We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

10k invest all at once or dripfeed?

Comments

-

Notepad_Phil said:

You really don't get it do you. You're not selling and just walking away so you've got a permanent £5,000 loss you're simply selling to free up £10,000, and I really can't see what you mean about getting £5,000 now or a promise to get £5,000.adindas said:

You sold your shares at a loss you lost your money. This is not about probability.

DCA vs Lump sum is about probability, it is not about certainty. So what not to understand here.If you have option get £5,000 now or you are promised to get £5,000 which one you choose ??The same thing with the HF, warren buffet, the traders timing the market is also about the game of probability. In statistics there is also what is so called degree of confidence.

I can't see any substantial difference between someone selling and then immediately buying back (i.e. lump sum investing) from someone who simply keeps their money fully invested - can you? So if you wouldn't sell your portfolio to reinvest via DCA then you can't believe that DCA will on average beat a lump sum.Nonsense illustration. You are asking my DCA. I do sell and buy individual stock using DCA but not using the way like you are suggesting just for the purpose of doing DCA. I post my result on other thread regarding DCA on Scottish Mortgage Trust (SMT) and compare my result with the one who do lump sum. Some people are down 30%+. I am now already in the green territory. SMT is a very volatile stock which could swing -30%, +30% in a matter of weeks.There a more better way of doing DCA than the way you are suggesting. You only sell a few of your position (not all) when they are high, not sell it earning nothing and then you will need to wait another chance to DCA around the dip.Say of you have 100k from the proceed of selling all of your assets (like your suggestion) and immediately buying back using DCA and you only find 10k of bargain for DCA in the market what is the other 90k are doing, doing nothing ?? Also if you have new money from ISA allowance why do you want to sell that stock which is currently keep making money has not reached the peak while you still have cash waiting allocation?? Imo this is naive.I do sell my stocks and do DCA when buying it but only sell it when I am happy with the return and re-enter doing DCA again with another stocks which is selling at a bargain price or dip value (not any stock at any price). I also do buy Cryptos with DCA.But I only buy and start doing DCA for both stocks and cryptos when they are around the bottom. I gauge the bottom using technical analysis using various indicator and charting tools. I am still learning it but I understand how to do the fundamental analysis, how to value a stock and technical analysis. I read this stock market news frequently. So I do DCA but I do not do like the way you suggest as I could find a better way of doing it.For other people who do not want to learn these stuffs they could still do DCA and or enhanced with selective DCA, only drip-feeding during the red days. If you want to discuss about the stock market trend, the fundamental analysis, how to value a stock and technical analysis open a new thread and I will entertain it.Believe what you want to believe like believing that you are better then Warren Buffet as Warren Buffet do time the market.0 -

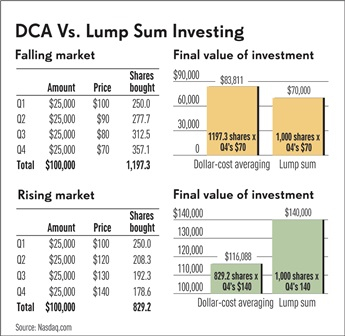

If you are sat with £100k and believe markets will rise over say the next 4 months, then you might immediately invest it all. If you believe the markets will fall over the same period, then you might well invest it all after 4 months.

If you have no idea if the market will rise or fall over the next 4 months, you might use cost averaging over the period.......the latter will ensure you do not suffer the worst outcome possible over those 4 months, but will also ensure you won't get the best possible outcome either.

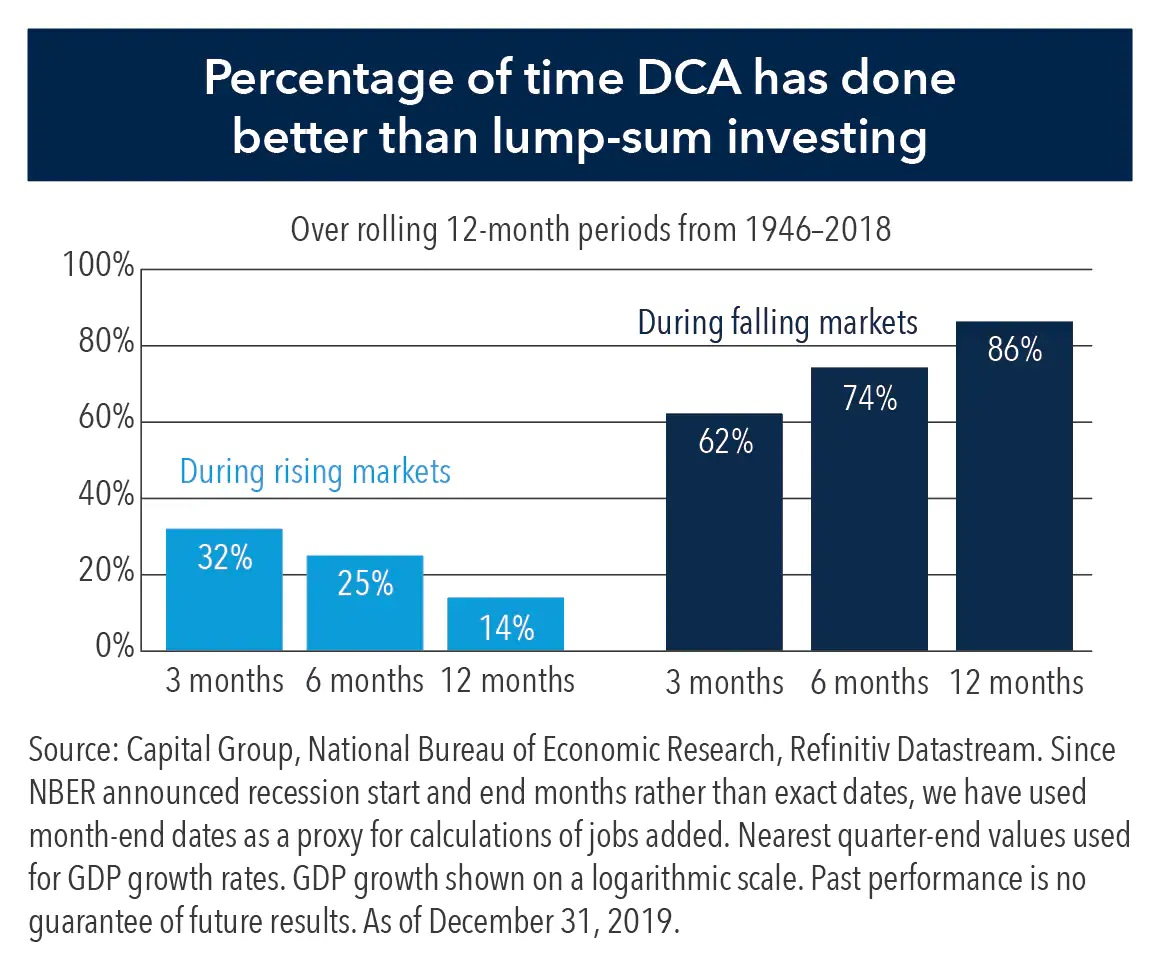

All you can say is that statistically, on average, investing the lump sum immediately has given the better outcome over using cost averaging about 2/3 of the time, but, again on average, that difference is less than 2%.

There are periods though when each approach has outperformed the other by quite a margin (up to 30%).

The crux of the matter is that sat here today, there is no way to know which approach will be better over the next 4 months.....markets rise and fall, but it's not in a straight line.....there is an expectation that markets will rise over the long term, but they are quite unpredictable over the short term.

PS I used 4 months as an example as a common method of cost averaging is 20% in followed by 20% per month for 4 months.......but there's an almost infinite number of combinations you could use.5 -

What do you mean by the particular period of BEAR MARKET and uncertainty?adindas said:@ NedS I am not quite sure what are you trying to show here. Did you compare the result of DCA and lumpsum during the bear market this year?? Did you show statistics proven that Lump sum beat DCA during the particular period of BEAR MARKET and uncertainty ??

@tebbins is Pensioncraft talking about DCA vs Lump-sum during the particular period of BEAR MARKET and uncertainty ?? Is he better than Warren Buffets. and other billionaires investor or strategist frequently aired on CNBC ??

Also the view is assuming there is not any additional trading cost of doing DCA every time you are adding your position which you could easily get it using near zero fees investing platform nowadays. If you use HL for instance of course it does not make sense of doing DCA, as your gain will be wiped by the trading cost £11.95 Per Deal. If you are using zero fee platform and allow fractional share, you could do DCA as low as $10 (or even $1) and it costs you almost nothing.

Here is another expert opinion regarding investing in the bear market which is specifically referring to DCA (e.g drip-feeding)

https://www.investopedia.com/8-ways-to-survive-a-market-downturn-4773417

Are you saying you believe "the" market, if so which, is current at the start/middle/end of a bear market period, or a period of uncertainty as opposed to the previous period of certainty?

PensionCraft is not "better" than Buffett, he simply presents research in that video. Why do you give weight to billionnaires on CNBC before listening to what others have to say? Do you believe credibility or reputation matters more than substance?

Are you ok? You seem to be repeating the same text a lot.1 -

MK62 said:If you are sat with £100k and believe markets will rise over say the next 4 months, then you might immediately invest it all. If you believe the markets will fall over the same period, then you might well invest it all after 4 months.

If you have no idea if the market will rise or fall over the next 4 months, you might use cost averaging over the period.......the latter will ensure you do not suffer the worst outcome possible over those 4 months, but will also ensure you won't get the best possible outcome either.

All you can say is that statistically, on average, investing the lump sum immediately has given the better outcome over using cost averaging about 2/3 of the time, but, again on average, that difference is less than 2%.

There are periods though when each approach has outperformed the other by quite a margin (up to 30%).

The crux of the matter is that sat here today, there is no way to know which approach will be better over the next 4 months.....markets rise and fall, but it's not in a straight line.....there is an expectation that markets will rise over the long term, but they are quite unpredictable over the short term.

PS I used 4 months as an example as a common method of cost averaging is 20% in followed by 20% per month for 4 months.......but there's an almost infinite number of combinations you could use.Despite so strong claims using statistics, surprisingly Noone has ever come up with the link to the statistics that Lump-sum outperform the Dollar Cost Averaging, DCA (e.g., the financial term for drip feeding) under this specific market condition, in the BEAR MARKET WITH A LOT OF FUD. They have been challenged so many times, Noone ever provide that evidence and link to the statistics under the condition mentioned above.

Also many statistics does not take into account that the people who are doing DCA rather than Lump sump safeguard their money into saving account/bonds earning some interest not under the pillow earning nothing. What you are actually doing is that you slowly reducing/rebalancing the bond percentage of your holding and increase equity. You are not out of the market. I am not aware any statistics ever take this into account.

Also, those who said Lump-sum outperform the Dollar Cost Averaging, DCA (e.g., the financial term for drip feeding) in the BEAR MARKET WITH A LOT OF FUD. HAVE YOU EVER TRIED YOURSELF AND COMPARING IT YOURSELF AND SEE THE RESULT??

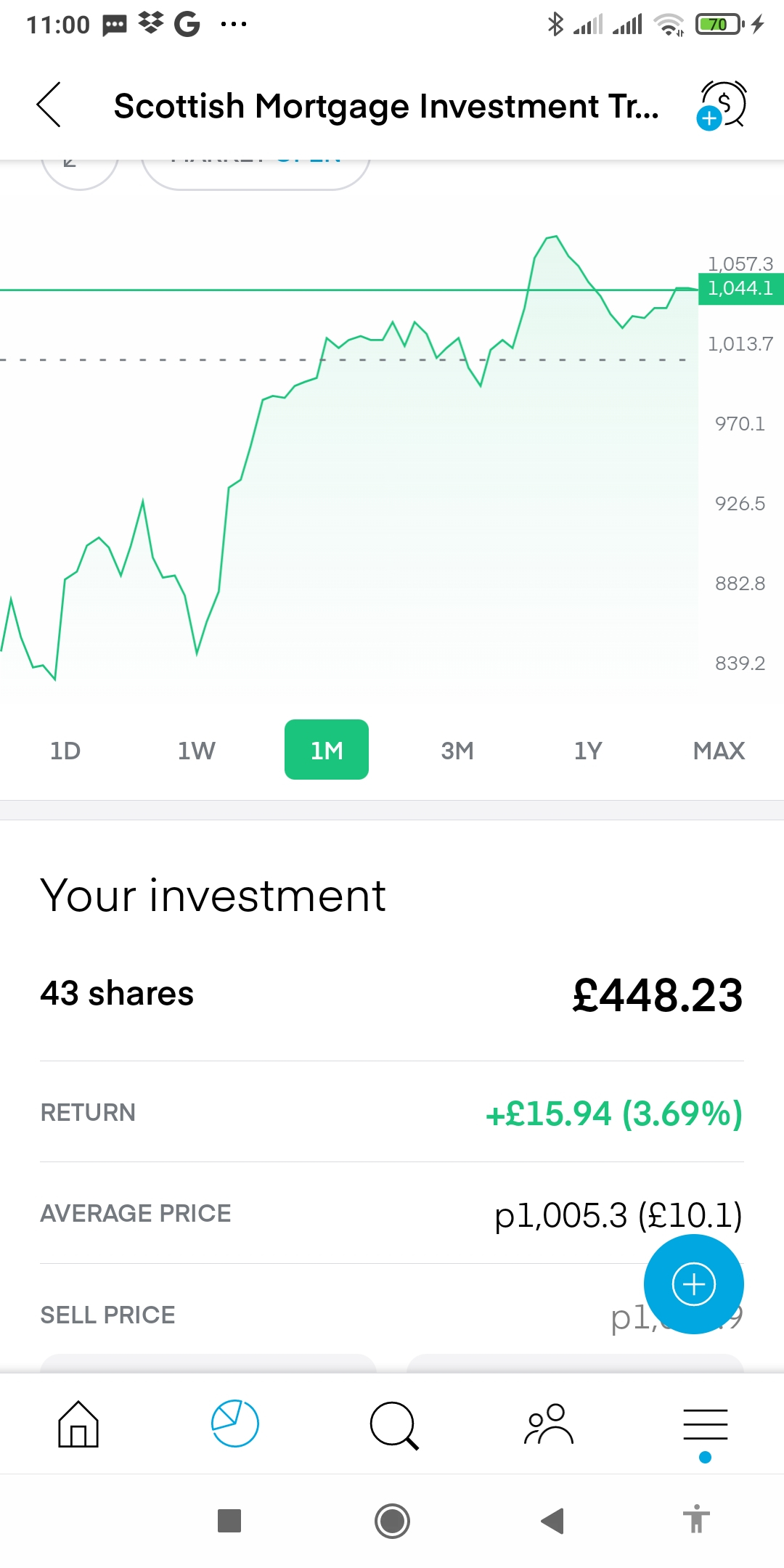

There is nothing certain in investing, it is all about probability. But a strong claim referring to statistics without be able to show the result or tried it yourself and show your result is misleading and making people lost money and cannot sleep well at night. This is especially true if you are investing significant lump sum money in high growth stocks, or a fund/trust containing a lot of high growth stocks such as SMT (Scottish Mortgage Trust). This investment trust is very popular here on MSEs. This one of many examples.

https://forums.moneysavingexpert.com/discussion/6345541/portfolio-question-bg-funds#latest

In the bear Market the stock price, funds tend to move around the channel and suddenly big leg further down consolidation, big leg further down. What you do not want to see is that the lump-sum money you just throw randomly when the price is in the top band of the channel is suddenly swallowed by significant leg down. Consolidation and further leg down. Particularly for fund with a lot of high growth stocks in bear market, throw lump sum randomly and you will soon get nervous when you you see your fund down 30%+

I posted my result using DCA for SMT on another thread, those who do lumpsum during the period of mid-January 2022 to today April 05, 2022, please post your result here and compare it with my result doing DCA on this SMT.

In the Bull market it does not make a lot of difference. In the bull market everyone will make money investing in a well-diversified fund, even a monkey will make money if investing in a well-diversified fund for a long term. In the bear market it makes a difference, especially if you are investing in high growth stocks, a fund containing a lot of high growth stock such as SMT (Scottish Mortgage Trust).

DCA in the bear market is one of the well-known smart strategies recognised by the experts in investing like you see here.

https://www.investopedia.com/8-ways-to-survive-a-market-downturn-4773417

I like to quote what this well-known guy is saying

0 -

I think that quote applies to you @adindas, you keep repeating the same thing, you haven't done any research before asking this question and you have apparently refused to follow any links that have been offered.

What have you been trying to get out of this thread?

If you start DCA at the start of a general fall in the price of what you're buying, obviously you'll do better than lump-sum though measuring that may not be straightforward. Vice versa lump-sum in a rising market.

But:

1. If only the market told you when it was going into a bear market - in which case you would defer buying to the bottom.And2. If only the market would only ever go up or down, instead of wobbling.1 -

tebbins said:I think that quote applies to you @adindas, you keep repeating the same thing, you haven't done any research before asking this question and you have apparently refused to follow any links that have been offered.

What have you been trying to get out of this thread?

If you start DCA at the start of a general fall in the price of what you're buying, obviously you'll do better than lump-sum though measuring that may not be straightforward. Vice versa lump-sum in a rising market.

But:

1. If only the market told you when it was going into a bear market - in which case you would defer buying to the bottom.And2. If only the market would only ever go up or down, instead of wobbling.- I do not ask the question someone ask the question not me.- A few people make a strong claim regarding statistics but have never been able to provide the link to statistics under the specific market condition mentioned above despite have been challenged so many times.- Blind believers, but they have never tried themself the other alternative (have not tried something different) and compare the result.Regarding I do not try something different, I do not do research, well please refer to my posting histories ....It seems this accusation is more applicable to you ??.There is nothing wrong with disagreement but do not accuse people such as people are not do the research people have not tried something else.Also, do not make strong claim to statistics when you can not provide evidence from an authoritative sources as this is misleading people.0 -

tebbins said:

You can't help some people.adindas said:tebbins said:I think that quote applies to you @adindas, you keep repeating the same thing, you haven't done any research before asking this question and you have apparently refused to follow any links that have been offered.

What have you been trying to get out of this thread?

If you start DCA at the start of a general fall in the price of what you're buying, obviously you'll do better than lump-sum though measuring that may not be straightforward. Vice versa lump-sum in a rising market.

But:

1. If only the market told you when it was going into a bear market - in which case you would defer buying to the bottom.And2. If only the market would only ever go up or down, instead of wobbling.- I do not ask the question someone ask the question not me.- A few people make a strong claim regarding statistics but have never been able to provide the link to statistics under the specific market condition mentioned above despite have been challenged so many times.

I have, the PensionCraft video is IMHO a well-presented summary of the research on lump-sum v. drip feed. If you want more information or research, no-one here is under any obligation to argue with you or prove you wrong. I cannot even understand what point you are making in the first place.- Blind believers, but they have never tried themself the other alternative (have not tried something different) and compare the result.

There is plenty of research about this. Please leave any ad hominem or strawmanning out of the forum, please also do not assume what people have or have not done in their investing lifetimes. Not everyone needs torepeat an experiment for it to be proven valid, there is historical data availabe you can use to come ot your own conclusions without having to compare lump-sum v. drip-feed approaches with your own money. The consensus of existing research appears to be that around 2/3 of the time lump sum gives higher returns than drip-feeding, however you may also wish to consider potentially lower volatility, and which route would make you sleep easier and worry less. This topic has already been asked and answered in numerous other threads such as the one linkedby @albemarle's first comment.Regarding I do not try something different, I do not do research, well please refer to my posting histories ....It seems this accusation is more applicable to you ??.

I have not "accused2 you of anything, I have seen no evidence that you have done your own research outside of the rabbit hole you appear to have wandered down. The PensionCraft video I linked is, IMHO a well-presented summary of lump sum v drip feed research and is reasonably unerstandable to a lay audience.There is nothing wrong with disagreement but do not accuse people such as people are not do the research people have not tried something else.

As above.Also, do not make strong claim to statistics when you can not provide evidence from an authoritative sources as this is misleading people.

I already have, I am not an authoriarian, I believe in judging information by its own merits and substance than by the credence or reputation of the person saying it. I am under no obligation, and you not entitled for people in the forum, to do your research for you."I am under no obligation, and you not entitled for people in the forum, to do your research for you."Well, again utterly misleading. I never ask you neither ask people to do research for me, as I have done my own research as well as my own experiment. Have you done your own experiment and compare the result ?? Please quote any of my post where I ask you or people to do the research for me.I challenge the people because they are claiming the research said so in their previous post, e.g to show research which have shown that Lump sum beat DCA in the bear market with a lot of FUD. Surprisingly noone has ever come up with that research result despite such a strong claim in their posts.Regarding Pensioncraft I have replied to you. I herewith re-quote it again.@tebbins is Pensioncraft talking about DCA vs Lump-sum during the particular period of BEAR MARKET and uncertainty ?? Is he better than Warren Buffets. and other billionaires investor or strategist frequently aired on CNBC ??

Also the view is assuming there is not any additional trading cost of doing DCA every time you are adding your position which you could easily get it using near zero fees investing platform nowadays. If you use HL for instance of course it does not make sense of doing DCA, as your gain will be wiped by the trading cost £11.95 Per Deal. If you are using zero fee platform and allow fractional share, you could do DCA as low as $10 (or even $1) and it costs you almost nothing.

Here is another expert opinion regarding investing in the bear market which is specifically referring to DCA (e.g drip-feeding)

https://www.investopedia.com/8-ways-to-survive-a-market-downturn-4773417

Smart Strategies for a Bear Market By The Investopedia Team

0 -

https://www.investors.com/etfs-and-funds/mutual-funds/dollar-cost-averaging-is-good-for-a-falling-market/ Dollar-Cost Averaging Good In A Falling Market

https://www.capitalgroup.com/pcs/insights/articles/benefits-of-dollar-cost-averaging-spring-2020.html A simple approach can help limit the downside during a bear market

https://www.capitalgroup.com/pcs/insights/articles/benefits-of-dollar-cost-averaging-spring-2020.html A simple approach can help limit the downside during a bear markethttps://www.fool.com/investing/stock-market/basics/dollar-cost-averaging/

Generally speaking, dollar-cost averaging works best in bear market and with securities that have dramatic price swings up and down. It is those times, and those types of investments, where reducing investor anxiety and fear of missing out tend to be the most important.

Actually it is very easy to see it does not need a research to know that during the particular period of the bear market (falling market) DCA (Drip feeding) will outperform lump Sum as the the price will fall more than it rises. Most research showing the Lump-sum beat DCA are looking into the bull market and long term period not particularly focus on the bear /falling market.In the long run the market will always go up. People could improve the result by adapting strategy switching from one side to another according to environment. It is very easy to know where we are on the bear market or not b reading the news.https://www.barrons.com/articles/stocks-bear-market-51645814386

We are currency in the bear market, More than 75% of stocks in the Nasdaq Composite Index and 51% of S&P 500 stocks are already in a bear market—down more than 20% from peak prices, The outlook is worsening with geopolitical risks exacerbating potential for inflation, higher commodity prices, and “shocks” to growth.

0 -

But surely lump sum at the end of a period will beat drip feeding in a falling market?

0 -

Well that depends on what the curve between entering and ending the bear market looks like, but yes in most cases that's probably true.InvesterJones said:But surely lump sum at the end of a period will beat drip feeding in a falling market?But I'm sure anyone who can tell that we're about to enter a bear market or are leaving a bear market will have much better ways to make their money than simple regular investing and lump summing.0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards