We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

Sensible low risk investment

Comments

-

apb123 said:

Never try to beat the market or time the market. No one can do this. The trick is to try and track the market.Time in the market vs timing the market hearsay was introduced a long time ago so it might not be accurate in the modern environment. With the proliferation of zero or near zero fees platform, there are more retailer investors do beat the market by timing the market. But certainly you are right if you said noone could do that in perfection. But keep in mind you just need to get 50%+ right to get a better result than another alternative.

In the modern environment news are available in real time; there are a lot of analytical tools, probabilistic models , have been developed. People like the active hedge fund managers, active traders, the robots do time the market on almost every single trading day. But they normally trade individual stocks rather than a very well diversified funds. They could comfortably do that because they understand the market behaviors, they have analytical tools that allow them to perform technical analysis such as price/volume action and fundamental analysis. Also because they know how to value the stocks so they know it when a stock is selling at a discount. Without knowing these, it is literary just gambling. So definitely, not the cup of tea of many investors.

In our real life, when we could play a waiting game we like to buy stuffs when we believe they are selling at a discount and not blindly buying it at any time at any price just because we have money ready to invest.

jake_jones99 said:It depends on the strategy. FTSE 100 represents a snapshot of the heavy lifters in the UK economy. They were hit badly because of the loss in investor confidence due to COVID. My prediction, which I found very likely and it actually happened, was that the economy was going to recover. It always does. I invested because I understood that the drop in FTSE 100 was simply due to human fear against something they did not fully understand. After the index reached ~7000 I backed off because my horizon of predictability had gone to 0. Yes, I read even before embarking on this journey that you should not time the market. Still I did it and I don't regret one bit. Because I am also able to admit when I have no idea what's gonna happen next, such as now, and thus I stay away from it.It is good to learn from people but people do what they believe it is good and true for them. It is your own money you are investing.

0 -

masonic said:jake_jones99 said:What do you guys think of investing in inflation linked bonds? I am thinking of this for the chunk of my savings that I would need inflation protection for. Either purchasing a govt bond, or investing in an ETF tracker:

https://www.ishares.com/uk/individual/en/products/251717/ishares-indexlinked-gilts-ucits-etf?switchLocale=y&siteEntryPassthrough=trueDo you understand index linked gilts, their volatility and loss potential, and prospects (including potential impact of the forthcoming change of inflation measure)? There was a thread a few months ago about someone who bought a gilt ETF and went through some clear emotional distress when it fell 6+% without warning over a few weeks, when the loss potential is ~10%, so well within the expected range.Index linked gilts return inflation minus 2-4% depending on their duration. They will not keep up with inflation. Inflation being RPI for the rest of this decade, then CPI. Buying an individual bond with appropriate duration and holding to maturity will lock in this return, otherwise you'll be at the mercy of the bond markets, where prices are likely to fall if interest rates rise. A series of fixed term savings accounts could conceivably beat the return from index linked bonds over the next 10 years. Trading individual bonds is not a mainstream activity, some brokers will allow you to trade them (often only by telephone), some won't offer them at all. It is not a particularly liquid market.

This is the variation of the gilt I posted from the date of the post until now. I have to say, I am glad I didn't invest a penny in it, I would have been 25% worse off. The idea that they change with inflation seems indeed a red herring.1 -

Anyone who believes that the price of inflation linked bonds does or should follow inflation does not understand them. Inflation matching only occurs on maturity. In the meantime the price is set by the market where the likely returns of inflation linked bonds are assessed against those offered by other, mainly fixed, bonds.jake_jones99 said:masonic said:jake_jones99 said:What do you guys think of investing in inflation linked bonds? I am thinking of this for the chunk of my savings that I would need inflation protection for. Either purchasing a govt bond, or investing in an ETF tracker:

https://www.ishares.com/uk/individual/en/products/251717/ishares-indexlinked-gilts-ucits-etf?switchLocale=y&siteEntryPassthrough=trueDo you understand index linked gilts, their volatility and loss potential, and prospects (including potential impact of the forthcoming change of inflation measure)? There was a thread a few months ago about someone who bought a gilt ETF and went through some clear emotional distress when it fell 6+% without warning over a few weeks, when the loss potential is ~10%, so well within the expected range.Index linked gilts return inflation minus 2-4% depending on their duration. They will not keep up with inflation. Inflation being RPI for the rest of this decade, then CPI. Buying an individual bond with appropriate duration and holding to maturity will lock in this return, otherwise you'll be at the mercy of the bond markets, where prices are likely to fall if interest rates rise. A series of fixed term savings accounts could conceivably beat the return from index linked bonds over the next 10 years. Trading individual bonds is not a mainstream activity, some brokers will allow you to trade them (often only by telephone), some won't offer them at all. It is not a particularly liquid market.

This is the variation of the gilt I posted from the date of the post until now. I have to say, I am glad I didn't invest a penny in it, I would have been 25% worse off. The idea that they change with inflation seems indeed a red herring.3 -

There is too much agreement in this thread, so I’m going to play Devil’s (or FTSE 100’s) advocate.

Reading through the thread I’ve identified the following, let’s call them anti-FTSE 100/pro-global points. and provided some counters. I don’t agree with or believe in all these points, nor am I asserting anything, just trying to present some different points of view. Some of them are even contradictory such as 4 and 6. For every point you could infer from data in economics and investing, there will always be at least 2 at least equally credible counters.

1. Dinosaur / dying / yesteryear industries

Longevity can be good too (https://hbr.org/2016/12/the-scary-truth-about-corporate-survival, https://research-doc.credit-suisse.com/docView?language=ENG&format=PDF&sourceid=csplusresearchcp&document_id=1070991801&serialid=0xhJ7ymG%2BLuZxZzmUHitAOqfIGpMxjfNOq%2FHpp%2FK2LU%3D&cspId=null)

However turnover in “younger” indices relates more to M&A activity (cosmetic change in the index) than “innovation” (substantive change in economic activity, indicative of real growth). The former has little to no net benefit for index-shareholders as “synergies” often fail to materialise but significant legal, consulting and integration costs can be incurred, so M&A can be a form of value extraction rather than value addition (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2993933) that can grow a company’s size past an efficiently manageable point (Slow Finance by Gervais Williams, Chapter 7), unless as with the FTSE 250, most of the acquirers are external buyers (https://research.ftserussell.com/products/downloads/ftse_250_constituent_history.pdf).

Also, the less-favoured sectors can be cyclically or temporarily out of favour without becoming permanently redundant.

2. Sector weightings

ICB Sector as at 29 April 2022

FTSE 100

+/-

FTSE All-World

Tech

0.96%

-20.91%

21.87%

Telecoms

2.33%

-0.77%

3.10%

Healthcare

13.65%

1.76%

11.89%

Banks

9.25%

2.15%

7.10%

Financial services

4.33%

0.03%

4.30%

Insurance

3.45%

0.33%

3.12%

Real estate

1.57%

-1.48%

3.05%

Cars and parts

0%

-2.96%

2.96%

Consumer products & services

2.86%

-0.17%

3.03%

Media

3.65%

2.55%

1.10%

Retail

1.25%

-3.85%

5.10%

Travel & leisure

2.18%

0.46%

1.72%

Food, beverage, tobacco

9.67%

5.31%

4.36%

Personal care, drug & grocery stores

8.19%

5.83%

2.36%

Construction & materials

1.25%

0.01%

1.24%

Industrials

9.79%

-1.61%

11.40%

Basic resources

9.07%

6.76%

2.31%

Chemicals

0.53%

-1.43%

1.96%

Energy

12.07%

7.25%

4.82%

Utilities

3.94%

0.73%

3.21%

I hope this table works! Source: FTSE 100 and All-World factsheets.

Every region, and every individual country’s market will obviously be less diverse than the total global market. The FTSE 100’s concentration in out-of-favour sectors is not actually that extreme.

3. Concentration of individual stocks

Firstly, this can arise as a result of M&A activity and does not necessarily imply concentration risk. Every FTSE 100 member is a group of companies and has undergone some M&A activity at some point in its life.

The top 10 in the FTSE 100 come to 50.00% of the total market cap (all of this data is from iShares ETFs) for the MSCI World it’s 18.66%, the S&P 500 28.55%, Japan 22.63%, China 41.51%, France 52.61%.

To repeat point 2, the FTSE 100 isn’t much more concentrated than individual country markets of comparable sizes.

4. Too much UK exposure

With ~3/4 of sales generated overseas, the 100 index is still a very globalised index, not unusual for Europe (https://www.morningstar.com/articles/914896/youre-more-internationally-diversified-than-you-probably-realize, https://content.ftserussell.com/sites/default/files/research/the-global-sales-ratio_-global-and-domestic-firms-final_0.pdf).

However, it is worth saying this figure is not constant, the UK’s global sales ratio appears to have been 54% in 2011 (https://www.regjeringen.no/globalassets/upload/fin/statens-pensjonsfond/eksterne-rapporter-og-brev/2012/msci_equityallocation_march2012.pdf, p. 10).

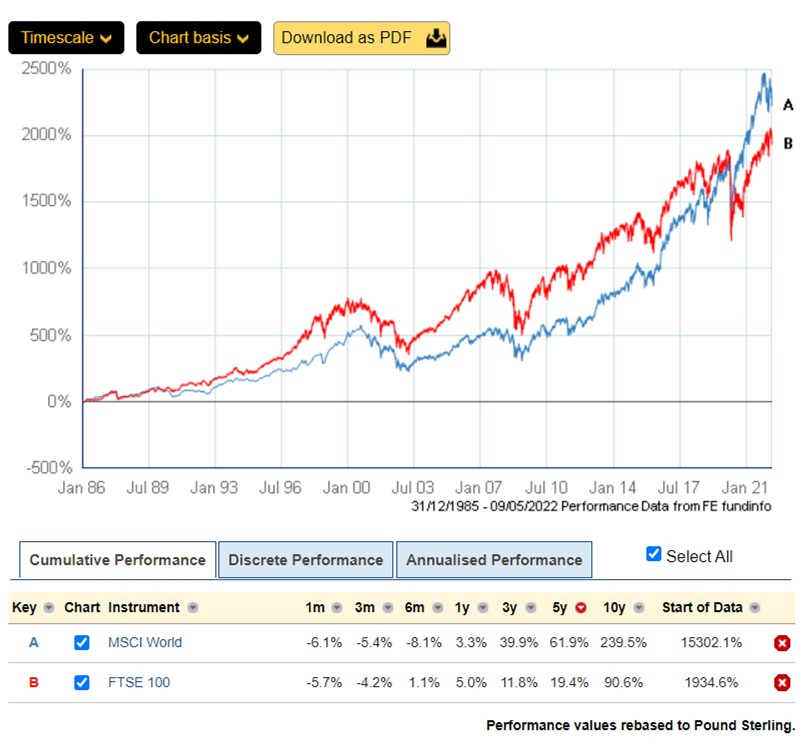

5. Performance

The FTSE 100’s relative underperformance of the wider global market is not a long-term norm. Over the very long term, UK and global equities have fared about the same (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=299335).

This is the total return data back to 1986:

The reversal of fortunes seems to have taken place in the mid-2010s (what was going on in the mid-2010s I wander?), and it’s not all down to slower earnings growth, but rerating too (https://indices.barclays/IM/21/en/indices/static/historic-cape.app). While valuation isn’t everything, it is one of the least bad indicators of future returns potential (https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2129474).

6. Nothing to do with the UK economy

Over short periods we all know the market has little to nothing to do with GDP. But since inception at the start of 1984, the 100’s annualised growth rate excluding dividends has been 5.3% (1,000 on 3/1/84 – 7,265 at the time of writing), compared with nominal GDP growth of 5.0-5.1% (ONS data – 1983 GDP £350,813, 1984 £377,386, 2021 £2,317,054, the endpoints of the two datasets are not the same but this is not meant to be exact, only illustrative).

Further, using that same GDP data back to 1948, and the Barclays UK equity index, you can work out the correlation between the two is between 0.964-0.967, depending if you use year-start or year-end values for the equity index.

7. Global is better / global-by-default

I keep mentioning this source because I admire the book’s simplicity and accessibility to lay readers. Gervais Williams Slow Finance presents a counter to the global-by-default approach of Lars Kroijer among others, the idea of “investing miles” (derived from food miles), that local investors have innate advantages over faraway investors. Though these days with a developed international investing framework, it is as easy to invest globally as domestically.

Global equity portfolios are not a historic norm, the % of overseas equity in UK portfolios, and the % of UK equity held by overseas investors, have both been growing for some time (https://www.regjeringen.no/globalassets/upload/fin/statens-pensjonsfond/eksterne-rapporter-og-brev/2012/msci_equityallocation_march2012.pdf, p. 6, https://www.ons.gov.uk/economy/investmentspensionsandtrusts/bulletins/ownershipofukquotedshares/previousReleases).

Data in the SPIVA scorecard suggests that, especially for the UK, domestic fund managers seem to be much less bad at keeping up with the relevant index than they fare elsewhere (https://www.spglobal.com/spdji/en/documents/spiva/spiva-europe-year-end-2021.pdf).

You could also view the FTSE 100 as “already” having a global portfolio.

8. Placeholder to edit later - dividends are bad

2 -

I made a mistake in investing in what I thought was a sensible low risk investment. I put £20,000 in an ISA with AJ Bell, choosing their moderately cautious ready made portfolio. It is down almost 2% in six weeks.

I wish I had just left it in the bank. I would rather have £20000 + 1% interest subject to inflation eating than £20,000 - 2% - AJ Bell fees subject to inflation eating.

I had around £300,000 which I could have invested but just dipped my toe in the water with last year's ISA allowance. I opened another S&S ISA for this year's allowance but I will not be investing. I clearly do not have the disposition for investing because I am not comfortable with what has happened. The fund might turn around over time, but I have learned that I would rather be safe than sorry and live with what inflation will inflict on me0 -

'Low risk' doesn't mean a one-way bet and any form of investing entails the risk of capital loss - higher risk investments will have lost more than that over that period, but the key message is that six weeks is a hopelessly short duration over which to judge the success or otherwise of investing, which should be considered suitable only for at least five years and preferably significantly more. Were you under the impression that a cautious investment could only increase in value, or did you accept that it could go down but didn't anticipate how that would actually feel?Aristotle67 said:I made a mistake in investing in what I thought was a low risk investment. I put £20,000 in an ISA with AJ Bell, choosing their moderately cautious ready made portfolio. It is down almost 2% in six weeks.

I wish I had just left it in the bank. I would rather have £20000 + 1% interest subject to inflation eating than £20,000 - 2% subject to inflation eating.1 -

The era of globalisation has past. The pandemic and geo political tensions have exposed the fault lines that lie beneath the thin veneer. Having followed both business and markets for a long time. Seems as if this is cusp of a new era for investors. Changes will take time to become apparent but they are already underway.

0 -

A bit of both, if I am honest. I saw all the recommendations for investing, read good reviews of AJ Bell and their portfolios, understood not to try and time the markets, appreciated that investing in one go tends to be better than drip-feeding......but yes, I thought a cautious investment would not go down, or at least not that much, and I clearly had not anticipated how I would feel about it. Very naive.eskbanker said:

'Low risk' doesn't mean a one-way bet and any form of investing entails the risk of capital loss - higher risk investments will have lost more than that over that period, but the key message is that six weeks is a hopelessly short duration over which to judge the success or otherwise of investing, which should be considered suitable only for at least five years and preferably significantly more. Were you under the impression that a cautious investment could only increase in value, or did you accept that it could go down but didn't anticipate how that would actually feel?Aristotle67 said:I made a mistake in investing in what I thought was a low risk investment. I put £20,000 in an ISA with AJ Bell, choosing their moderately cautious ready made portfolio. It is down almost 2% in six weeks.

I wish I had just left it in the bank. I would rather have £20000 + 1% interest subject to inflation eating than £20,000 - 2% subject to inflation eating.2 -

I guess it's times like this we realise that investment is for the long term rather than six weeks. I'm four years in on a minimum ten years with a substantial VLS60 investment and reading this forum over the last few days hasn't been encouraging. I'm not touching it however and will decide in 2028 if I made the wrong choice. I could cash out now at a decent profit but wouldn't have a clue where to put it apart from Premium bonds and the new Chase account or top up my old 123. The thought of inflation nibbling away doesn't sit easy but interesting times all the same.Aristotle67 said:I made a mistake in investing in what I thought was a sensible low risk investment. I put £20,000 in an ISA with AJ Bell, choosing their moderately cautious ready made portfolio. It is down almost 2% in six weeks.

I wish I had just left it in the bank. I would rather have £20000 + 1% interest subject to inflation eating than £20,000 - 2% - AJ Bell fees subject to inflation eating.

I had around £300,000 which I could have invested but just dipped my toe in the water with last year's ISA allowance. I opened another S&S ISA for this year's allowance but I will not be investing. I clearly do not have the disposition for investing because I am not comfortable with what has happened. The fund might turn around over time, but I have learned that I would rather be safe than sorry and live with what inflation will inflict on me1 -

What about bringing a lump sum back to cash and drip-feeding , say £500-£750 each month?0

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.9K Banking & Borrowing

- 254.6K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.7K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards