We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

New finance denied, questions

Chrisr3521

Posts: 4 Newbie

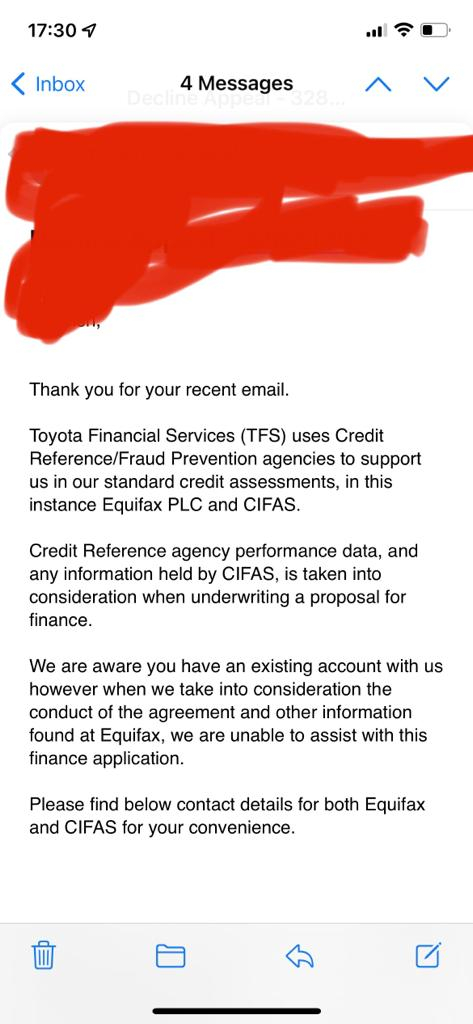

We applied for finance with Toyota for a new car, bear in mind we already have finance with them and have over the last five years renewing for another 5 years a year ago and my credit rating haven't changed over the last 2 years, they declined us, after pressing them on why they sent an email (attached) obviously we know what the info on Equifax is but they also mention the conduct of the current agreement? Could anyone shed any light on what this means?

Thanks

Thanks

0

Comments

-

It's a generic answer that means you haven't met their criteria. It doesn't mean you've necessarily mismanaged your current agreement.

Check your files to see what they show. Your credit rating isn't a reflection of your risk.0 -

As above, the response seems very generic and "catch-all" on behalf of Toyota.

Out if interest, have you maintained all payments on the current agreement in full and on time?

Are you sure there is not an admin error that means every payment has been recorded late? For example, payment due 3rd of every month and you actually made every payment on the 4th each month?

Did you need to take any payment holidays for any reason, such as COVID period? Although these might have been agreed at the time and "without penalty" on the current borrowing, the lender can assess such factors in their willingness for future borrowing.

Review all your credit files for any data errors that would negatively impact a lender's decision.Chrisr3521 said:We applied for finance with Toyota for a new car, bear in mind we already have finance with them and have over the last five years renewing for another 5 years a year ago and my credit rating haven't changed over the last 2 years, they declined us, after pressing them on why they sent an email (attached) obviously we know what the info on Equifax is but they also mention the conduct of the current agreement? Could anyone shed any light on what this means?

Thanks

0 -

No payments have been late missed or taken a holiday, new credit agreement only last year and that car was going to be traded in against the new one and the existing loan settled.0

-

You are 1 year into a 5-year term for a car, say £20k outstanding finance.

That loan has been correctly managed and all payments in full and on time.

You plan to sell that car and clear the finance.

You plan buy a new car with another loan over 5-years, say £25k.

Is it possible that Toyota have assessed your application on the basis of the current loan (say £20k) plus the new loan (say £25k) in addition? That would mean total borrowing at a much higher level (say £45k) and would affect the affordability calculation.0 -

If the OP has had the finance proposed via a Toyota dealership, which is likely as it appears the OP is looking to purchase a brand new car, the proposal terms may have been presented with a contra settlement or without, only the person completing the proposal will know this (sales executive/manager for example). The existing agreement number with a finance settlement and part exchange value should have formed part of the proposal thus eliminating the above possibility.Grumpy_chap said:You are 1 year into a 5-year term for a car, say £20k outstanding finance.

That loan has been correctly managed and all payments in full and on time.

You plan to sell that car and clear the finance.

You plan buy a new car with another loan over 5-years, say £25k.

Is it possible that Toyota have assessed your application on the basis of the current loan (say £20k) plus the new loan (say £25k) in addition? That would mean total borrowing at a much higher level (say £45k) and would affect the affordability calculation.

Lenders are increasingly tightening their belts and criteria, it may simply be a matter of affordability.As mentioned above, scrutinise your credit reports and ensure that all data held is true and correct.

You will not get any further information with greater detail out of them Im afraid.If you believe you can, you will. If you believe you can't, you won't.

Secured/Unsecured loans x 1

Credit Cards x 8 (total limit £55,050)

Creation FS Retail Account x 1

Creation Credit Sale 0% x 1 = £112.50pm x 20 mths

0% Overdraft x 1 (£0 / £250)

Mortgage Outstanding - £137,707.00 (Payment 13/360)

Total Debt = £7,400 (0%APR) @ £100pm - Stoozing0 -

That said, it is not entirely clear as to whether the OP is part exchanging or buying a second car in addition to.If you believe you can, you will. If you believe you can't, you won't.

Secured/Unsecured loans x 1

Credit Cards x 8 (total limit £55,050)

Creation FS Retail Account x 1

Creation Credit Sale 0% x 1 = £112.50pm x 20 mths

0% Overdraft x 1 (£0 / £250)

Mortgage Outstanding - £137,707.00 (Payment 13/360)

Total Debt = £7,400 (0%APR) @ £100pm - Stoozing0 -

Its a possibility I suppose.Grumpy_chap said:You are 1 year into a 5-year term for a car, say £20k outstanding finance.

That loan has been correctly managed and all payments in full and on time.

You plan to sell that car and clear the finance.

You plan buy a new car with another loan over 5-years, say £25k.

Is it possible that Toyota have assessed your application on the basis of the current loan (say £20k) plus the new loan (say £25k) in addition? That would mean total borrowing at a much higher level (say £45k) and would affect the affordability calculation.0 -

Part exchanging existing against a new car, as works out cheaper than the equivelent used.MrFrugalFever said:That said, it is not entirely clear as to whether the OP is part exchanging or buying a second car in addition to.0 -

Have you appealed the decision with the dealership, they will likely have a finance agent to support them with individual cases.If you believe you can, you will. If you believe you can't, you won't.

Secured/Unsecured loans x 1

Credit Cards x 8 (total limit £55,050)

Creation FS Retail Account x 1

Creation Credit Sale 0% x 1 = £112.50pm x 20 mths

0% Overdraft x 1 (£0 / £250)

Mortgage Outstanding - £137,707.00 (Payment 13/360)

Total Debt = £7,400 (0%APR) @ £100pm - Stoozing0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.2K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247.2K Work, Benefits & Business

- 603.8K Mortgages, Homes & Bills

- 178.4K Life & Family

- 261.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards