We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Lloyd’s Bank Preferential Shares

Comments

-

Ok thanks. I missread it. Wish I had sold them now but its probably too late.Thrugelmir said:

112p is the offer.sooty900 said:

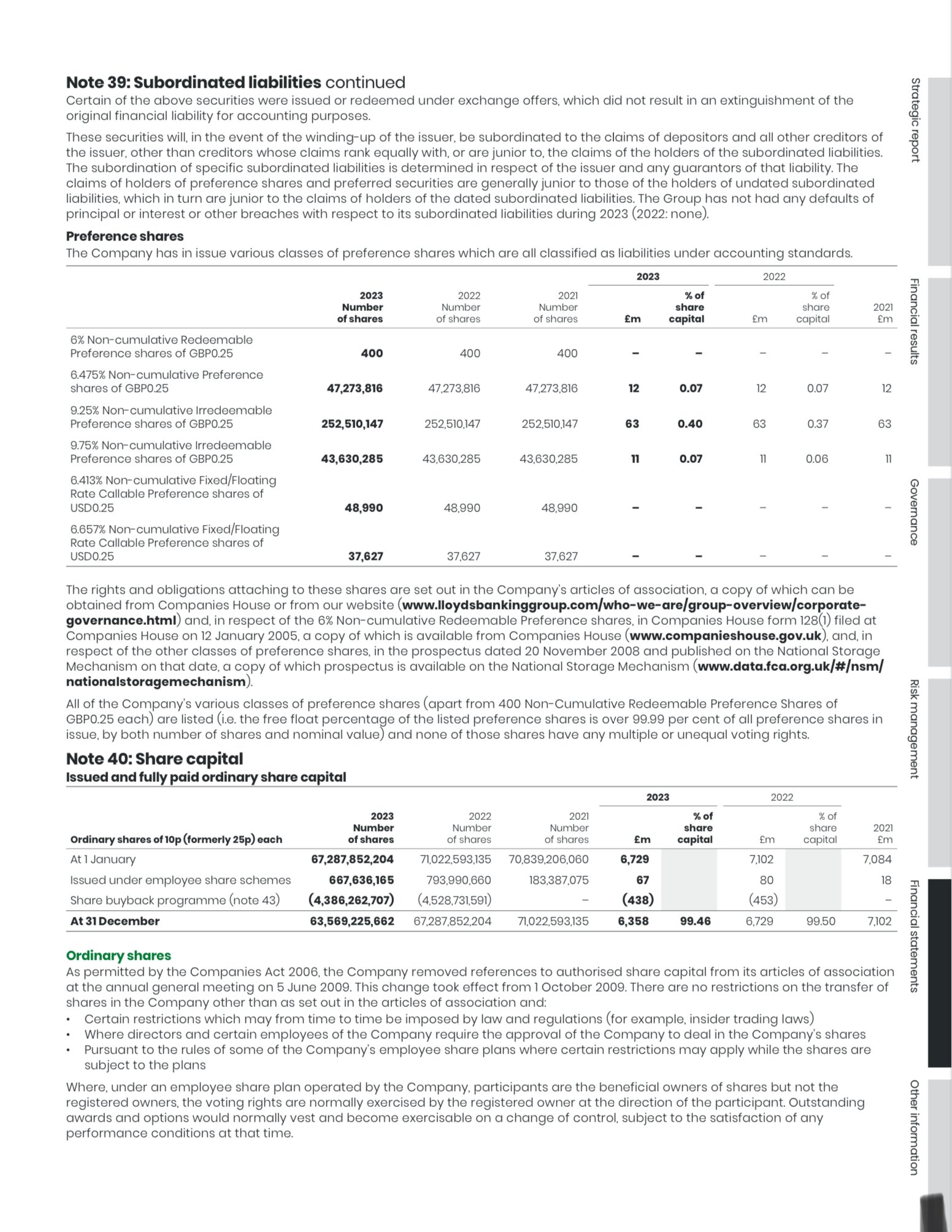

They are offering 112.05 % presumably of the market value on the day. That won't be 112p I don't think.RAFFLES said:I have 400 of the 6.475% shares.

They have been paying a dividend of £12.95 twice a year, so a total of £25.80 per year.

If they are offering £1.12 per share that equals £448

if I continue to hold until 2024, then that will mean that I get £1 for them plus at least another £51.60 (2 years dividends) totalling £451.60. Unless I get 3 years dividends which would mean £477.40

I am no expert, and have probably got this wrong?0 -

Although if you get the money now you can then invest it elsewhere and get other income from it for the next 3 years which should equate to more than the money you'd get if you waitRAFFLES said:I have 400 of the 6.475% shares.

They have been paying a dividend of £12.95 twice a year, so a total of £25.80 per year.

If they are offering £1.12 per share that equals £448

if I continue to hold until 2024, then that will mean that I get £1 for them plus at least another £51.60 (2 years dividends) totalling £451.60. Unless I get 3 years dividends which would mean £477.40

I am no expert, and have probably got this wrong?Remember the saying: if it looks too good to be true it almost certainly is.0 -

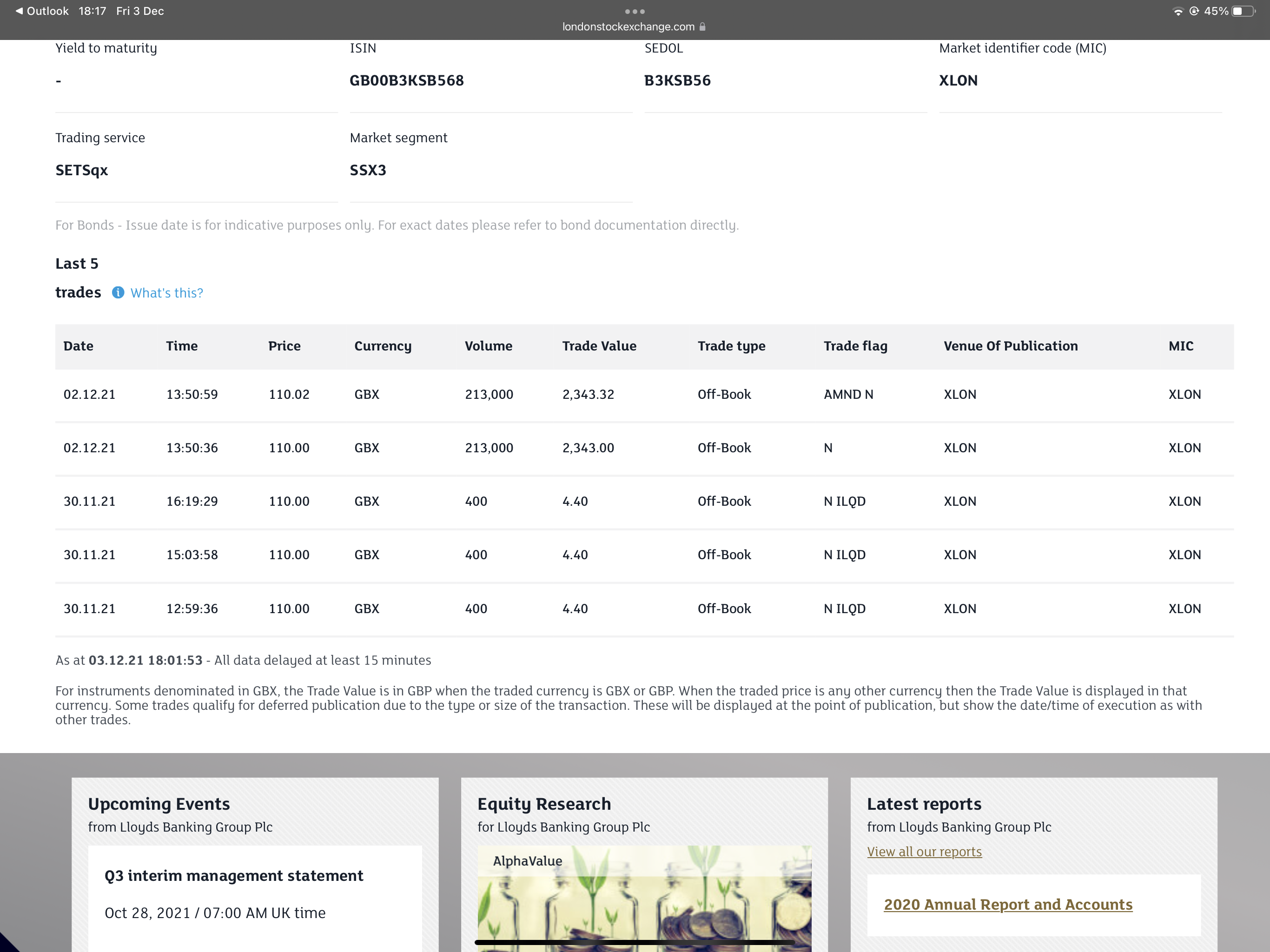

Obviously there will be a broker's fee but you can always sell them in the market. Looks today like people have been achieving 110p for their sales. Appears that three people sold their free shares.sooty900 said:

Ok thanks. I missread it. Wish I had sold them now but its probably too late.Thrugelmir said:

112p is the offer.sooty900 said:

They are offering 112.05 % presumably of the market value on the day. That won't be 112p I don't think.RAFFLES said:I have 400 of the 6.475% shares.

They have been paying a dividend of £12.95 twice a year, so a total of £25.80 per year.

If they are offering £1.12 per share that equals £448

if I continue to hold until 2024, then that will mean that I get £1 for them plus at least another £51.60 (2 years dividends) totalling £451.60. Unless I get 3 years dividends which would mean £477.40

I am no expert, and have probably got this wrong?

1 -

I received £448.20 for my shares £1.1205 times 400."Look after your pennies and your pounds will look after themselves"0

-

Also now received final dividend of £1.06

total £449.26"Look after your pennies and your pounds will look after themselves"0 -

Reviving an old thread

")

Had a letter today saying Lloyds will be redeeming these shares for 100p each in September - I shall miss my twice-yearly £12.95!0 -

garfield33 said:Reviving an old thread

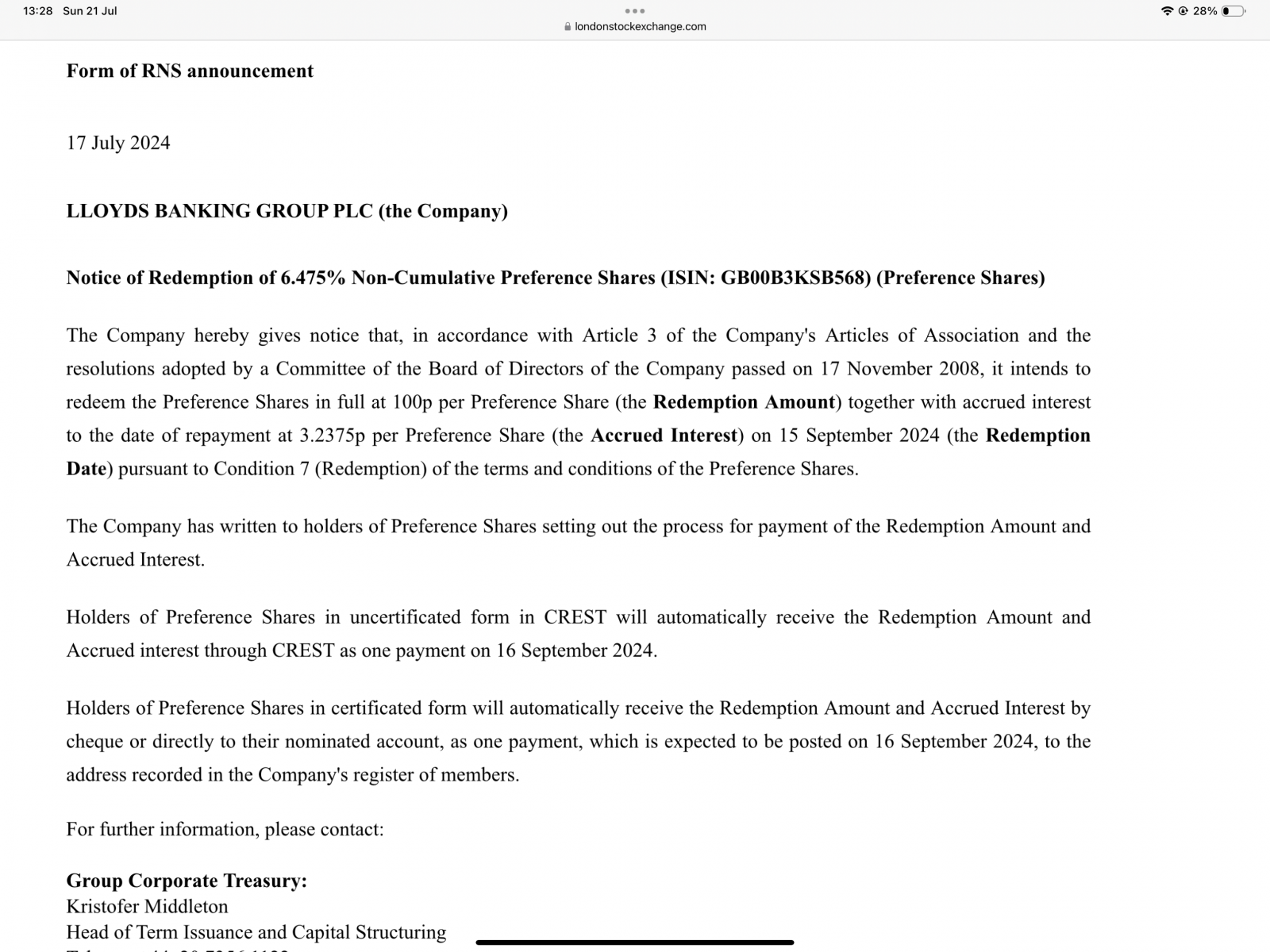

Had a letter today saying Lloyds will be redeeming these shares for 100p each in September - I shall miss my twice-yearly £12.95!Oh yes; 100p plus accrued dividend* of 3.2375p on 15/09/24 so you'll receive one last dividend. This is the first opportunity Lloyds has had to redeem these.

*Not sure why the RNS states interest, these preference shares pay a dividend. I've just double checked the prospectus and there's no mention of interest, only dividends.https://www.londonstockexchange.com/news-article/LLOY/redemption-of-preference-shares/16572482 1

1 -

It’s probably because Lloyds hold these as (interest bearing) subordinated liabilities on their balance sheet rather than equity (which pays dividends). Accounting standards can require redeemable pref shares to be recorded as liabilities, not equity, as they are no different in substance to debt.wmb194 said:garfield33 said:Reviving an old thread

Had a letter today saying Lloyds will be redeeming these shares for 100p each in September - I shall miss my twice-yearly £12.95!Oh yes; 100p plus accrued dividend* of 3.2375p on 15/09/24 so you'll receive one last dividend. This is the first opportunity Lloyds has had to redeem these.

*Not sure why the RNS states interest, these preference shares pay a dividend. I've just double checked the prospectus and there's no mention of interest, only dividends.HMRC will likely still treat this as a dividend I believe

https://www.gov.uk/hmrc-internal-manuals/corporate-finance-manual/cfm21120 3

3 -

Hi

I have received a letter recently from Lloyds informing me that I have received a notice of redemption of 6.475% non cumulative preference shares. Currently holding 400. They are saying that in accordance it intends to redeem the preference shares in full at 100p per preference share together with accrued interest to the date of repayment at 3.2375p per preference share.

What exactly does this mean in layman's terms? Is it they want to buy them back? What about if I don't want to sell them, can I exercise that right or do I not have that option? Just so I know for future why would companies want to do this? Be good to get this broken by someone who knows a bit more about this than me. Thanks0 -

They’re redeemable preference shares and this was always the first opportunity for them be redeemed - have a look at the prospectus. You don’t have a choice; you’ll receive £400 and a last dividend.isotonic_uk said:Hi

I have received a letter recently from Lloyds informing me that I have received a notice of redemption of 6.475% non cumulative preference shares. Currently holding 400. They are saying that in accordance it intends to redeem the preference shares in full at 100p per preference share together with accrued interest to the date of repayment at 3.2375p per preference share.

What exactly does this mean in layman's terms? Is it they want to buy them back? What about if I don't want to sell them, can I exercise that right or do I not have that option? Just so I know for future why would companies want to do this? Be good to get this broken by someone who knows a bit more about this than me. Thanks

Why? They don’t count towards loss absorbing capital anymore ie. they’re obsolete and they’re relatively expensive.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354.7K Banking & Borrowing

- 254.5K Reduce Debt & Boost Income

- 455.6K Spending & Discounts

- 247.6K Work, Benefits & Business

- 604.5K Mortgages, Homes & Bills

- 178.6K Life & Family

- 262.1K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards