We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Getting FIREd up 😀

Comments

-

Morning PIP, thank you for your lovely message 🥰!

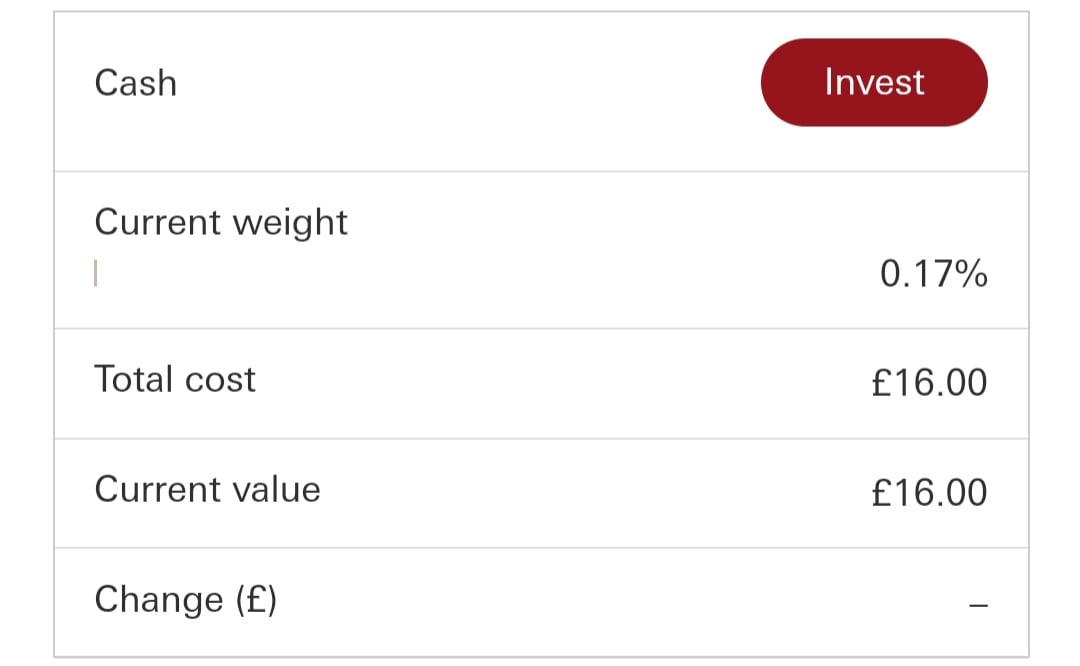

I will leave KP to answer the question on the S&S LISA, as my LISA *whispers* is a cash one (I wanted to keep some money in cash, but it still goes up by 25% on whatever I put in, plus it's earning interest and compounding away in the background). However, I do know that with my S&S ISA, just transferring the money into it is not enough, as it will sit in the "cash" holding account in my name unless I actually choose a fund to put it into. See below screenshot from my account. This is the proceeds of a sale from a fund I don't like any more (which I have actually reinvested in another fund last night, but it's not gone through yet)

Unless I press the invest button, it's just going to sit there as cash. They'll pay me a few pennies in interest, but that's a lot less than it might earn out in the world. I would assume it's the same principle with the S&S LISA.Mortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!3 -

My S&S LISA is with Nutmeg and they invest automatically for you. You do a survey on opening the account and another yearly to check your risk profile and they rob-invest in alignment with that. For non-passive funds I’m pretty pleased with the performance. I’m surprised at you SC - my cash LISA (Skipton) has a terrible interest rate and basically does nothing, hence opening an S&S one.Mortgage free 16/06/2023! £132,500 cleared in 11 years, 3 months and 7 days

'Now is no time to think of what you do not have. Think of what you can do with what there is.' Ernest Hemingway3 -

Now I feel like I've disappointed you, Vix 🤣! I've already got multiple pensions and an S&S ISA, so there was always a cash element to my plans. Mine is with Beehive Money/Nottingham Building Society (not entirely sure what they call themselves). The rate has gone up a couple of times in the last year, currently at 3.5% - not great and below inflation, but the Govt is also adding 25% to my stake each year. There's a bit over £20k in there at the moment, so currently earning £1.95/day in interest. I think it'll be worth around £80k by the time I'm 60, so I'll probably pause any withdrawals from pensions/ISA for a few years at that point and just live off this cash pot, and leave the others growing in the background in the meantimeMortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!5 -

PIP always best to start with a mutual fund so a basket of shares rather than individual ones to have much less riskPennysIntoPounds said:

Hi @South_coast and thread friends, I was going to say hello anyway after randomly coming across your diary and thoroughly enjoying it-killerpeaty said:I remember when the LISA came out, a friend told us (her friends) that she had done the maths and decided that LISA would be better for her than a pension (self employed). We were like "great, what did you invest in?" "A LISA". She didn't know that she would need to invest and we have never managed to convince her.

So I can see that being confused is normal, but someone really should be checking those questions!

and then saw this very pertinent post from @killerpeaty!

I've just been wondering on my own diary if I should be putting money into my S&S LISA as I have no idea about investing at all. Could you please explain like I'm very stupid what your friend should have been doing?!

No worries if it's too arduous, I don't have any money anyway so I don't expect it'll end up mattering a great deal what I do 😁

But many congratulations @South_coast on being mortgage free, that's a lovely thing to hear and a great achievement

all funds have an annual mgt fee so look at low cost ones you can pay 0.10% on a vanguard one vs 2% on others so you can miss out on a lot of money on compound of the fees

2 kinds of funds

accumulation, means any dividends are paid into the fund itself so you don’t have to do anything

distribution or distributing share funds will pay you dividends which means you then have cash in your isa which you have to reinvest fine if you’re older or planning to use that but probably easier now just to buy accumulation

the vanguard funds you can buy as part of a vanguard s$S but also in other ISA providers and are a great first start

you can go for a global one as then it’s companies across the world and you could buy just that - I get more complicated and then buy in other sectors /specific countries but one doesn’t need to

eg Vanguard Global Equity Fund

and Global Equity Small Cap (smaller companies)

I also have US funds eg Vanguard US Equity Fund and European

eg Vanguard FTSE Developed Europe ex-U.K. Equity Index Fund - Accumulation

Vanguard also do a life strategy one 100% which is all shares

Lifestrategy is 80 % shares 20 % bonds

personally I buy just shares but that’s cos I will have a DB pension which is guaranteed soThere are also ETFs which mean that unless you buy them within a vanguard isa there is an upfront service charge to buy as with an individual share. So you can ignore as you start to learnDON'T BUY STUFF (from Frugalwoods)

No seriously, just don’t buy things. 99% of our success with our savings rate is attributed to the fact that we don’t buy things... You can and should take advantage of discounts.... But at the end of the day, the only way to truly save money is to not buy stuff. Money doesn’t walk out of your wallet on its own accord.

https://forums.moneysavingexpert.com/discussion/6289577/future-proofing-my-life-deposit-saving-then-mfw-journey-in-under-13-years#latest4 -

Not disappointed - just surprised! I guess the 25% makes the difference - I just have my cash holding in a higher-interest paying account and let the markets play with my 25% from the govt. My rate on my cash ISA is similar - very poor compared to inflation.South_coast said:Now I feel like I've disappointed you, Vix 🤣! I've already got multiple pensions and an S&S ISA, so there was always a cash element to my plans. Mine is with Beehive Money/Nottingham Building Society (not entirely sure what they call themselves). The rate has gone up a couple of times in the last year, currently at 3.5% - not great and below inflation, but the Govt is also adding 25% to my stake each year. There's a bit over £20k in there at the moment, so currently earning £1.95/day in interest. I think it'll be worth around £80k by the time I'm 60, so I'll probably pause any withdrawals from pensions/ISA for a few years at that point and just live off this cash pot, and leave the others growing in the background in the meantimeMortgage free 16/06/2023! £132,500 cleared in 11 years, 3 months and 7 days

'Now is no time to think of what you do not have. Think of what you can do with what there is.' Ernest Hemingway3 -

I have been feeling spreadsheety - must be the sun peeking through the clouds.If you look at @South_coast vs @themadvix approaches over time, SC looks like she is winning the battle with but with time TMV wins the war.

I looked at a few different scenarios. With all things being equal, the higher interest rate of cash ISAs vs cash LISAs more than compensates for the 25% gummint bonus on that year's contributions. It's a relatively close thing, in the 3 examples I looked at, it took 12/17/18 years for ISA to overtake LISA over a 20-year span. In the worst case scenario, someone using a LISA for cash loses perhaps £7,000-£8.000 vs the ISA).There were a bunch of assumptions (such as assuming a constant interest rate over 20 years etc., that the delta between ISA and LISA cash savings rates will remain constant over this period, that both savers seek out the best rates the market has to offer).3 -

Ooh thanks Ed, that’s interesting. I confess there’s nothing more than internal hunch behind my logic (or even much of that!). That being said, I’m not convinced that the economic model of endless growth is the answer to sustainable life on the planet (nor feasible with demographic changes) so I am likely to be changing my investment strategy (if you can call it that) in the near future anyway.Mortgage free 16/06/2023! £132,500 cleared in 11 years, 3 months and 7 days

'Now is no time to think of what you do not have. Think of what you can do with what there is.' Ernest Hemingway6 -

Very interesting Ed (slow day at work 🤣?) I'm not really 100% sure why I went for a cash LISA instead of S&S, but now I've got that as my "strategy" I'm happy to stick with it. I don't have any DB pensions, so nothing else "guaranteed" apart from the state pension, so good to know it'll always be thereMortgage start: £65,495 (March 2016)

Cleared 🧚♀️🧚♀️🧚♀️!!! In 5 years, 1 month and 29 days

Total amount repaid: £72,307.03. £1.10 repaid for every £1.00 borrowed

Finally earning interest instead of paying it!!!4 -

Hello All - sorry to gate crash,

I recently read a very useful and evidence based book on investing called ‘live the life you want’ by Powell and Howell. I think it gives lots of sensible advice about what to invest in and why.We are investing with an strong ESG tilt in a index tracking fund (ie a mutual) because of similar concerns to Thermavix; as I think environmental sustainable economic growth is possible via technical innovation whilst reducing consumption and environmental impact.. but that’s just the optimist in me..

Also unfashionably I still like bonds especially the super boring government ones, as I remain the cautious type. Also I have a lot of money is cash (which is not advisable but I just like the security of it, and am terrible at spending it!)And low fees are also important to me too.CM4 -

Thanks all for your advice, happily I also have Nutmeg so it doesn't sound like I've been doing anything too stupid!https://forums.moneysavingexpert.com/discussion/6466032/an-in-between-phase/p1

'aggressive safety shot' Ken Doherty4

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.8K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.7K Work, Benefits & Business

- 604.6K Mortgages, Homes & Bills

- 178.7K Life & Family

- 262.3K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards