We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

Shariah compliant tracker

Comments

-

Some of us setup a regular investment share trade at the reduced £1.50 rate and cancel it after a single execution.SharpShooter said:AJ Bell for buying and selling stocks is ok, as long as you are ok with paying large fees of £10.

Given that ETFs have no FSCS protection then I don't see the harm in selecting a similar investment from a different fund manager for the new account. If the overall amounts were substantial enough then I would probably even use an unrelated platform.masonic said:I would suggest sticking to one global tracker if possible.

0 -

Magginnis said:Thanks, Am I also correct in saying this is a tracker fund (so the risk is quite low)If markets tank an index tracker will slavishly follow the index down to where ever it ends up. It has no choice, it is tracking its index. An actively managed investment has the opportunity (in theory at least) to take mitigating actionSo it's not as black and white as you imagine.100% equities is not a low risk option however you package it up

0 -

Alexland said:

Given that ETFs have no FSCS protection then I don't see the harm in selecting a similar investment from a different fund manager for the new account. If the overall amounts were substantial enough then I would probably even use an unrelated platform.masonic said:I would suggest sticking to one global tracker if possible.In my view that would just add unnecessary complexity. For example in my S&S ISA and SIPP I hold VEVE, but could have opted for Vanguard in one account and iShares in another. It would just create another line of stock to track and integrate without giving me any appreciable added diversification or protection. While those investments would track different indices, the differences are not significant and it would make tracking the whole portfolio more complicated for little to no advantage. I can certainly see the benefit of using unrelated platforms to insure against the risk of one going bust, but this is not something I'd consider worthy of taking measures against when talkig about Vanguard or Blackrock.The principal reason to avoid too much diversification when investing using moral principles is that different funds and indices use different interpretations of moral standards. If you are trying to avoid certain activities and practices then you double your efforts in monitoring multiple funds and increase the likelihood of gaining unwanted exposure to companies which do not meet your personal criteria. I don't personally believe such criteria are compatible with index investing, but for those who do it may be the primary driving force of their decision of which investment to buy.0 -

To add to the previous replies you may even say that the risk is higher than a standard tracker as you are limiting the selection of shares and sectors in much the same way that an ESG fund would have a more limited range to choose.Magginnis said:Thanks, Am I also correct in saying this is a tracker fund (so the risk is quite low) and also there are a broad range/ base of different stocks to diversify risk?

A tracker could track bonds which would be lower risk than a tracker that covered emerging markets so it's not the fact that it's a tracker that impacts that risk.Remember the saying: if it looks too good to be true it almost certainly is.0 -

My SIPP is also invested is VEVE but then we hold similar HMWO in my wife's SIPP and its actually easier to track in my HL watchlist as the investments appear as separate lines so I can quickly see how each account is doing. Each to their own preferences.masonic said:In my view that would just add unnecessary complexity. For example in my S&S ISA and SIPP I hold VEVE, but could have opted for Vanguard in one account and iShares in another. It would just create another line of stock to track and integrate without giving me any appreciable added diversification or protection.0 -

Fair enough, I've not come across that particular limitation of needing different investments to split accounts into separate lines before.Alexland said:

My SIPP is also invested is VEVE but then we hold similar HMWO in my wife's SIPP and its actually easier to track in my HL watchlist as the investments appear as separate lines so I can quickly see how each account is doing. Each to their own preferences.masonic said:In my view that would just add unnecessary complexity. For example in my S&S ISA and SIPP I hold VEVE, but could have opted for Vanguard in one account and iShares in another. It would just create another line of stock to track and integrate without giving me any appreciable added diversification or protection.

0 -

It's not really a limitations as the app let's you setup multiple watchlists but I find it simpler to just have one watchlist and I know which investment relates to which account. Where we have exactly matching accounts I just know half the units are in each account.masonic said:Fair enough, I've not come across that particular limitation of needing different investments to split accounts into separate lines before.0 -

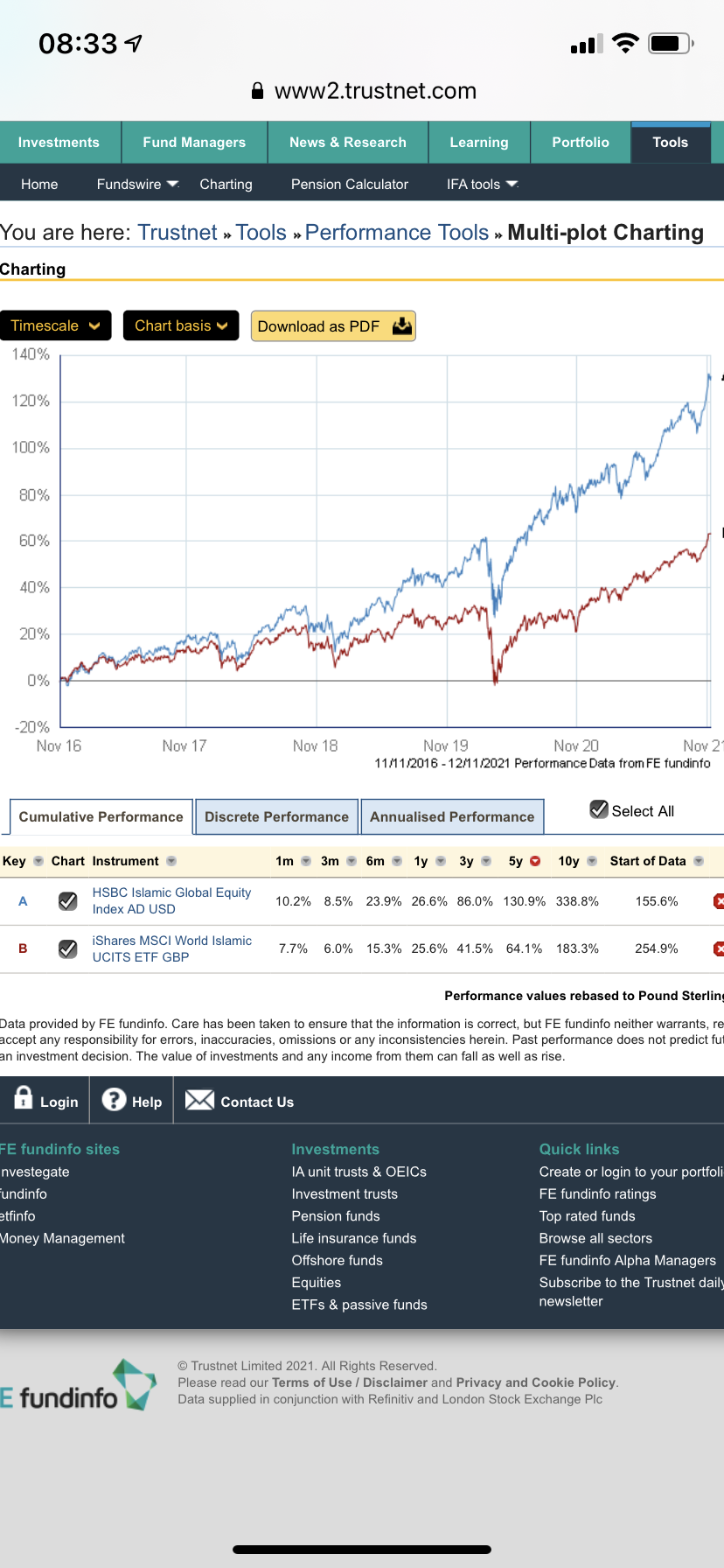

Have I got the wrong funds? HSBC seems much better that iShares

0

0 -

You have the correct funds (there is a GBP version of the HSBC fund, but performance of the USD unit class rebased to GBP is more or less the same). The MSCI World Islamic Index (used by iShares) appears to have excluded Microsoft, Apple, Amazon, Tesla, Google, Facebook and Nvidia from its index. The Dow Jones Islamic Market Titans 100 Index (used by the HSBC fund) includes all of those companies. The indexes being tracked by the two funds are therefore hugely different. If your own Islamic principles do not permit you to invest in those companies then you would have no choice but to opt for the more restrictive iShares ETF, but if your principles are more relaxed you could have gone for the HSBC fund. While the HSBC fund has less stringent criteria, it is a more concentrated index with only around 100 holdings vs >300 in the iShares ETF.MX5huggy said:Have I got the wrong funds? HSBC seems much better that iShares

4 -

mmm - IIRC last time I checked the MSCI Islamic index was very high in tech but now it is far mor e reasonable. The HSBC index however is 33% tech and 13% in the the relatively new Communications Services sector which includes facebook, Netflix and Alphabet)(Google). Looking at the largest underlying investments gives a total of 32% of the whole fund to Microsoft, Apple, Facebook, Amazon and Alphabet. Tesla is 2.8%. North America is 74.5%. The whole of the UK gets less than half the amount allocated to Microsoft. This is not what one should expect from a broadly based global investment.masonic said:

You have the correct funds (there is a GBP version of the HSBC fund, but performance of the USD unit class rebased to GBP is more or less the same). The MSCI World Islamic Index (used by iShares) appears to have excluded Microsoft, Apple, Amazon, Tesla, Google, Facebook and Nvidia from its index. The Dow Jones Islamic Market Titans 100 Index (used by the HSBC fund) includes all of those companies. The indexes being tracked by the two funds are therefore hugely different. If your own Islamic principles do not permit you to invest in those companies then you would have no choice but to opt for the more restrictive iShares ETF, but if your principles are more relaxed you could have gone for the HSBC fund. While the HSBC fund has less stringent criteria, it is a more concentrated index with only around 100 holdings vs >300 in the iShares ETF.MX5huggy said:Have I got the wrong funds? HSBC seems much better that iShares

So I would certainly not recommend the HSBC fund to anyone who did not understand the downsides.2

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 355.1K Banking & Borrowing

- 254.7K Reduce Debt & Boost Income

- 455.8K Spending & Discounts

- 247.9K Work, Benefits & Business

- 605K Mortgages, Homes & Bills

- 178.8K Life & Family

- 262.7K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards