We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Upside Gains vs Downside Protection

Comments

-

I understand that.dunstonh said:Anything you put in for downside protection will be a drag in positive periods but not in negative periods.

You have downside protection to keep the volatility within you acceptable limits and capacity for loss. You dont have downside protection in there to improve investment returns.0 -

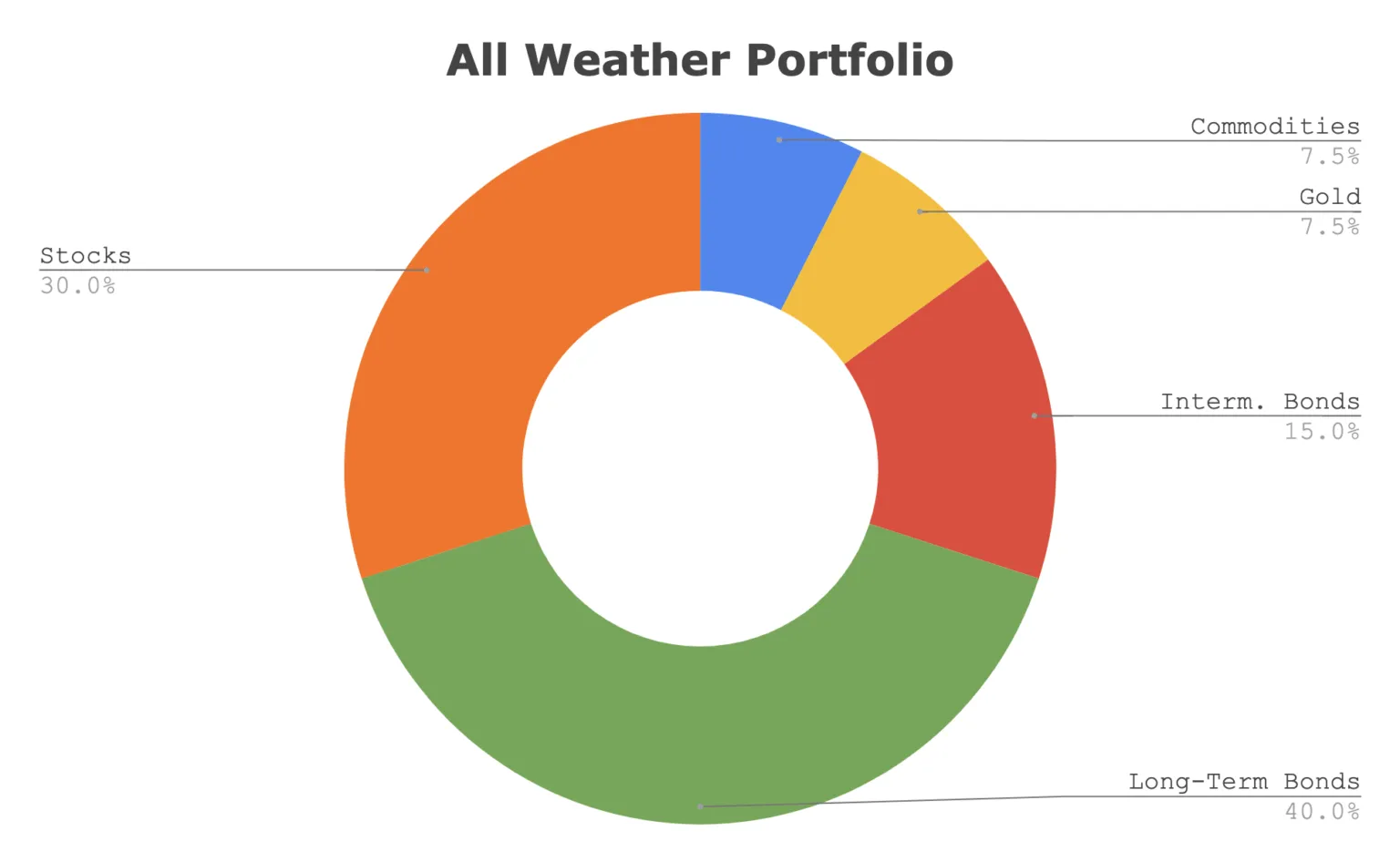

chiang_mai said:Half my portfolio is split between RICA, PNL and CGT. Another 25% is in Cash and the last 25% is split between MWY, FSSA Asia Focus and BG Int. That combination should, on a historical basis, achieve around 12% per year but also provide significant downside protection. I'm currently down 3.1% YTD but up 6.5% over one year. I'll allocate most of the remaining Cash as soon as the time seems right. A couple of friends are big BG fanatics, one holds nearly all the big BG funds but is down 28% over one year and holds no downside protection whatsoever. We constantly debate whether 60/40 is dead and the 40 is merely a drag on the 60, I think it is but that's the price to be paid for protecting the downside, I'm holding only 40% equities! I think they're hairy chest types who don't understand what they've invested in. They think I'm foolish for holding so few equities, we're all in our mid/late 60's and the money involved is not central to our well being. I also think many have unrealistic expectations of what is a reasonable gain each year. What do you think?Have you thought about hedging it ??For instance protection against inflation is to have some gold in your portfolio. Unless you have done that since November/Dec last year, but it is too late now as the price of gold have shooting up.The other strategy is going "short".There are various variations such as put option, short ETP, or the easiest one is to buy and inverse ETFs., it could be leveraged or unleveraged.If you "strongly believe" that your current high growth stocks or ETFs position will be going down much further from here you could for instance hedge by opening SQQQ (ProShares UltraPro Short QQQ ETF) a 3X Short QQQ Inverse ETFSimilarly to S&P500, by openingg SPXU (ProShares UltraPro Short S&P500) Inverse ETF this is a 3X Short S&P 500Just need to make sure that you understand about the risk and how the short, put option, Short ETP, Inverse inverse ETF work.Hedging and short will limit your damage when your current portfolio going south but it will also limit your profit when the stock market is going up.The long term solution is by composing an all weather, weather proof portfolio. such as Ray Dalio all weather portfolio.

Doing hedging, going short right now will only make sense and make profit if the current market have more in the downside compared to the upside. I personally believe that market especially high growth stock is already very close to the bottom and due for reversal. This is also the views of many wall-street strategists / analysts if you regularly watch the stock market news.The high growth stock even the very good one has been battered recently going down 50% or even more as 70%+. The downside is 30%, the upside is 100%+ which one is bigger ??. Let alone many of these high growth stocks are highly unlike to go bankrupt as they do not have comparable substitute.0

Doing hedging, going short right now will only make sense and make profit if the current market have more in the downside compared to the upside. I personally believe that market especially high growth stock is already very close to the bottom and due for reversal. This is also the views of many wall-street strategists / analysts if you regularly watch the stock market news.The high growth stock even the very good one has been battered recently going down 50% or even more as 70%+. The downside is 30%, the upside is 100%+ which one is bigger ??. Let alone many of these high growth stocks are highly unlike to go bankrupt as they do not have comparable substitute.0 -

Always buy the underlying investments not the fund manager. Perpertual were in a similar position 20 years ago.chiang_mai said:A couple of friends are big BG fanatics, one holds nearly all the big BG funds but is down 28% over one year and holds no downside protection whatsoever. We constantly debate whether 60/40 is dead and the 40 is merely a drag on the 60,

60/40 is merely taking a backseat. Trades are cyclical and the wind has most certainly changed direction. Be back in favour by the end of the coming decade. Invest for tomorrow on the basis of what's known today.1 -

I am very comfortable with my holdings and plan to do almost nothing with them, apart perhaps from scaling up. The point of the discussion, as outlined in the original post, is about the degree of risk a person at or beyond retirement age should take.adindas said:chiang_mai said:Half my portfolio is split between RICA, PNL and CGT. Another 25% is in Cash and the last 25% is split between MWY, FSSA Asia Focus and BG Int. That combination should, on a historical basis, achieve around 12% per year but also provide significant downside protection. I'm currently down 3.1% YTD but up 6.5% over one year. I'll allocate most of the remaining Cash as soon as the time seems right. A couple of friends are big BG fanatics, one holds nearly all the big BG funds but is down 28% over one year and holds no downside protection whatsoever. We constantly debate whether 60/40 is dead and the 40 is merely a drag on the 60, I think it is but that's the price to be paid for protecting the downside, I'm holding only 40% equities! I think they're hairy chest types who don't understand what they've invested in. They think I'm foolish for holding so few equities, we're all in our mid/late 60's and the money involved is not central to our well being. I also think many have unrealistic expectations of what is a reasonable gain each year. What do you think?Have you thought about hedging it ??For instance protection against inflation is to have some gold in your portfolio. Unless you have done that since November/Dec last year, but it is too late now as the price of gold have shooting up.The other strategy is going "short".There are various variations such as put option, short ETP, or the easiest one is to buy and inverse ETFs., it could be leveraged or unleveraged.If you "strongly believe" that your current high growth stocks or ETFs position will be going down much further from here you could for instance hedge by opening SQQQ (ProShares UltraPro Short QQQ ETF) a 3X Short QQQ Inverse ETFSimilarly to S&P500, by openingg SPXU (ProShares UltraPro Short S&P500) Inverse ETF this is a 3X Short S&P 500Just need to make sure that you understand about the risk and how the short, put option, Short ETP, Inverse inverse ETF work.Hedging and short will limit your damage when your current portfolio going south but it will also limit your profit when the stock market is going up.The long term solution is by composing an all weather, weather proof portfolio. such as Ray Dalio all weather portfolio.Doing hedging, going short right now will only make sense and make profit if the current market have more in the downside compared to the upside. I personally believe that market especially high growth stock is already very close to the bottom and due for reversal. This is also the views of many wall-street strategists / analysts if you regularly watch the stock market news.The high growth stock even the very good one has been battered recently going down 50% or even more as 70%+. The downside is 30%, the upside is 100%+ which one is bigger ??. Let alone many of these high growth stocks are highly unlike to go bankrupt as they do not have comparable substitute.1 -

chiang_mai said:masonic said:chiang_mai said:

Which begets the questions: how long is the longer term and how long can it possibly be to a 69 year old male.masonic said:I don't think 12% per year is a realistic expectation going forward, even with inflation where it is. Risk tolerance is a personal matter, if downside protection is important to you then some element of bonds in your portfolio is going to be unavoidable (since the defensive trusts you mention all hold a generous allocation of bonds, that should tell you they still have a place in a defensive portfolio). Many threads discuss the search for an alternative and none have yet come up with anything viable to eschew bonds completely. There is nothing wrong with your friends going anywhere up to 100% equities if they are in it for the long term and like you it is money they don't need to meet their basic needs. Chances are that will deliver the highest returns over the long term, but they could see some heavy losses over the short term. BG was positioned perfectly for the economic conditions of the recent past, but they may not fare as well in the future.A healthy, happy, 69 year old male with parents who survived past 75 years old would have a life expectancy into their 90s. That's over 20 years, which certainly qualifies as long term. If the assets are left in a will, then they might be held for even longer.If they have already held the investments for a few years, then they'd have had enough of a head start that even a moderate loss in the short term would likely leave them better off than someone who had invested cautiously throughout.

Every piece of investment advice I have ever read suggests that people approaching retirement age should begin to de-risk and tone down their investments, advice which doesn't seem unreasonable at all. Cautious investing for younger/middle-aged investors is all fine and good if that's a person's risk appetite, if it's not, by all means, put on the hairy chest shirt. I think the rule of thumb changes once past 65/70, even if in theory that person could theoretically live for a further 20 years. But OK, you're clearly from the 100% school of equity investing and I respect your views on the subject, I'll be interested to learn what others have to say on the subject.I had just assumed that such advice pre-dates UK pension market freedoms from a time where pensioners had no choice but to cash in their pot and purchase an annuity, so it was advisable for one to de-risk as retirement approaches to maintain the (annuity) purchasing power of the pot.With pension freedoms, and a currently more common drawdown scenario, I envisage one making little change to investment strategy at or around retirement age. As others have pointed out, a retiree hopefully still has a 20-30 year time horizon so I would consider it reasonable for them to stay invested at a risk level appropriate for them and to drawdown on their investments over the course of their retirement.Maybe my assumptions are completely wrong?

Our green credentials: 12kW Samsung ASHP for heating, 7.2kWp Solar (South facing), Tesla Powerwall 3 (13.5kWh), Net exporter1 -

I would say it depends on the starting point. I have been invested between 80% and 100% equities for the last 25 years but as I get closer to retirement and drawing on those investments I will be reducing that expose somewhat. Not because my attitude to risk has changed - I am still invested in some high growth private equity and lots of small company exposure. Its because I cannot afford to take those risks while being in drawdown. So more cash, bonds and property is required.NedS said:chiang_mai said:masonic said:chiang_mai said:

Which begets the questions: how long is the longer term and how long can it possibly be to a 69 year old male.masonic said:I don't think 12% per year is a realistic expectation going forward, even with inflation where it is. Risk tolerance is a personal matter, if downside protection is important to you then some element of bonds in your portfolio is going to be unavoidable (since the defensive trusts you mention all hold a generous allocation of bonds, that should tell you they still have a place in a defensive portfolio). Many threads discuss the search for an alternative and none have yet come up with anything viable to eschew bonds completely. There is nothing wrong with your friends going anywhere up to 100% equities if they are in it for the long term and like you it is money they don't need to meet their basic needs. Chances are that will deliver the highest returns over the long term, but they could see some heavy losses over the short term. BG was positioned perfectly for the economic conditions of the recent past, but they may not fare as well in the future.A healthy, happy, 69 year old male with parents who survived past 75 years old would have a life expectancy into their 90s. That's over 20 years, which certainly qualifies as long term. If the assets are left in a will, then they might be held for even longer.If they have already held the investments for a few years, then they'd have had enough of a head start that even a moderate loss in the short term would likely leave them better off than someone who had invested cautiously throughout.

Every piece of investment advice I have ever read suggests that people approaching retirement age should begin to de-risk and tone down their investments, advice which doesn't seem unreasonable at all. Cautious investing for younger/middle-aged investors is all fine and good if that's a person's risk appetite, if it's not, by all means, put on the hairy chest shirt. I think the rule of thumb changes once past 65/70, even if in theory that person could theoretically live for a further 20 years. But OK, you're clearly from the 100% school of equity investing and I respect your views on the subject, I'll be interested to learn what others have to say on the subject.I had just assumed that such advice pre-dates UK pension market freedoms from a time where pensioners had no choice but to cash in their pot and purchase an annuity, so it was advisable for one to de-risk as retirement approaches to maintain the (annuity) purchasing power of the pot.With pension freedoms, and a currently more common drawdown scenario, I envisage one making little change to investment strategy at or around retirement age. As others have pointed out, a retiree hopefully still has a 20-30 year time horizon so I would consider it reasonable for them to stay invested at a risk level appropriate for them and to drawdown on their investments over the course of their retirement.Maybe my assumptions are completely wrong?2 -

I haven't been in the UK for over 20 years, most if not all of my input regarding investing comes from the US or Asia and from other ex-pat friends. It may well be the case that UK market freedoms allow pensioner investors to do as you say, I/we however have to look at what makes sense for us to do rather than what government allows or requires us to do. With those things in mind.....I have a financial services/risk/consulting background plus I am risk-averse. It does not make sense to me that a person would work all their life to acquire wealth and then in the final 10% of their life, risk losing a substantial portion of that wealth, simply because they didn't modify their approach.NedS said:chiang_mai said:masonic said:chiang_mai said:

Which begets the questions: how long is the longer term and how long can it possibly be to a 69 year old male.masonic said:I don't think 12% per year is a realistic expectation going forward, even with inflation where it is. Risk tolerance is a personal matter, if downside protection is important to you then some element of bonds in your portfolio is going to be unavoidable (since the defensive trusts you mention all hold a generous allocation of bonds, that should tell you they still have a place in a defensive portfolio). Many threads discuss the search for an alternative and none have yet come up with anything viable to eschew bonds completely. There is nothing wrong with your friends going anywhere up to 100% equities if they are in it for the long term and like you it is money they don't need to meet their basic needs. Chances are that will deliver the highest returns over the long term, but they could see some heavy losses over the short term. BG was positioned perfectly for the economic conditions of the recent past, but they may not fare as well in the future.A healthy, happy, 69 year old male with parents who survived past 75 years old would have a life expectancy into their 90s. That's over 20 years, which certainly qualifies as long term. If the assets are left in a will, then they might be held for even longer.If they have already held the investments for a few years, then they'd have had enough of a head start that even a moderate loss in the short term would likely leave them better off than someone who had invested cautiously throughout.

Every piece of investment advice I have ever read suggests that people approaching retirement age should begin to de-risk and tone down their investments, advice which doesn't seem unreasonable at all. Cautious investing for younger/middle-aged investors is all fine and good if that's a person's risk appetite, if it's not, by all means, put on the hairy chest shirt. I think the rule of thumb changes once past 65/70, even if in theory that person could theoretically live for a further 20 years. But OK, you're clearly from the 100% school of equity investing and I respect your views on the subject, I'll be interested to learn what others have to say on the subject.I had just assumed that such advice pre-dates UK pension market freedoms from a time where pensioners had no choice but to cash in their pot and purchase an annuity, so it was advisable for one to de-risk as retirement approaches to maintain the (annuity) purchasing power of the pot.With pension freedoms, and a currently more common drawdown scenario, I envisage one making little change to investment strategy at or around retirement age. As others have pointed out, a retiree hopefully still has a 20-30 year time horizon so I would consider it reasonable for them to stay invested at a risk level appropriate for them and to drawdown on their investments over the course of their retirement.Maybe my assumptions are completely wrong?

If I was a younger man who had more time to recover lost investment money, I would happily be 100% in equities. But 20 years on from age 50 it doesn't make sense to me. The writing has been on the wall for many months regarding the many negative factors that will impact investment returns. Advancing years aside, the economic and geopolitical circumstances currently are flashing red warning signs and have been for months, yet another set of reasons why I think risk reduction is appropriate. But that's just me, other people with different risk appetites and of different ages will see the world differently.1 -

Annuities would still be the preferred option for many given the choice. The GFC and subsequent events changed the game. The whistle appears to have blown though. New game is in play. Likely to catch many unaware. As those with endowment policies found to their cost investment returns can indeed disappoint.NedS said:chiang_mai said:masonic said:chiang_mai said:

Which begets the questions: how long is the longer term and how long can it possibly be to a 69 year old male.masonic said:I don't think 12% per year is a realistic expectation going forward, even with inflation where it is. Risk tolerance is a personal matter, if downside protection is important to you then some element of bonds in your portfolio is going to be unavoidable (since the defensive trusts you mention all hold a generous allocation of bonds, that should tell you they still have a place in a defensive portfolio). Many threads discuss the search for an alternative and none have yet come up with anything viable to eschew bonds completely. There is nothing wrong with your friends going anywhere up to 100% equities if they are in it for the long term and like you it is money they don't need to meet their basic needs. Chances are that will deliver the highest returns over the long term, but they could see some heavy losses over the short term. BG was positioned perfectly for the economic conditions of the recent past, but they may not fare as well in the future.A healthy, happy, 69 year old male with parents who survived past 75 years old would have a life expectancy into their 90s. That's over 20 years, which certainly qualifies as long term. If the assets are left in a will, then they might be held for even longer.If they have already held the investments for a few years, then they'd have had enough of a head start that even a moderate loss in the short term would likely leave them better off than someone who had invested cautiously throughout.

Every piece of investment advice I have ever read suggests that people approaching retirement age should begin to de-risk and tone down their investments, advice which doesn't seem unreasonable at all. Cautious investing for younger/middle-aged investors is all fine and good if that's a person's risk appetite, if it's not, by all means, put on the hairy chest shirt. I think the rule of thumb changes once past 65/70, even if in theory that person could theoretically live for a further 20 years. But OK, you're clearly from the 100% school of equity investing and I respect your views on the subject, I'll be interested to learn what others have to say on the subject.I had just assumed that such advice pre-dates UK pension market freedoms from a time where pensioners had no choice but to cash in their pot and purchase an annuity, so it was advisable for one to de-risk as retirement approaches to maintain the (annuity) purchasing power of the pot.1 -

That's quite accurate insight. I really like the information shared here.

-2 -

chiang_mai said:One last thought: which of us doesn't buy insurance of some sort in our daily lives, it seems odd that people would buy life insurance etc but not buy similar when investing.If I die and my spouse waits an indeterminate period of 5-10 years, I'm not going to come back to life.Most investors do have downside protection in the sense of 1) alternative asset classes to reduce volatility and 2) a cash emergency fund to ensure that it's unlikely they'll need to cash in investments during a downturn. Gung-ho DIY investors who go 100% equities are in a minority.Most investors hold any or all of 1) workplace pension default funds 2) Vanguard Lifestrategy type "60/40" funds 3) risk-targeted portfolios designed by advisers or the likes of Nutmeg 4) DIY portfolios with some downside protection.It does not make sense to me that a person would work all their life to acquire wealth and then in the final 10% of their life, risk losing a substantial portion of that wealth, simply because they didn't modify their approach.The final 10% of life for the typical investor is 80-90, possibly older.If your heirs are of a similar mindset to you, and are likely to leave any inherited funds invested, you are not necessarily running any more risk of loss than you were at 60. If your invested assets fall by 20% or 40% just before death you don't fall down the high score table.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 353.7K Banking & Borrowing

- 254.2K Reduce Debt & Boost Income

- 455.1K Spending & Discounts

- 246.8K Work, Benefits & Business

- 603.2K Mortgages, Homes & Bills

- 178.2K Life & Family

- 260.8K Travel & Transport

- 1.5M Hobbies & Leisure

- 16K Discuss & Feedback

- 37.7K Read-Only Boards