so.

2 -

Technically no. However, with many S32s there are GARs and GMP that can mean its better to.Jonty6262 said:Do section 32 pension have to be taken as an annuity?I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.1 -

All else being equal, at what rate would a single life, aged 65, RPI annuity become attractive?HL are currently quoting 2.92% on their best buy tables and from the above discussions, we are all assuming that figure will rise so 3% looks a given. We already have a good chunk of DB/SP to come, but if rates get anywhere near 5% by the time I hit 65 I think I'll be seriously considering adding some annuity.The main issue for us is when one partner dies, so maybe waiting until that happens with the surviving partner converting remaining SIPP to an annuity rather than each buying joint life annuities now, especially as our SIPP assets are not evenly balanced so OH does not have assets that can be used to directly purchase an annuity and I would presumably have to pay tax to withdraw from my SIPP for OH to purchase a joint life annuity.I am a Forum Ambassador and I support the Forum Team on the Benefits & tax credits, Heat pumps and Green & Ethical MoneySaving forums. If you need any help on those boards, do let me know. Please note that Ambassadors are not moderators. Any post you spot in breach of the Forum Rules should be reported via the report button, or by emailing forumteam@moneysavingexpert.com. All views are my own & not the official line of Money Saving Expert.0

-

NedS said:All else being equal, at what rate would a single life, aged 65, RPI annuity become attractive?HL are currently quoting 2.92% on their best buy tables and from the above discussions, we are all assuming that figure will rise so 3% looks a given. We already have a good chunk of DB/SP to come, but if rates get anywhere near 5% by the time I hit 65 I think I'll be seriously considering adding some annuity.I would guess 3.5-4%, so you get the same return as the supposed SWR but without the risk of running out of funds before you die.People who are more flexible in their retirement needs might still choose drawdown.N. Hampshire, he/him. Octopus Intelligent Go elec & Tracker gas / Vodafone BB / iD mobile. Kirk Hill Co-op member.Ofgem cap table, Ofgem cap explainer. Economy 7 cap explainer. Gas vs E7 vs peak elec heating costs, Best kettle!

2.72kWp PV facing SSW installed Jan 2012. 11 x 247w panels, 3.6kw inverter. 37 MWh generated, long-term average 2.6 Os.1 -

I wonder if RPI, 50% survivor, age 60 rates will get to 3.5%/4%? Unlikely I assume.0

-

I suppose I was just trying to compare to an "average" final salary pension.michaels said:

And it is easy to argue that even 50% partner benefit is worse than SWR where the partner effectively gets 100%.westv said:I wonder if RPI, 50% survivor, age 60 rates will get to 3.5%/4%? Unlikely I assume.1 -

I am not a believer in the 4% rule. For a 30 year, properly invested SWR, I think 3% is probably OK, but if you want to get closer to the nailed-on safety of an annuity, I would start at 2.5% and review every few years - maybe you can increase to 3% if the first few years weren't a disaster. At age 65, a 30 year time horizon would be fairly safe. Maybe you could start at 3% SWR, though having to cut back would not be out of the question. Therefore, if annuity rate was 3% you might opt for it. Depends on your risk averseness, and your inheritance wishes. With SWR, you keep some risk, but you keep potentially a lot of inheritance.NedS said:All else being equal, at what rate would a single life, aged 65, RPI annuity become attractive?HL are currently quoting 2.92% on their best buy tables and from the above discussions, we are all assuming that figure will rise so 3% looks a given. We already have a good chunk of DB/SP to come, but if rates get anywhere near 5% by the time I hit 65 I think I'll be seriously considering adding some annuity.The main issue for us is when one partner dies, so maybe waiting until that happens with the surviving partner converting remaining SIPP to an annuity rather than each buying joint life annuities now, especially as our SIPP assets are not evenly balanced so OH does not have assets that can be used to directly purchase an annuity and I would presumably have to pay tax to withdraw from my SIPP for OH to purchase a joint life annuity.

So, if you just want to forget about it and sleep at night, 3%. If you have children, and would like to pass on a small fortune in the event you go early, higher than 3%. So, in your case - wanting to protect your spouse, maybe a bit higher than 3%.

Reasons why I don't like the 4% rule:- 4% worked for an optimally invested portfolio - chose the right market and didn't suffer any unfortunate events. We can't all count on being that lucky.

- 4% doesn't account for costs. Even with a great portfolio, the 4% wouldn't actually be achieved because there are always costs.

- Only in recent times have central banks started major QE programs. This really messes with bond prices. Therefore I don't believe that even 100 years of historical data is suitable to back-test the SWR method. This time really is different. Bonds have historically been somewhat uncorrelated with stocks so that the two provide protection for each other. Today, bond returns simply suck, and don't protect against equity downturn. SWR can't be relied upon until QE is over. (Which might only be a year or two...)

- Even though the SWR is successful in 99% of cases, (or 95% or 100%...) there were cases where the pot was grievously diminished during its lifetime, but turned out OK. The retiree would have cut their income in order to protect the pot, even though it turned out to be unnecessary. That case should be regarded as a fail, not a pass.

- Constant SWR is too blunt an instrument for a long retirement. It serves a purpose for planning and estimating, but there must be some willingness to re-evaluate.

- Many people don't have constant income in retirement. They start multiple pensions at different ages. They downsize, or inherit, or do equity release. Therefore a personalised model is needed, as the withdrawal rate will change.

1

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.3K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.9K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605.1K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.9K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards