We’d like to remind Forumites to please avoid political debate on the Forum.

This is to keep it a safe and useful space for MoneySaving discussions. Threads that are – or become – political in nature may be removed in line with the Forum’s rules. Thank you for your understanding.

📨 Have you signed up to the Forum's new Email Digest yet? Get a selection of trending threads sent straight to your inbox daily, weekly or monthly!

The Forum now has a brand new text editor, adding a bunch of handy features to use when creating posts. Read more in our how-to guide

Wisdom sought on Vanguard funds

Comments

-

This is not correct. Ireland based ETFs do have FSCS protection if you experience broker fraud or insolvency, just as you would have protection if holding any other UK listed share, and providing you use a FCA authorised broker. If the Irish investment company defrauds you or becomes insolvent then you may or may not have protection from the Irish scheme (Vanguard, SPDR and iShares ETFs definitely do not have protection - source), but even if your provider says it does I'd draw your attention to the failure of the passport scheme to protect Icelandic bank savers and point out there is zero precedent for such a scheme compensating UK investors.GeoffTF said:

The FSCS does protect UK domiciled equity funds against fraud or insolvency, but does not protect them from loss of value of the underlying investments. Ireland based ETFs are protected up to €20,000 on the same basis.Albermarle said:As Dunstonh says , no ETF's are covered by UK compensation scheme as they are considered to be a share type investment by FSCS . Are you sure they are covered by the Irish scheme?

If you have a small account, you are going to be covered by the compensation scheme anyway.

Correct but could take months to untangle a collapsed broker ( see SVS securities ) , or longer .

It can indeed take months to recover investments from a collapsed broker. Small investors putting away a few £hundred each month, should not have to worry to much about that. If they do, they probably should not be investing in equities anyway. The main obstacle will be that they cannot pay into two stocks and shares ISAs in a tax year (which is a bit unfair if one of them has collapsed). They should not pay tax on a few months savings in an unsheltered account, however. Nonetheless, having a broker fail will always be a serious nuisance.

2 -

It all depends on when you measure from and to. For example if we go back exactly 20 years from today the FTSE 100 easily outperformed the US markets until the rest of the world caught up in around 2015. The switchover point was as Tebbins points out around 2010.jimjames said:

I'm not sure that assertion is backed up by the numbers. I'd say the FTSE100 has underperformed for at least 20 years compared to world indexes at least ex dividendstebbins said:Thrugelmir said:

Forget indices. Active management is the most appropriate route to gain UK exposure.masonic said:Thrugelmir said:

The UK markets have an international bias. The mantra rolls on and on.bostonerimus said:Avoiding the UK bias of VLS is a good reason not to buy it,I wouldn't disagree, but it's generally not the fact that the market is located in the UK that makes it undesirable, rather its composition, and perhaps the fact that it doesn't really give much exposure to companies reflective of the UK economy. The UK is a region where a simple UK cap weighted index really hasn't been a good investment choice for a few decades. UK bias via active funds or FTSE250 exposure makes more sense than the All-share exposure of VLS.OP, I think the route via ultra-cheap broker for small amounts (no custody or trading fees), followed by transfer to flat fee broker/investment platform when you reach a critical mass, makes more sense than going direct to Vanguard, if you can get what you need from ETFs.1. UK equity indices such as the FTSE 100 and all-share have not been underperforming for decades but only since the mid 2010s - trustnet chart, compare with FTSE world/MSCI world (https://www2.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NUKX, yes this is in £)

FTSE100 has increased approx 5% since 2000.

MSCI has gone increased 300% in the same time

https://backtest.curvo.eu/market-index/msci-world

https://www.macrotrends.net/2324/sp-500-historical-chart-data0 -

And as a consequence retail investors will continue to invest in concepts rather than hard financial data. At least until the music finally stops.jimjames said:

I'm not sure that assertion is backed up by the numbers. I'd say the FTSE100 has underperformed for at least 20 years compared to world indexes at least ex dividendstebbins said:Thrugelmir said:

Forget indices. Active management is the most appropriate route to gain UK exposure.masonic said:Thrugelmir said:

The UK markets have an international bias. The mantra rolls on and on.bostonerimus said:Avoiding the UK bias of VLS is a good reason not to buy it,I wouldn't disagree, but it's generally not the fact that the market is located in the UK that makes it undesirable, rather its composition, and perhaps the fact that it doesn't really give much exposure to companies reflective of the UK economy. The UK is a region where a simple UK cap weighted index really hasn't been a good investment choice for a few decades. UK bias via active funds or FTSE250 exposure makes more sense than the All-share exposure of VLS.OP, I think the route via ultra-cheap broker for small amounts (no custody or trading fees), followed by transfer to flat fee broker/investment platform when you reach a critical mass, makes more sense than going direct to Vanguard, if you can get what you need from ETFs.1. UK equity indices such as the FTSE 100 and all-share have not been underperforming for decades but only since the mid 2010s - trustnet chart, compare with FTSE world/MSCI world (https://www2.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NUKX, yes this is in £)

FTSE100 has increased approx 5% since 2000.

MSCI has gone increased 300% in the same time2 -

As far as I know, there are still no UK domiciled ETFs. You are right about the Ireland domiciled ETFs. The Vanguard ETFs are regulated by the Central Bank of Ireland. There is a Monevetor article entitled "Investor Compensation Schemes - are you covered". The Accumulator managed to get a letter from Vanguard clarifying a previous statement and "it turns out that ‘maybe’ means that Vanguard Irish domiciled funds and ETFs are not covered by the Irish Compensation Scheme." So the Irish domiciled OEICs are not covered either. We are entirely reliant on Vanguard, overseen by the Central Bank of Ireland here.Albermarle said:The FSCS does protect UK domiciled equity funds against fraud or insolvencyFor funds ,as in OEICS for example this is true.

But not for ETF's . IN the link below, scroll down to the section on Investments .

0 -

The Vanguard Global Bond Index Fund is domiciled in Ireland, by the way.0

-

No ETFs, regardless of where they are domiciled get any protection from UK or domicile country. Same as investment trusts. Both are classed as direct assets.

There is an exception that was a rarity but maybe not so much now with the robo providers. Where it is a packaged product that uses an ETF/IT within it, then FSCS protection applies if the packaged product is UK domiciled (i.e. an FCA regulated provider)I am an Independent Financial Adviser (IFA). The comments I make are just my opinion and are for discussion purposes only. They are not financial advice and you should not treat them as such. If you feel an area discussed may be relevant to you, then please seek advice from an Independent Financial Adviser local to you.2 -

Is the global bond fund on vanguard V3GP?Nurse striving for financial freedom0

-

The MSCI world is the longest dated one I can find on trustnet.Thrugelmir said:

And as a consequence retail investors will continue to invest in concepts rather than hard financial data. At least until the music finally stops.jimjames said:

I'm not sure that assertion is backed up by the numbers. I'd say the FTSE100 has underperformed for at least 20 years compared to world indexes at least ex dividendstebbins said:Thrugelmir said:

Forget indices. Active management is the most appropriate route to gain UK exposure.masonic said:Thrugelmir said:

The UK markets have an international bias. The mantra rolls on and on.bostonerimus said:Avoiding the UK bias of VLS is a good reason not to buy it,I wouldn't disagree, but it's generally not the fact that the market is located in the UK that makes it undesirable, rather its composition, and perhaps the fact that it doesn't really give much exposure to companies reflective of the UK economy. The UK is a region where a simple UK cap weighted index really hasn't been a good investment choice for a few decades. UK bias via active funds or FTSE250 exposure makes more sense than the All-share exposure of VLS.OP, I think the route via ultra-cheap broker for small amounts (no custody or trading fees), followed by transfer to flat fee broker/investment platform when you reach a critical mass, makes more sense than going direct to Vanguard, if you can get what you need from ETFs.1. UK equity indices such as the FTSE 100 and all-share have not been underperforming for decades but only since the mid 2010s - trustnet chart, compare with FTSE world/MSCI world (https://www2.trustnet.com/Tools/Charting.aspx?typeCode=NM990100,NUKX, yes this is in £)

FTSE100 has increased approx 5% since 2000.

MSCI has gone increased 300% in the same time

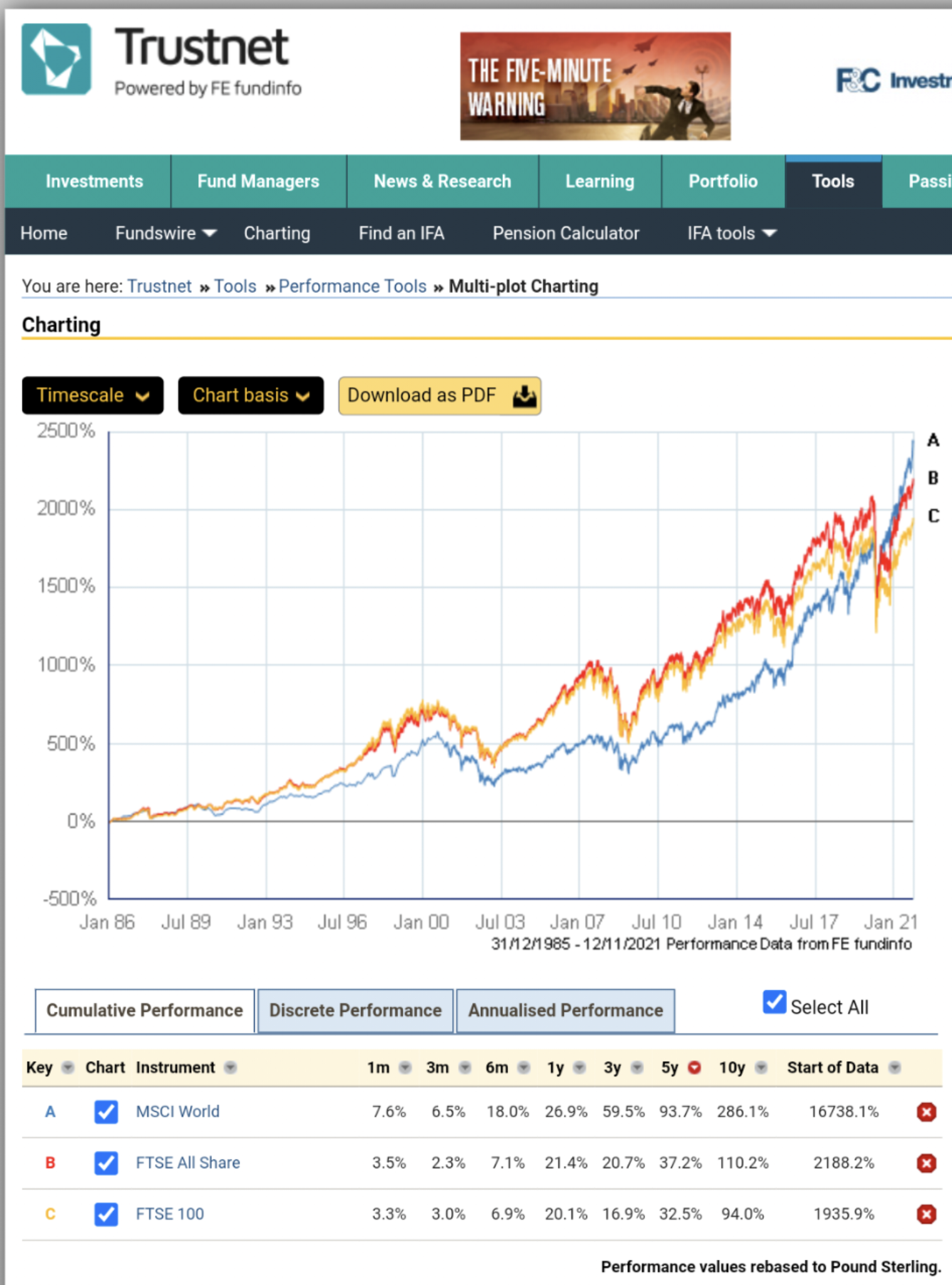

Firstly here's it, the FTSE 100 and all share's total returns back to 31/12/1985 when UK total return data begins.

...

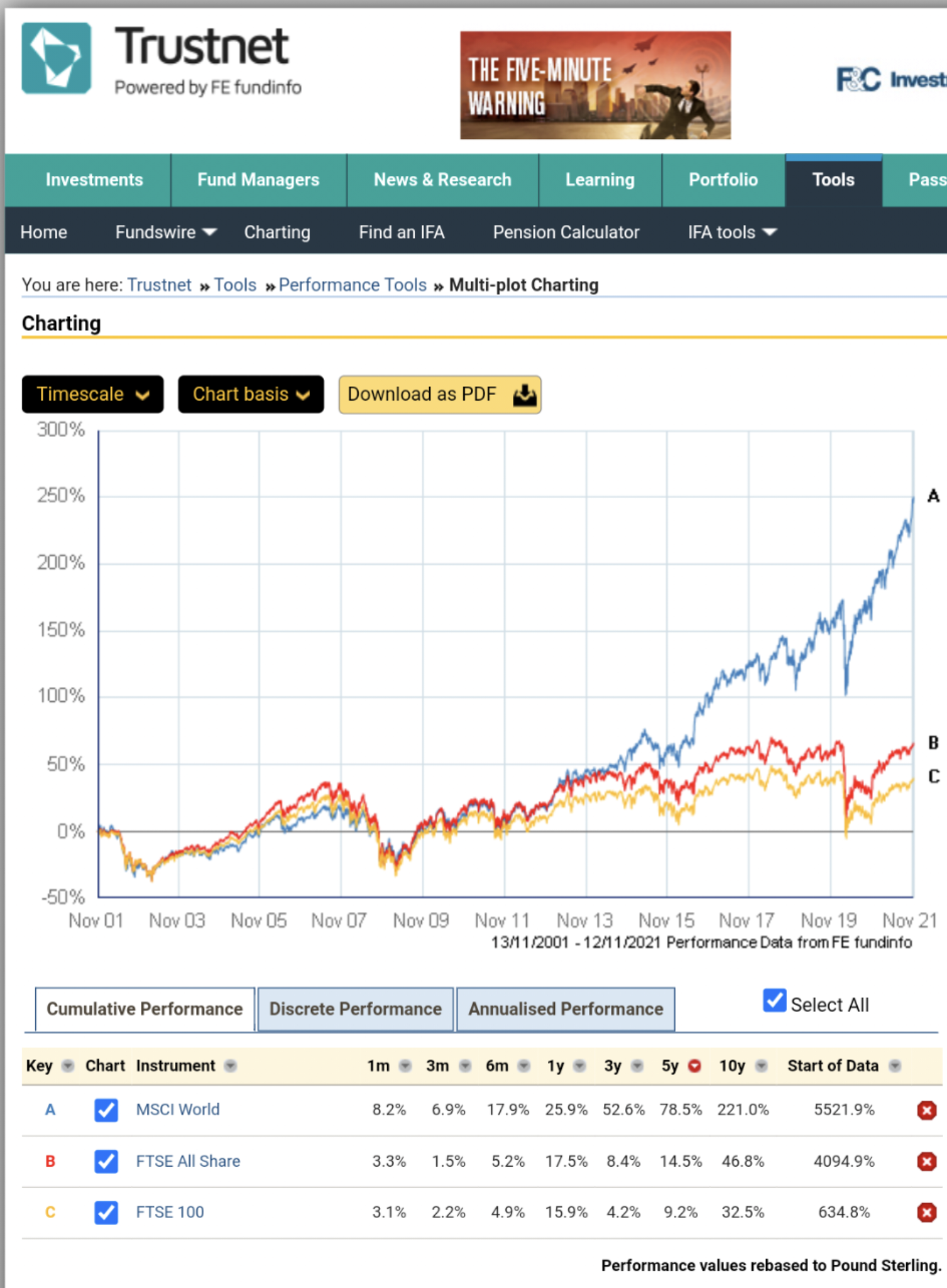

Next up, the past 20 years to date

...

Index price only.

...

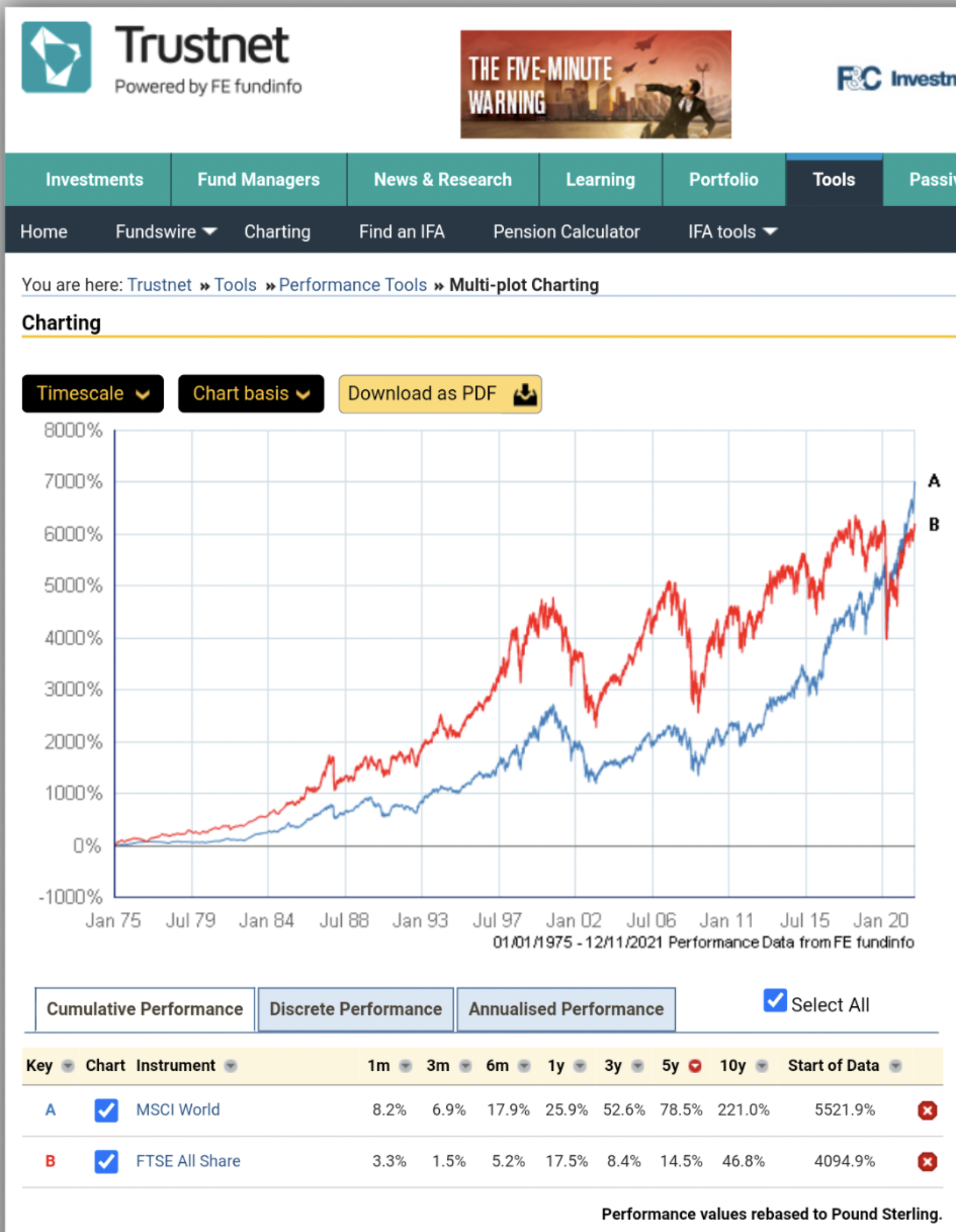

Remove the FTSE 100 as its index only goes back to 1984, and look at the FTSE all share and Msci world as far back as the latter goes, to start 1975. However that looks like this because that startpoint is the bottom of the 1972-74 crash, UK equities worst crash on record. ...

...

So to make it fair I set the startpoint forward 1 year. Whether you set the startpoint anytime between then and roughly 2010, supports my argument as it is clear UK large cap equity's alleged decades of underperformance did not happen.

...3 -

I’ve only been investing in an ISA for 6 months. Over that 6 months I’ve spent 26.1% of my cash on bonds because the equities have been outperforming bonds.HCIMbtw said:

have you been buying a lot of units in the bond index these past two years?MX5huggy said:Global Bond Index and FTSE Global All Cap Fund for me ATMThis is what I do at 75/25 whenever I invest I rebalance back to 75/25 with a rule that if it ever gets more than 5% out of balance I would rebalance by selling one and buying the other. But I also have a plan to move to 80/20 or even 85/15 if there is an equity correction (it might be better to hold cash over bonds for this purpose).I Don’t use ETF’s because you have to buy whole units so there would always be small bits cash left after each transaction at your and mine levels it would make a difference.Once investment builds to I might swap to Fidelity or HL and go with ETF’s as both only currently charge £45 platform fee for ETF’s. The Green dots are buys but not all buys are the same value I’m down £5.50 on the bonds currently0

The Green dots are buys but not all buys are the same value I’m down £5.50 on the bonds currently0 -

It looks like MSCI World really starts to pull ahead from the middle of 2016......I wonder what happened around that time which could affect ex-UK investments in such a positive way....

") Incidentally, how did you find that MSCI World on Trustnet's charting tool......it's not listed under indices (I only have the free account though)3

Incidentally, how did you find that MSCI World on Trustnet's charting tool......it's not listed under indices (I only have the free account though)3

Confirm your email address to Create Threads and Reply

Categories

- All Categories

- 354K Banking & Borrowing

- 254.3K Reduce Debt & Boost Income

- 455.3K Spending & Discounts

- 247K Work, Benefits & Business

- 603.6K Mortgages, Homes & Bills

- 178.3K Life & Family

- 261.2K Travel & Transport

- 1.5M Hobbies & Leisure

- 16.1K Discuss & Feedback

- 37.7K Read-Only Boards